Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

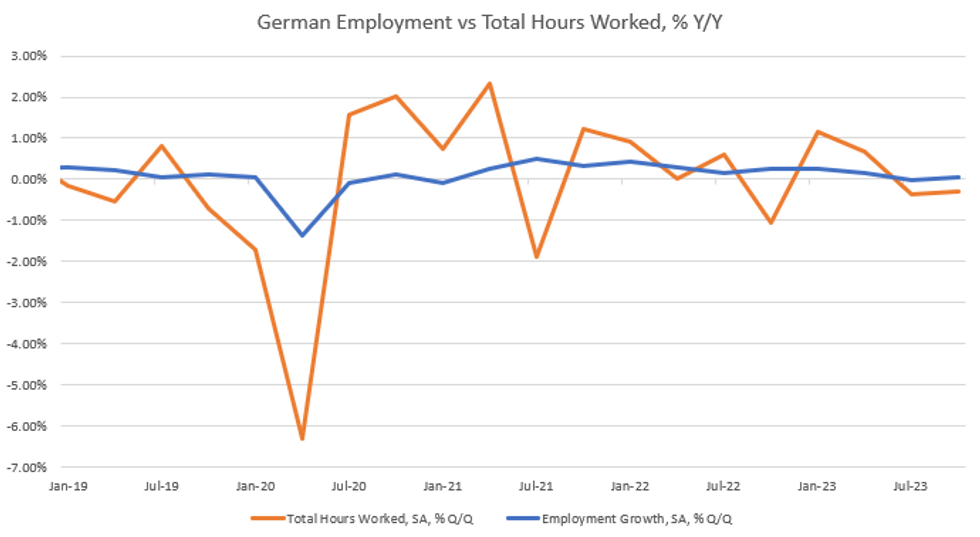

German employment rose further in Q4 2023, extending its all-time high to 46.2m (+0.06% Q/Q SA, +28k vs -0.02% prior).

- The increase was driven by the services sector, in which employment rose +0.06% Q/Q (SA, +20k, vs +0.09% prior), with the "public service providers, education, health" subsector in particular, up +0.34 Q/Q (SA, 41k, vs +0.38% prior). Excluding this subsector, employment fell -0.04% Q/Q (SA, -13k, vs -0.16% Q/Q).

- In particular, this decline could be seen in the manufacturing sector, which saw a decrease of -0.24% Q/Q (SA, -26k, vs -0.15% prior), the fastest drop since the pandemic, showing that weak developments in industrial production are pushing through to the respective labour market.

- The sectoral analysis must be taken with caution, though, as there is a fairly volatile error term in between the sum of the sectoral employment figures and the total.

- The number of self-employed persons decreased -0.3% Q/Q (SA, -10k, vs -0.3% prior), continuing a long-term downward trend which was halted in Q3, and provides a weak picture in terms of the lingering German debate of the government trying to ease business conditions in the country.

- Hours worked per person employed decreased by -0.4% Q/Q to 335.6h on a seasonally-adjusted basis (vs -0.3% prior), keeping total hours worked at 15.4bln, also down -0.3% Q/Q SA (vs -0.3% prior).

- Overall, the report paints a weaker picture than the headline figure suggests. The public sector drove the employment uptick, showing that, taking into account lower hours worked, the private sector labour market became notably weaker in the second half of 2023.

- Soft data mirrors that picture - the IFO employment barometer (96.5 in Dec) has been in slightly contractionary territory since mid-2023, with the expansionary signals of the services balance (6.7 points in Dec) not making up for the downtrend in manufacturing (-13.6 points).

MNI, Destatis

MNI, Destatis

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok