Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

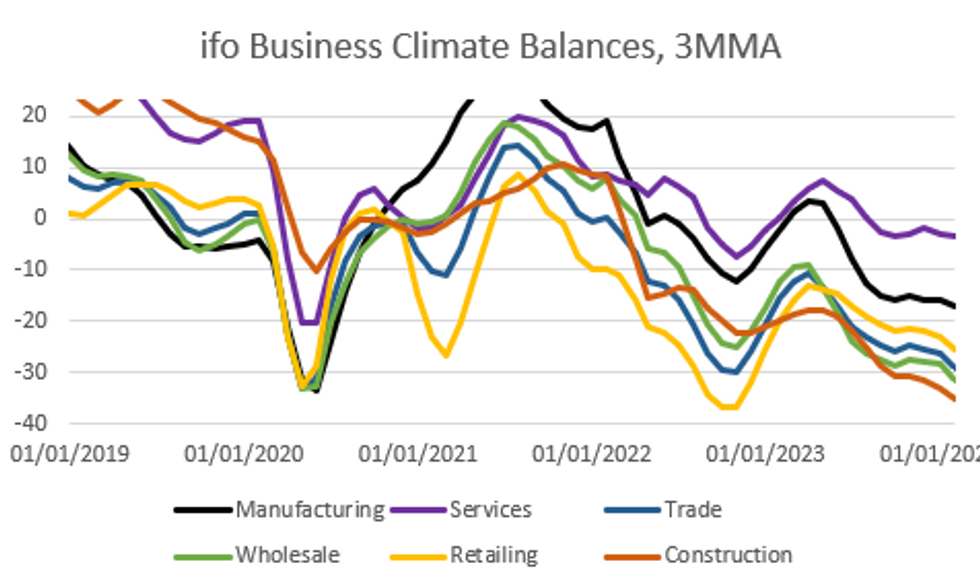

Germany's IFO Business Confidence Index edged up to 85.5 in February, in line with expectations and higher than the 85.2 prior. It also marked a modest divergence with February's flash Composite PMI which weakened - but both surveys pointed to poor economic momentum to start the year, and suggested further deterioration in manufacturing contrasting with solidifying services.

- The IFO Current Assessment reading came in almost in line with both consensus and the prior value, at 86.9, with January's reading downwardly revised by 0.1pts, also to 86.9. IFO Expectations were also slightly stronger than expected, and increased to 84.1 (from 83.5 prior).

- The slight increase was driven by a stronger services sector, with the respective Business Climate balance up to -4.1 (vs -4.8 prior). IFO notes that services providers were content with the current business situation but their expectations remained weak. Conversely, the manufacturing sector reading fell versus January (balance at -17.4 vs -15.8, back in line with December 2023 levels).

- Still, this was a slightly less weak signal for activity than seen in February's Manufacturing PMI, which clearly broke its recent uptrend by declining to a 4-month low at 42.3 (down 3.2 points vs 45.5 prior), while Services PMI increased 0.5 points to 48.2 (vs 47.7 prior).

- The Construction sector continues looking weakest of all, which while rising to -35.4 was up only slightly from January's -35.8, which was the weakest level since Oct 2022.

- Having a broad look at a less volatile 3MMA measure, there seems to be an ongoing downtrend in all sectors except services.

- Overall, even though the release did not surprise to the downside, it also failed to provide any indication of resurgent momentum in the German economy. This mirrors most hard data including core factory orders, which have remained on a downtrend in recent months. January's truck toll index suggested some potential momentum for industrial production in Q1, though.

- The current consensus real GDP forecast for 2024 is +0.2%, vs -0.3% in 2023, with sequential growth only returning in Q2 '24 (+0.2% Q/Q) after 4 consecutive flat/negative quarters. These forecasts were only recently revised downwards - February's IFO print will not provide a major shift here.

MNI, Destatis

MNI, Destatis

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok