Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

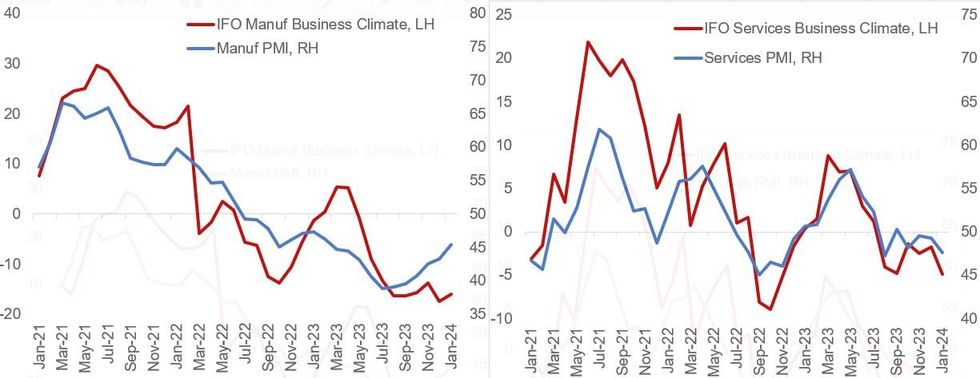

Germany's IFO Business Confidence Index slipped to 85.2 in January, weaker than the 86.6 expected and the 86.3 prior (downwardly revised). The Current Assessment and Expectations readings were each weaker than expected, and fell to 87.0 and 83.5 respectively (from 88.5 and 84.2 respectively prior, with Expectations downwardly revised).

- The unexpected deterioration was largely about Germany's services sector weakening - confirming what we saw in the flash January PMIs - with other non-manufacturing industries deteriorating further too.

- The IFO Manufacturing Business Climate subindex rebounded 1.4 points in January to -16.0 from a 42-month low in December of -17.4. IFO Services conversely saw its biggest monthly drop since August, falling 3.2 points to a 14-month low -4.9.

- In the flash January PMIs released the day prior, Manufacturing PMI accelerated to an 11-month high of 45.4 (up 2.1 points), while Services PMI slid 1.7 points to a 5-month low 47.6.

- The Construction sector looks weakest of all, falling to -35.9 in January - the lowest level since September 2005. And the Trade sector climate fell to its weakest level since Oct 2022.

- Taken together with other data including factory orders, it still appears that German manufacturing is bottoming out at very weak levels. Worryingly, though, the construction and trade sectors are deteriorating per IFO, and it looks as though the nascent stabilisation in services activity over the past couple of quarters may be giving way to renewed weakness.

- The current consensus real GDP forecast for 2024 is 0.3%, vs -0.3% in 2023, which includes a return to Q/Q growth in Q1 of +0.1% after two consecutive quarters of contraction. Further survey readings like these in the coming months could force a downward reconsideration of those forecasts.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok