Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

MNI (London)

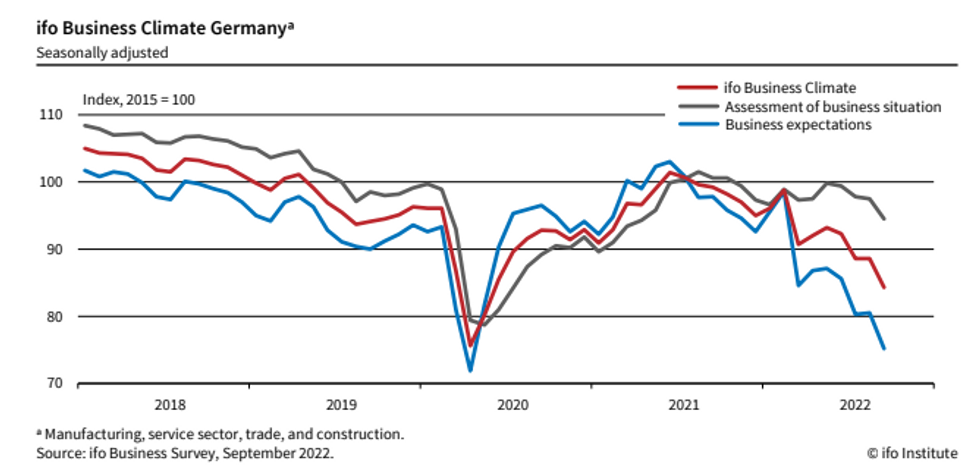

GERMANY SEP IFO BUSINESS CLIMATE 84.3 (FCST 87.0); AUG 88.6r

GERMANY SEP IFO CURRENT ASSESSMENT 94.5 (FCST 96.0); AUG 97.5

GERMANY SEP IFO EXPECTATIONS 75.2 (FCST 79.0); AUG 80.5r

- The German Ifo business survey slumped to the lowest since May 2020 as outlooks across manufacturing, services, trade and construction all fell further into pessimistic territory. Ifo continues to expect a Q3 contraction.

- The headline index, current assessment and expectations indexes again fell further than expected.

- Acute concerns regarding inflation and gas/energy supply shortages remain key issues headed into year-end. Although Friday's PMIs saw supply chain issues easing, this effect has clearly been overshadowed by gloomy economic growth outlooks.

- On Wednesday the GfK consumer confidence index will be released, likely to slide to a fresh low and generate further concern for the ECB as they hike into a recession.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok