Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

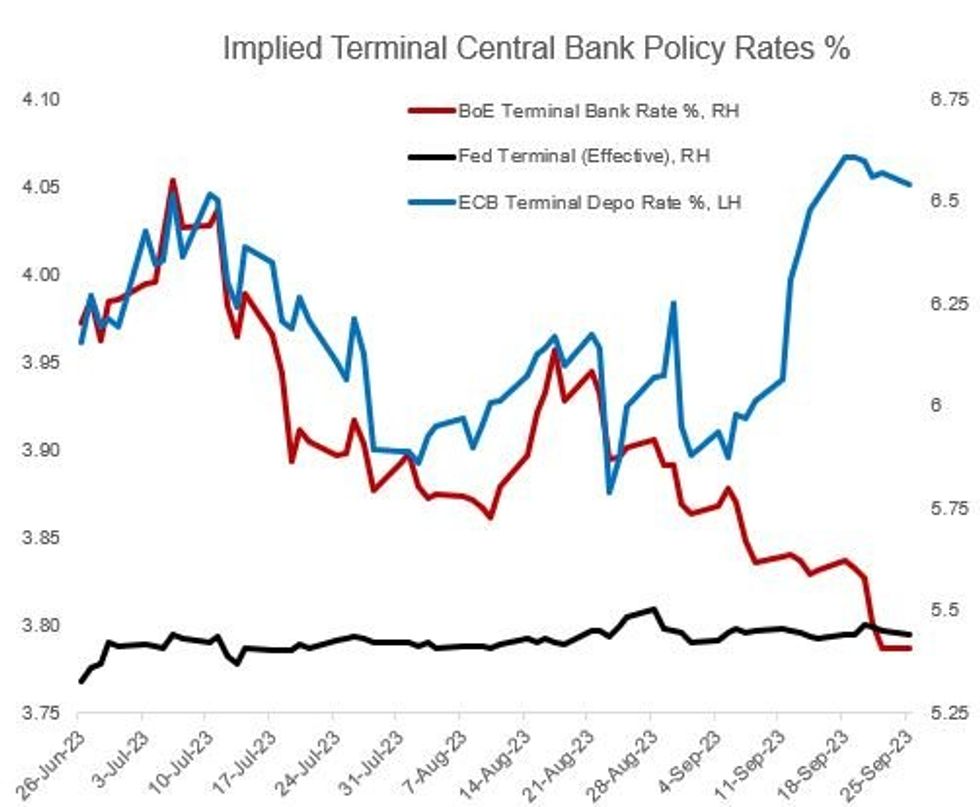

- ECB terminal rates were little changed Monday, with Pres Lagarde reiterating the guidance out of the September meeting and few macro/speaker catalysts otherwise impacting the short end. (The long-end of yield curves appears to be the pressure valve for higher-for-longer speculation for now.)

- Around 5bp of further depo hikes are seen to a December 2023 depo rate peak of 4.05%, with 62bp of cuts are seen through Dec 2024 (2bp more than seen last Friday).

- BoE terminal pricing pulled back about 2bp from session highs to close at 5.41%, implying 16bp of further Bank Rate hikes from here. Nov pricing was little changed at 9bp (around 36% prob of a 25bp hike). About 77bp of cuts are seen in the year following the peak (2bp less than seen Friday).

- As we discussed in today's Gilt Week Ahead, there are only limited catalysts on the domestic front this week, but some noteworthy events including an MNI event with BoE's Andrew Houser, and we will also hear from new MPC member Greene.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok