Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GLOBAL

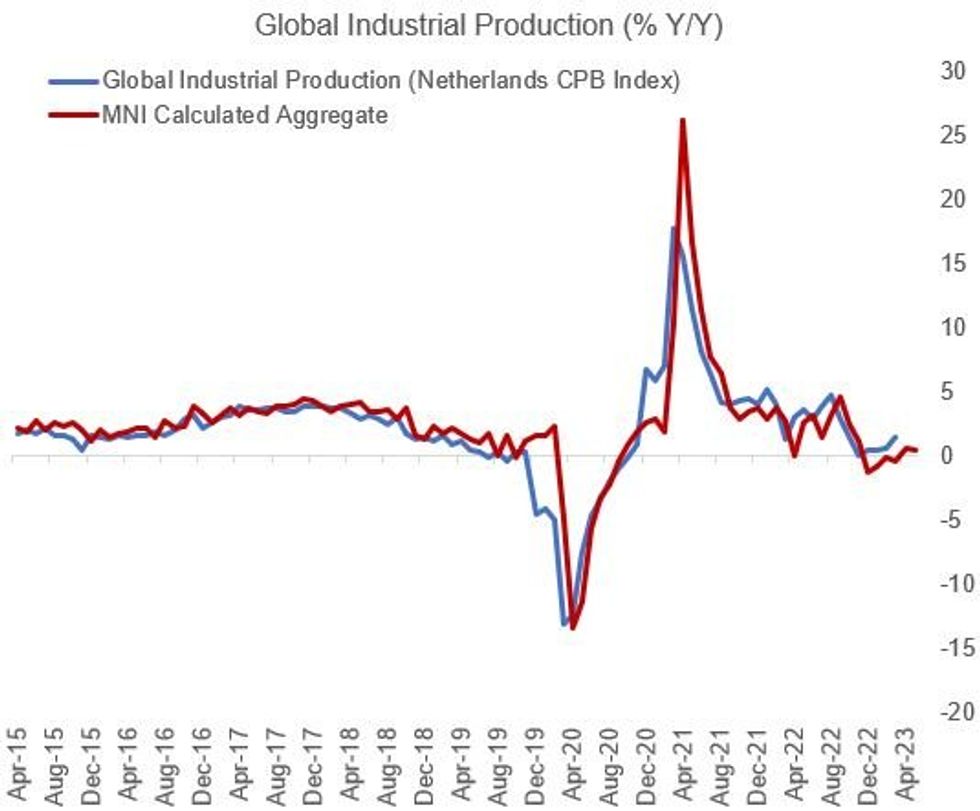

Contractions in Eurozone and UK industrial production for May out this morning were a further sign that global industry continues to struggle following a pandemic-related boom. We estimate that aggregate global industrial production grew by less than 1% in May on a year-on-year basis, meaning output has largely stayed static over the past year.

- So far the "hard data" has defied the weaker surveys, with global manufacturing PMI below 50 since September 2022. While that's not a "pure" indicator for the broader industrial complex (some of the recent IP weakness is energy sector-related), its descent has accelerated in recent months, suggesting a worse outcome.

- Resilient "hard data" is due in part to activity being maintained as supply chain-induced backlogs have been cleared out, rather than new demand. But also represents a rotation of sorts as Asian production has picked up as European/US production weakens.

- On aggregate, global industrial output is slightly lower than it was at the end of 2021, and forward looking indicators (including a 6 month global PMI low in June) provide little indication that activity will pick up in H2.

Source: CPB, MNI Calculations

Source: CPB, MNI Calculations

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok