Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

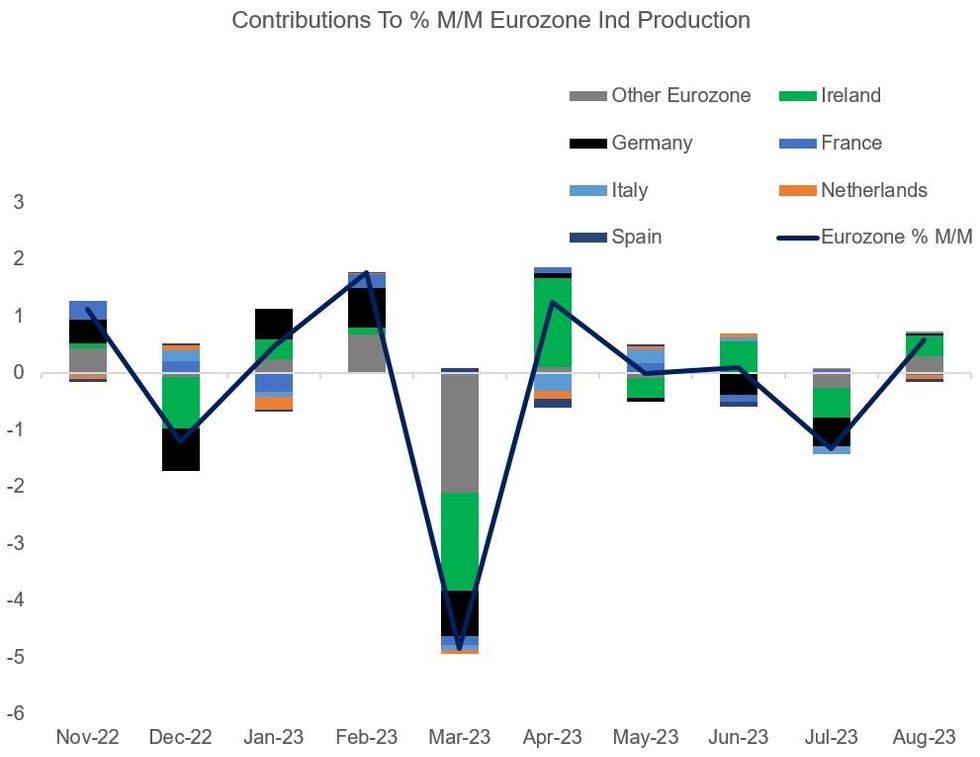

Eurozone industrial production in August saw its biggest rise in M/M seasonally adjusted terms since April (+0.6% vs -1.3% prior), with rises in durable consumer goods (+1.2% vs -1.3% Jul) and non-durables (+0.5%, same as Jul) outweighing declines in energy (-0.9% vs +1.2% Jul) and intermediate goods (-0.3% vs +0.2%). Capital goods production came in at 0.3% (-3.1% Jul).

- On an annual basis though, total industry slumped -5.1% Y/Y, with all categories in contraction (capital goods and durable goods each shrinking more than 7%).

- Once again though it's difficult to get a read on aggregate dynamics given the outsized contribution of Ireland, which saw the largest gain in Aug (+6.1% vs -9.0% prior and +9.3% in June) on a M/M basis, but also the biggest decline by far on a Y/Y basis (-27.3%).

- Excluding Ireland (which contributed 0.4pp to M/M growth), eurozone IP would have growth by roughly 0.2% M/M, the first such rise since May but not enough to offset the large declines of the previous 2 months. Germany and Italy contributed slightly to the overall M/M figure, with France, the Netherlands, and Spain dragging.

- The Y/Y figure is likewise mitigated by Ireland's outsized drag (-1.6pp) but Germany pulled the headline figure down by 0.8pp for a 2nd consecutive month, with the Netherlands, Spain, and Italy all slumping too (France was the outlier, contracting Y/Y for the first time since January).

- Overall despite the Irish statistical distortion, there is no question that Eurozone industry is in the midst of a significant and broad-based contraction, with both demand (domestically and overseas eg China) and supply (energy, labour market) constraints weighing.

Source: Eurostat, MNI Calculations

Source: Eurostat, MNI Calculations

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok