Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA DATA

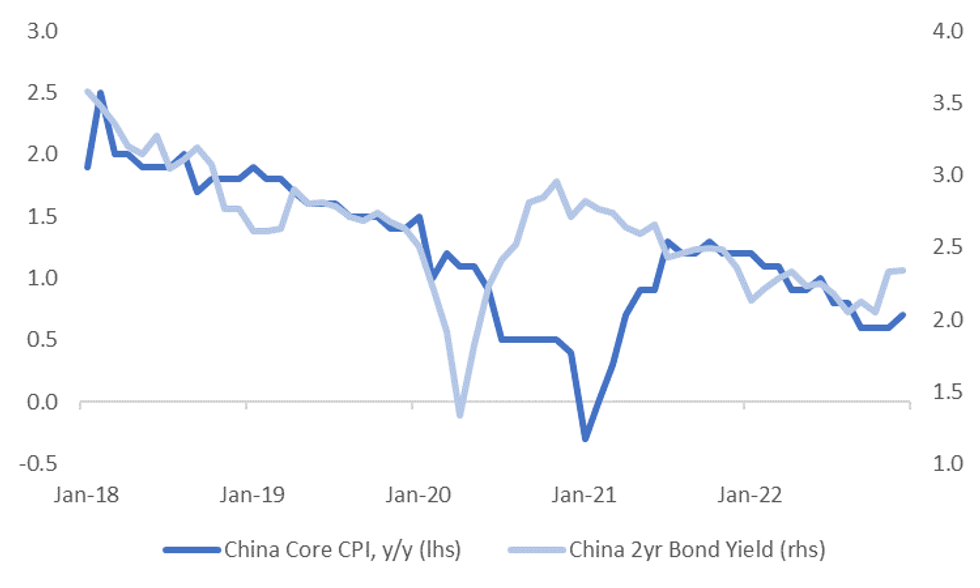

(MNI Australia) Headline inflation was at expectations, +1.8% y/y, with a flat outcome for the month (-0.2% m/m was recorded in Nov). Core inflation ticked higher to 0.7% y/y, from 0.6% prior for the past 3 months. The chart below overlays the 2yr government bond yield against core inflation.

- Food inflation pushed back to 4.8% y/y, from 3.7% prior. Interestingly of the 8 sub-components, only one (transport and communication), recorded a lower y/y pace. The rest either saw a step up in y/y momentum, or were unchanged from Nov. Non-food inflation was unchanged at 1.1% y/y though.

- The bias from some sell-side analysts is to pay China rates amid the recovery trend, although as we noted yesterday, some onshore analysts are still calling for easier monetary policy settings this year.

Fig 1: China Core Inflation & 2yr Government Bond Yield

Source: MNI - Market News/Bloomberg

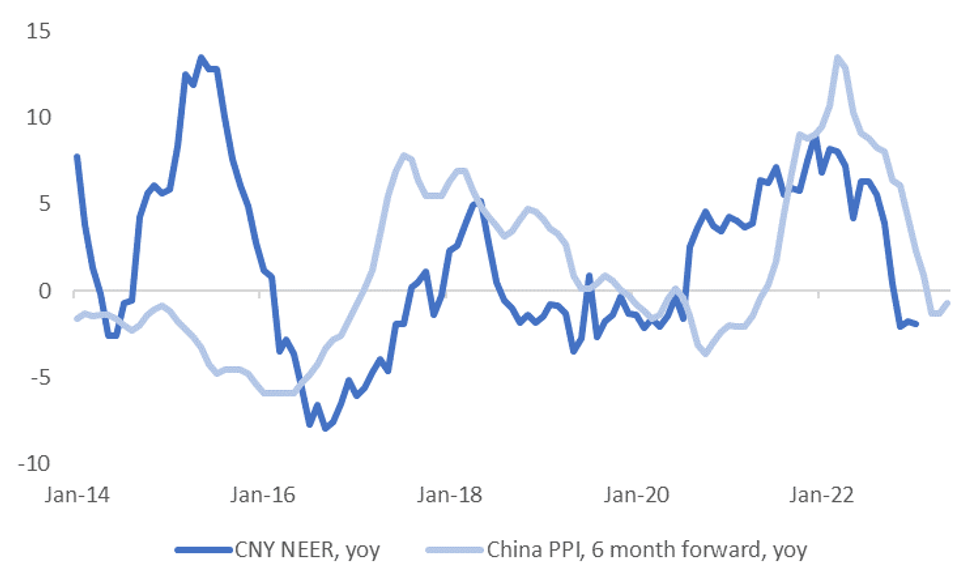

- In terms of the PPI, it was slightly weaker than expected, -0.7% y/y, versus -0.1% expected. Weakness remains in manufactured producer goods (-2.7% y/y), whilst most other segments showed improvement.

- The expectation is for a firmer upstream pulse as we progress further into 2023, aided by the shift away from CZS. This should be supportive of CNY in NEER terms (J.P. Morgan Index), see the second chart below. The NEER is already +2.8% up from late November lows.

Fig 2: China PPI & CNY NEER Y/Y (J.P. Morgan Index)

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok