Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA DATA

China headline inflation results were weaker for both CPI and PPI. Headline CPI printed at 0.1% y/y, versus 0.3% forecast and 0.7% prior. Base effects from 2022 weren't favorable, still this is the softest headline inflation outcome since early 2021. This was also the third straight month of m/m falls. At face value, this doesn't give a sense of a robust domestic demand backdrop.

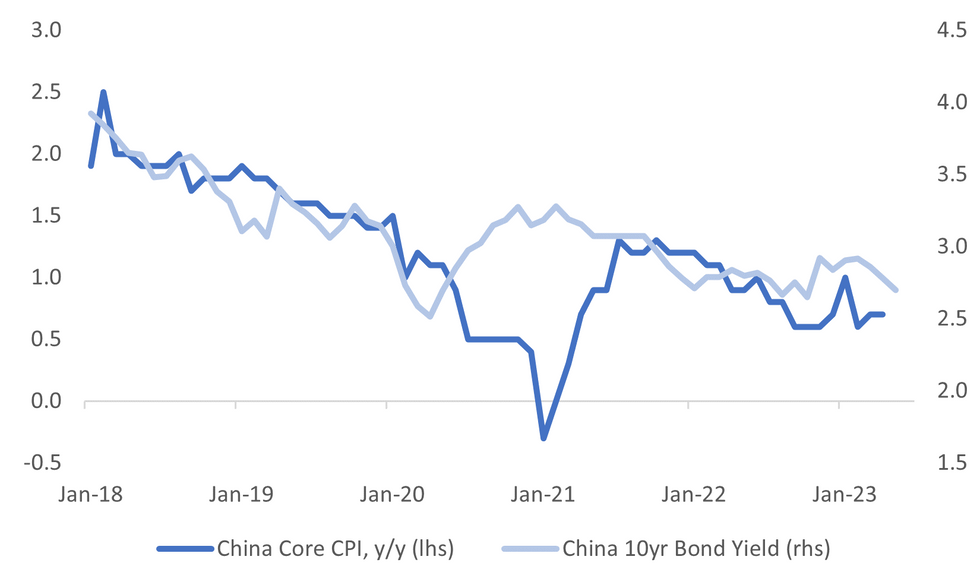

- Non-food inflation was a benign 0.1% y/y, although core (ex food and energy) was unchanged on Mar levels at 0.7% y/y. The first chart below plots the core measures against the 10yr government bond yield.

- The other detail was mixed, with transport -3.3%y/y (prior -1.9%) offset by firmer recreation at 1.9% (1.4% prior) and the others category (+3.5%, prior 2.5%).

Fig 1: China Core Inflation Versus 10yr Bond Yield

Source: MNI- Market News/Bloomberg

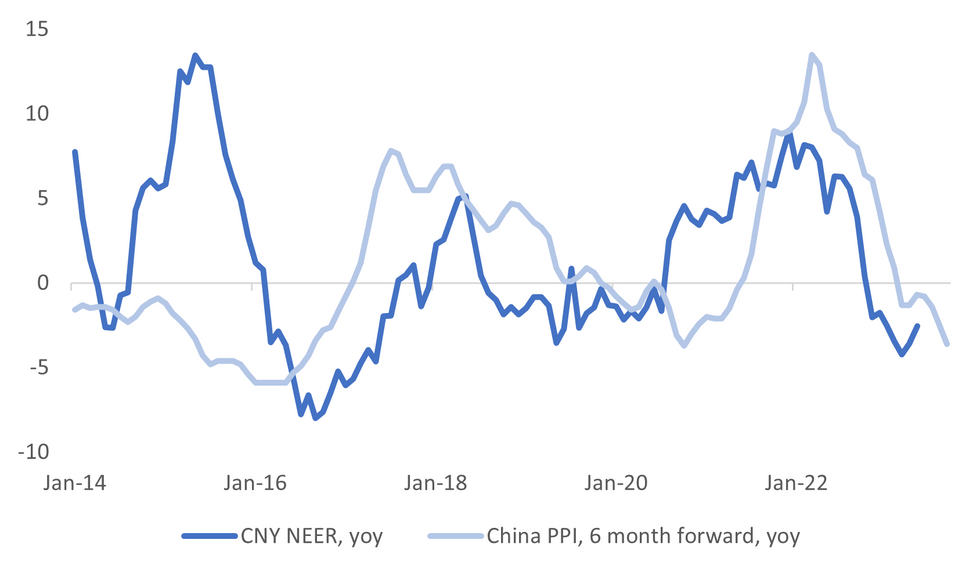

- For the PPI, we came in at -3.6% y/y, versus -3.3% forecast and -2.5% prior. Weakness was broad based, with manufacturing at -3.6% y/y, -2.8% prior. Consumer goods were 1.0% y/y (from 2.0%), weighed by durables at -0.6% y/y. Mining slipped to -8.5% y/y from -4.7%.

- The chart below overlays the CNY NEER versus the PPI y/y, which is pushed forward 6 months. The weaker PPI trend is consistent with a softer NEER backdrop. Note the CNY NEER has slipped to multi-month lows in recent sessions (per the J.P. Morgan index).

Fig 2: China PPI & CNY NEER

Source: J.P. Morgan/MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok