Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SPAIN DATA

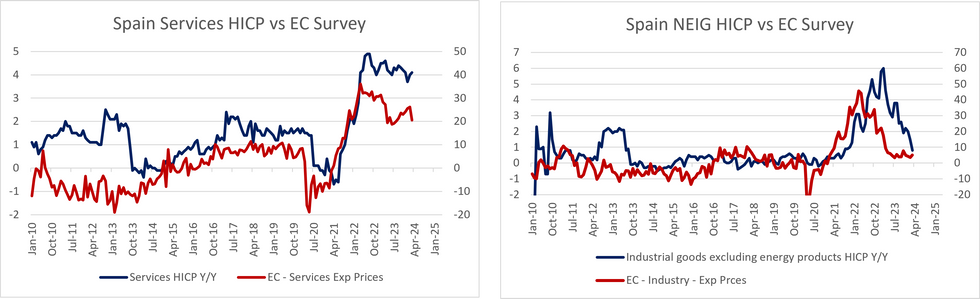

Though the final HICP reading shows Spanish core inflation receded in March, services remained sticky, printing at 4.1% Y/Y (vs 4.0% prior).

- The print comes after the Spanish services PMI continued to cite wages as a source of inflationary pressure amongst services firms in March.

- Looking ahead, services expected prices in the March EC survey fell 6.2 points to 20.6, below the 2023 average. This suggests some scope for services HICP to start moving below 4% Y/Y in the coming months.

- Despite the services stickiness, moderations in processed food inflation (4.7% Y/Y vs 5.3% prior) and non-energy industrial goods (0.8% Y/Y vs 1.5% prior) helped HICP excluding ex unprocessed food and energy fall to 3.4% Y/Y (vs 3.7% prior).

- Annual energy inflation turned positive for the first time since November 2022, at 1.6% Y/Y (vs -4.6% prior), with beneficial base effects having now fully faded.

- Spanish inflation breadth nonetheless improved in March, with the share of components with annual rates above 2% falling to 52% (vs 61% prior), the lowest since December 2021.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok