Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

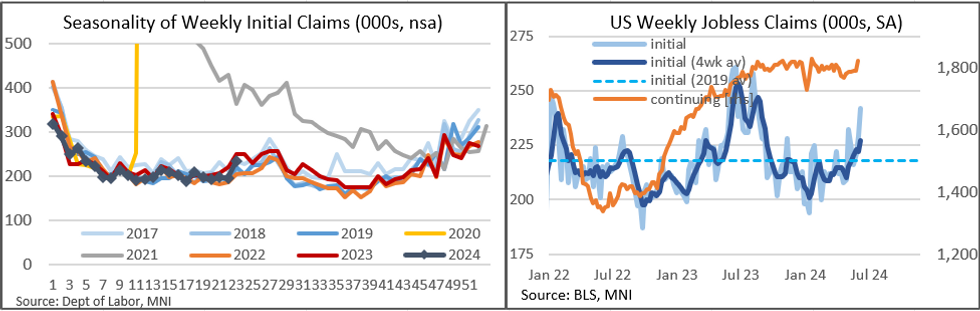

The latest weekly jobless claims report was weaker than expected, with initial claims rising 13k in the June 8 week to 242k (vs expectations of a 4k drop to 225k). Continuing claims rose much more than expected as well in the June 1 week, to 1,820k (vs 1,795k, from 1,790k reflecting a 2k revision).

- The rise in initial claims was the most for 5 weeks and takes the level to the highest since mid-August 2023. The 4-week moving average rose to 227k from 222k prior; the highest since September 2023. On an non-seasonally-adjusted basis, initial claims rose 39k, the most since the first week of 2024, to 235k.

- Th 30k increase for continuing claims was the biggest in a week since January. It's now been 6 consecutive weeks without a decline in continuing claims, and the level is likewise as high as it's been since mid-January. On a non-seasonally-adjusted basis, continuing rose 44k, again the most since mid-Jan, to 1,714k.

- State-by-state, there are a few stand-outs in the NSA insured unemployment column, including a 17.6k rise in California, 7.3k in Minnesota, 4.3k in NY, 3.8k in Washington and 2.5k in NJ, though with the exception of Minnesota most of these aren't out of the ordinary for this week of the year - the weakness looks more broad based.

- Indeed, nothing seemed out of the ordinary with the state-by-state initial claims.

- The SA figures were higher for each of the initial and continuing claims, as is typical for the adjustment this week of the year, though perhaps it looks as though the unadjusted seasonal weakness may be starting a touch early.

- Overall this is a sign of further softening in the labor market as the summer gets underway, with the Establishment survey in May's nonfarm payrolls report looking like an outlier, though claims are still at relatively low levels overall.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok