Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

JPY

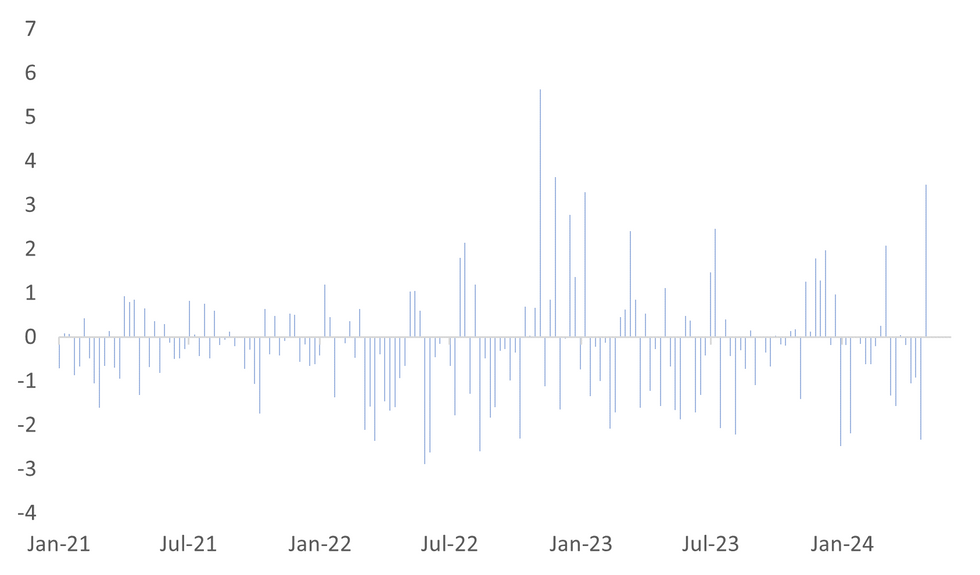

Yen gains for the past week against the USD now stand around 3.5%. This is the best weekly gain since Nov 2022, see the first chart below, as the authorities stepped in to curb yen weakness (post Monday's break above 160.00).

- Short term focus is likely to rest on whether we can see a test of the 50-day EMA at 152.39. We are already comfortably sub the 20-day EMA, at 154.58, which has highlighted the risks of a corrective cycle lower in the pair. Note that trendline support drawn from the Dec 28 low, lies at 151.05.

- Intervention estimates for this week stand at similar to those seen in 2022 (see this link). This is not to say further intervention is unlikely. The authorities have demonstrated a preference to intervene during lighter liquidity periods this past week (see this link). Japan markets are closed today and Monday so a further opportunity may present itself.

Fig 1: Yen Weekly Rate Of Change

Source: MNI - Market News/Bloomberg

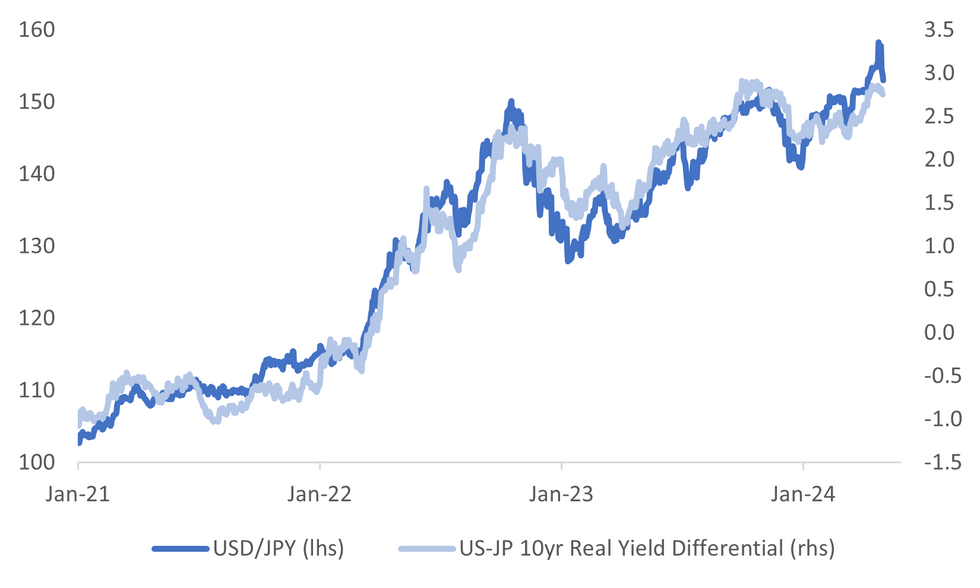

- Longer term trends for USD/JPY are still likely to be dictated by relative monetary price trends between the US and Japan. The second chart below overlays USD/JPY against the real 10yr interest rate differential.

- This week's dovish lean by the Fed has taken US yields off recent highs, although we are only just off cycle highs. The US leg of this spread will continue to dictate the overall direction, given the BoJ's likely moderate tightening cycle.

- The next litmus test will be tonight's US NFP report (see our preview here). The US Citi surprise index has tracked down sharply in the second half of April, suggesting some softening data momentum in the US. We are back close to 2024 lows for this index, although still in positive territory.

Fig 2: USD/JPY & US-JP Real 10yr Yield Differential

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok