Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA

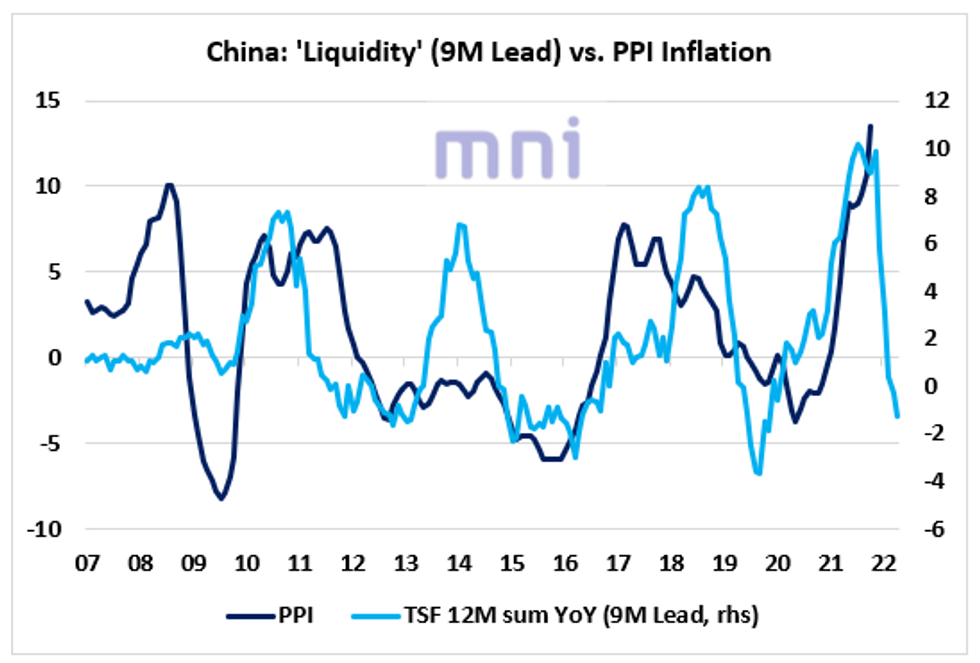

- China inflation will come out overnight (1.30 London time), with PPI inflation expected to decelerate to 12.1% YoY in November after reaching a 26-year high of 13.5% in October.

- China ‘liquidity’ (TSF 12M sum) suggests that the inflation peak is near and that we should enter into a ‘disinflationary’ period in the next 6 to 12 months.

- The chart below shows that China liquidity has strongly led PPI inflation by 9 months in the past 15 years.

- A higher-than-expected PPI print limits the room for policy easing in the medium term.

- We saw that China cut its RRR by 50bps this week to stimulate both the economic activity and asset prices (i.e. equities) and sell-side firms have been pricing in further cuts coming ahead.

Source: Bloomberg/MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok