Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SOUTH KOREA

Earlier data showed March industrial production well below expectations. We fell -3.2% m/m, against a +0.5% forecast. Feb was revised down to a 2.9% gain from 3.1% initially reported. In y/y terms, IP growth was 0.7% (+4.6% forecast). This puts IP momentum back to Q3 2023 levels.

- In m/m terms it was the largest drop since end 2022. The Stats agency noted growth was coming off a high base.

- Still, the result places downside risks to the bumper Q1 GDP result (initially reported as a 1.3% q/q rise). Overall manufacturing activity fell in quarter, but the GDP report suggested it rose 1.2%.

- In terms of the detail chip production eased in the month, but there remains a large wedge between production in this sector versus the rest of production sub components.

- Other data released shows retail spending rose 1.6%, but construction investment was down 8.7%m/m.

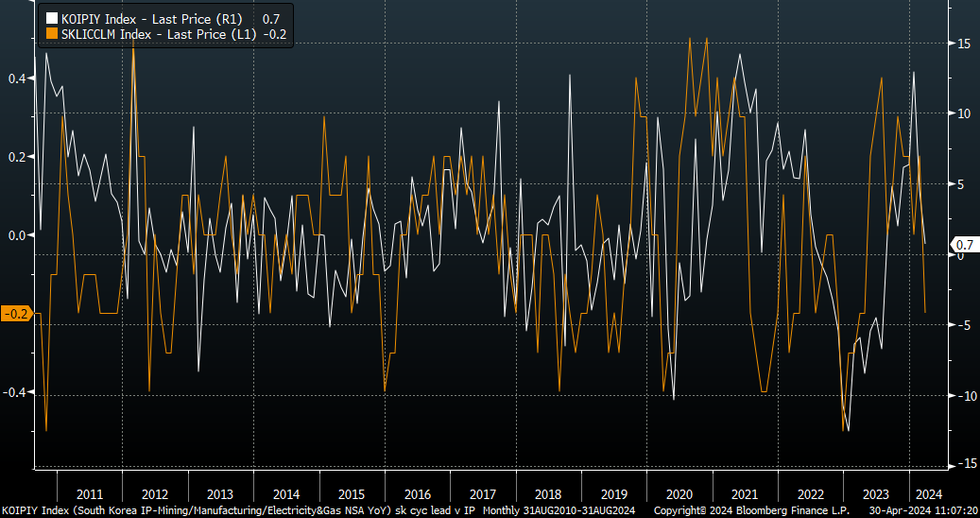

- The cyclical leading index fell to -0.2 in March from 0.2 prior. It suggests some loss of economic momentum towards the end of Q1. The chart below overlays this index against y/y IP growth.

Fig 1: South Korea Cyclical Leading Index Versus Y/Y IP

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok