Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

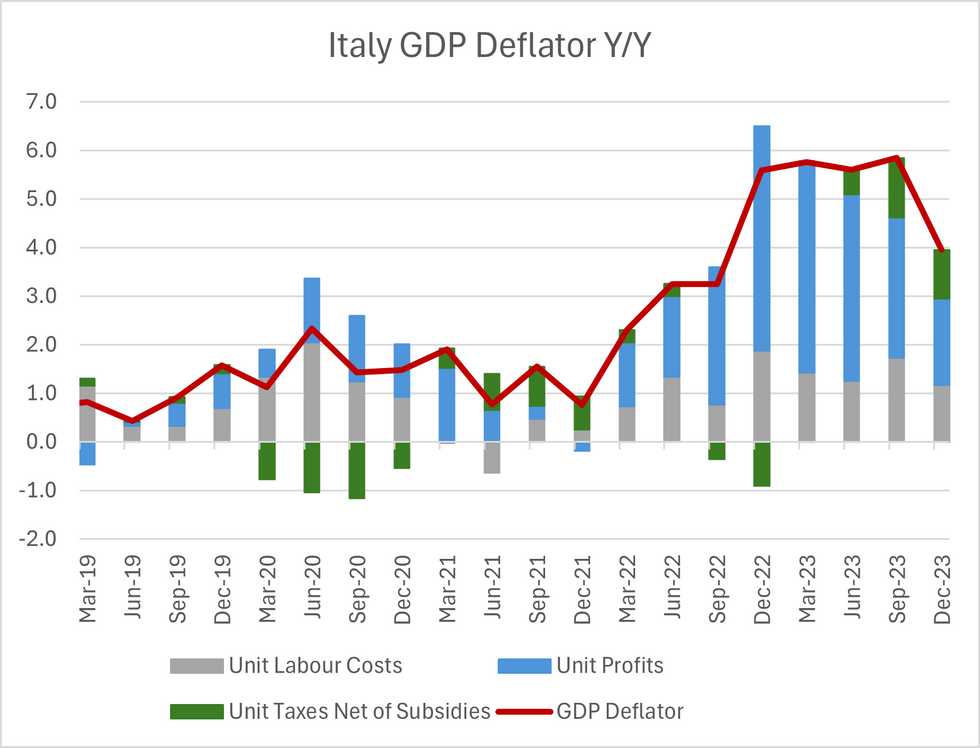

Italian real productivity per hour worked remained sluggish in Q4 2023, which pushed unit labour costs (ULCs) higher on a quarterly basis. However, a softening of annual total compensation growth meant both ULCs and the GDP deflator moderated Y/Y (to 2.9% Y/Y and 4.0% Y/Y respectively).

- For the ECB, the moderation of ULC and the GDP deflator in Italy will be taken alongside less favourable figures in other major EZ countries (e.g. in Germany and Spain, annual ULC growth remains above 6% Y/Y while GDP deflator growth is above 5% Y/Y).

- Despite this, the Q4 data is likely to be discounted in favour of looking ahead to the Q1 2024 figures at tomorrow's meeting.

- The updated macroeconomic projections will give an insight into the ECB's current view of the deflator components.

- The full Eurozone Q4 national accounts will be released on Friday March 8 at 1000GMT/1100CET.

- See the following PDF for our recent piece on EZ ULC and GDP deflator trends: https://roar-assets-auto.rbl.ms/files/60197/MNI%20Eurozone%20GDP%20Deflator%20and%20ULCs%20240301.pdf

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok