Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

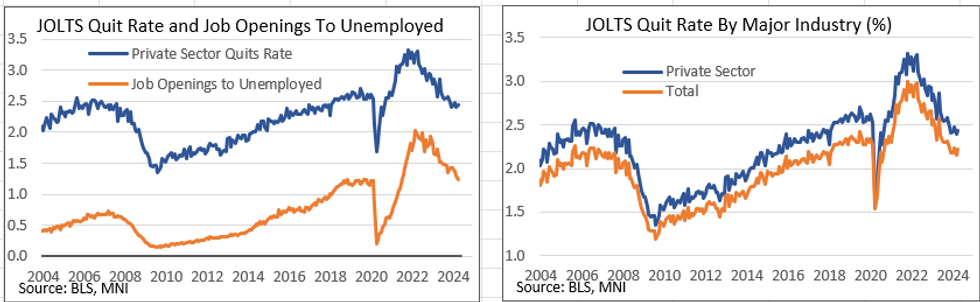

April's JOLTS report was softer than expected, showing the lowest number of job openings since February 2021, at 8.059m vs 8.355m in March (downwardly revised from 8.488m). That compares to a survey median 8.350m and represents a 2-month drop of over 750k.

- The ratio of job openings to unemployed fell to 1.24 from 1.30 prior (rev from 1.32), the lowest since September 2021. That figure averaged 1.19 in 2019, pre-pandemic.

- With March's quits rates upwardly revised by 0.1pp, the overall rate has been remarkably steady at 2.2% for 6 consecutive months; private sector quits were 2.4% for a 2nd month (had been 2.3% Mar prior to release), and the 4th month in the past 5.

- Those remain notably lower than the pre-pandemic (2019) averages for quits of 2.33% (overall) and 2.59% (private).

- Construction and manufacturing sector quit rates notably jumped, with professional/business, and "other" services falling sharply.

- The hiring rate was steady at 3.6%/private 3.9%.

- Overall the drop in openings and steady rather than rising job churn is encouraging for the doves among the FOMC heading into next week's meeting and economic projections.

- But Friday's nonfarm payrolls release will be of greater importance, not least because it is a more recent read (May) on labor market dynamics.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok