Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FRANCE DATA

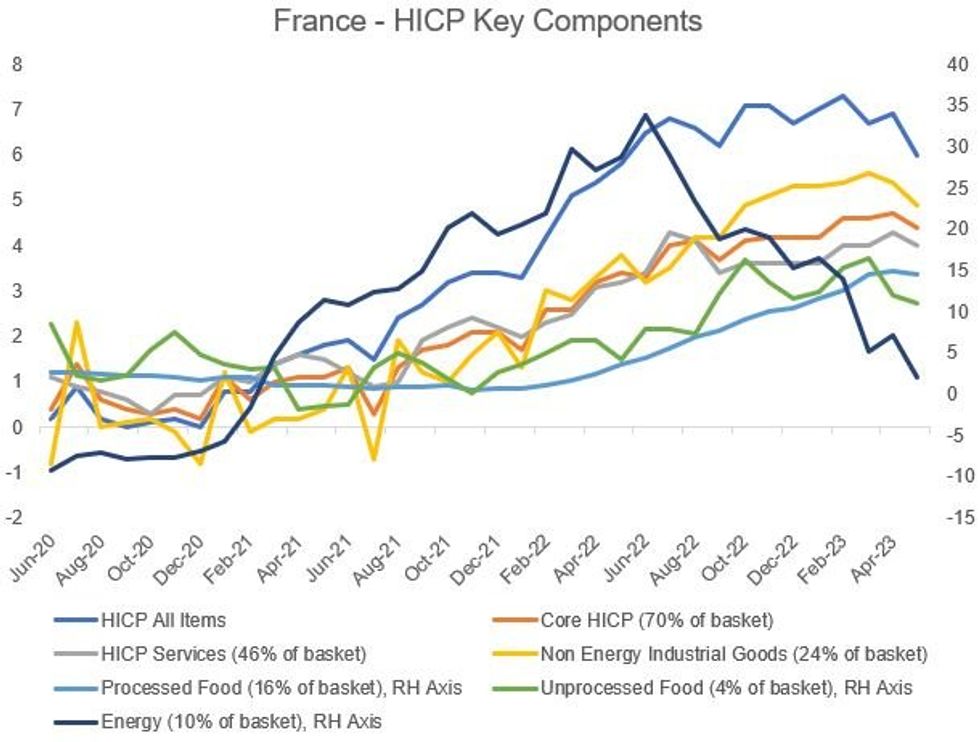

France (20% of EZ HICP) – 0745UK/0845CET Fri 30 Jun. Consensus:

- HICP: 5.4% Y/Y (6.0% prior) / 0.2% M/M (-0.1% prior)

- CPI: 4.6% Y/Y (5.1% prior) / 0.2% M/M (-0.1% prior)

- Headline Y/Y seen weaker largely on energy/base effects, though M/M pressures are set to rebound from a soft May.

- Last month's flash data surprised to the downside (HICP fell -0.1% m/m (vs +0.3% expected), whilst cooling by 0.9pp to +6.0% y/y vs +6.4% expected.

- While the flash estimate doesn't include a core reading, last month's showed a deceleration in both services and manufactured goods, which correctly flagged the softer core CPI in the final print (+5.8%, after +6.3% in April; HICP core was 4.4% after 4.7%).

- There is no analyst survey for core but the key dynamic eyed will likely be services (46% of the basket - was 4% Y/Y in HICP last time, after 4.3% in April, and in line with 4% in Mar and Feb).

Some sell-side analyst outlooks:

- JPMorgan: HICP: 5.6%. CPI 0.2% M/M, 4.6% Y/Y

- BofA: 5.6% Y/Y HICP headline (0.5% M/M), CPI 0.6% and YOY 4.9%

- Goldman Sachs: 5.4% Y/Y on -2.7% Y/Y energy driven by base effects, petrol prices. Processed food 16% Y/Y, unprocessed 8.1%. Core 4.6% Y/Y, unwinding Apr/May sequential volatility and back in line with March's pace.

- Nomura: 5.5%

- Citi: Not for this report but notes potential upside in Jul headline print as French regulated energy tariffs come to an end.

% Y/Y ChangeSource: Insee, Eurostat, MNI

% Y/Y ChangeSource: Insee, Eurostat, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok