Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SWEDEN

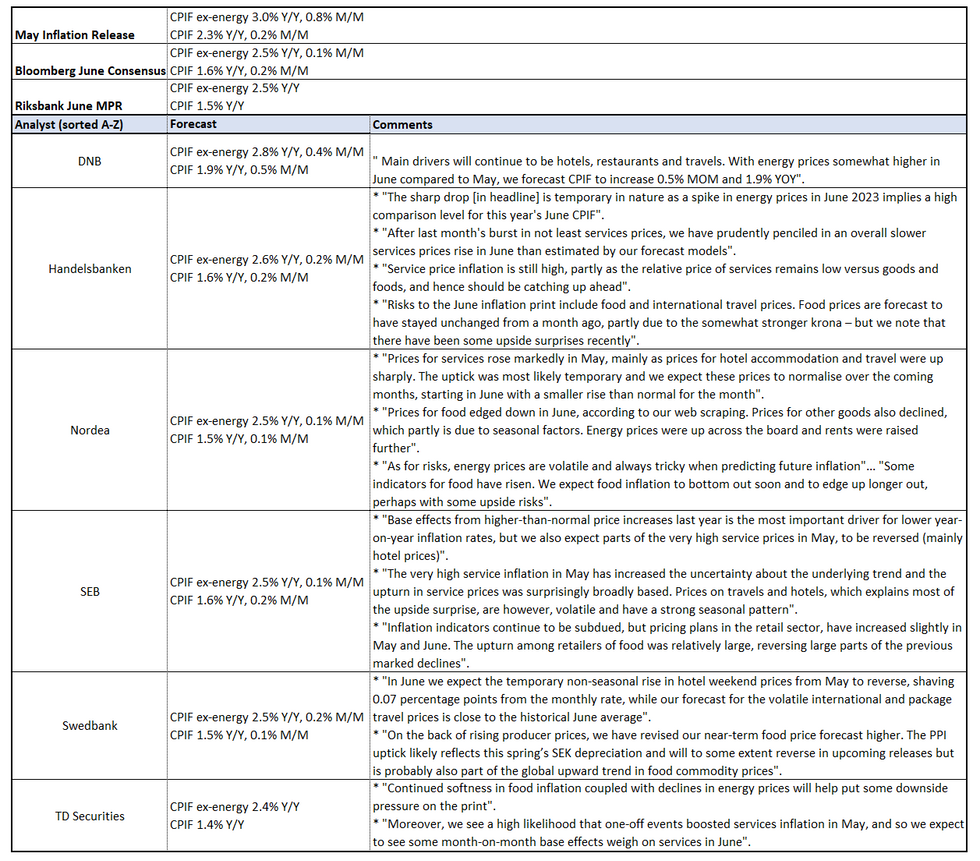

Swedish June inflation is due at 0700BST/0800CET, and is one of two inflation prints before the Riksbank’s August 20 meeting, where a 25bps cut is expected.

- We think that any upside surprise to June CPIF ex-energy inflation will need to be taken alongside the July inflation data (due August 14) before meaningfully altering market expectations for an August cut.

- Both the Bloomberg consensus and Riksbank’s June MPR expect CPIF ex-energy at 2.5% Y/Y, more-than reversing May’s acceleration to 3.0% Y/Y (vs 2.9% in April).

- A reversal of May’s rise in services inflation is expected in June. Part of the acceleration in May was due to one-off events like Taylor Swift concerts and Eurovision.

- There are mixed views on the expected contribution of food prices. A reminder that food inflation was higher-than-expected in the Norwegian June inflation print.

- Headline CPIF is seen at 1.6% Y/Y (Riksbank 1.5%, May 2.3%), primarily due to energy base effects.

- See below for a selection of analyst views:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok