Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

NZD

NZD/USD sold off sharply on Wednesday, finding support around $0.6244, as commodity markets weakened amid global recession fears. BBG Commodity Index plunged to its lowest point since April amid general aversion to take more risk.

- The rate got some reprieve in the London/NY crossover as U.S. Tsy yields extended their dip, which resulted in the widening of U.S./NZ 10-Year yield spread (already unwound this morning).

- Elsewhere, Fonterra hiked the mid-point of its farmgate milk price forecast for the 2022/23 season that started this month by $0.50 to $9.50/kg of milksolids. If this forecast is realised, it will be a new all-time high. And it would come on top of a record 2021/22 season, when the final price is expected to settle around NZ$9.30.

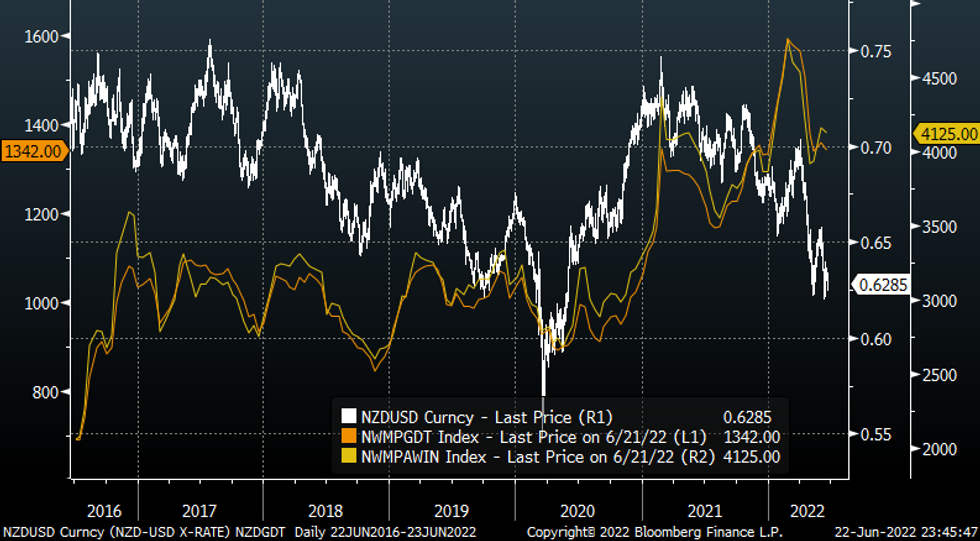

- The kiwi dollar has shown little reaction to these developments, as usual. While typically its initial reaction is limited, the chart below shows that there has been a degree of co-movement in NZD/USD and dairy prices in the medium term, particularly over the last two years or so.

- The rate last deals at $0.6287, little changed on the day. Losses past Jun 14 low of $0.6197 would signal potential for a move below $0.6000. Conversely, a rebound above Jun 16 high of $0.6396 would shift bullish focus to key resistance from Jun 3 high of $0.6576.

- The local economic docket is virtually empty during the remainder of the week.

Fig. 1: NZD/USD vs. New Zealand GDT Price Index vs. New Zealand GDT WMP (Whole Milk Powder) Average Winning Price

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok