Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

NZD

NZD/USD has lost a little more ground as the morning session has progressed. The pair was last at 0.6210/15, around -0.20% below NY closing levels. This is line with the rest of G10 (ex JPY), which is mostly tracking softer versus the USD, although NZD and NOK are modestly underperforming. In terms of downside levels, lows near 0.6180 were supported on Monday.

- Locally, the ANZ activity outlook for March improved slightly to -8.5 from -9.2, while business confidence edged down to -43.4 from -43.3. This followed the earlier 9% slump in Feb building approvals (-9%), which are back to mid 2020 ranges from a levels standpoint.

- These releases continue to suggest a challenging activity backdrop ahead of next week's RBNZ meeting, although market pricing remains at +25bps for the meeting.

- Cross asset signals are fairly muted, with US equities down a touch, while US yields have firmed slightly.

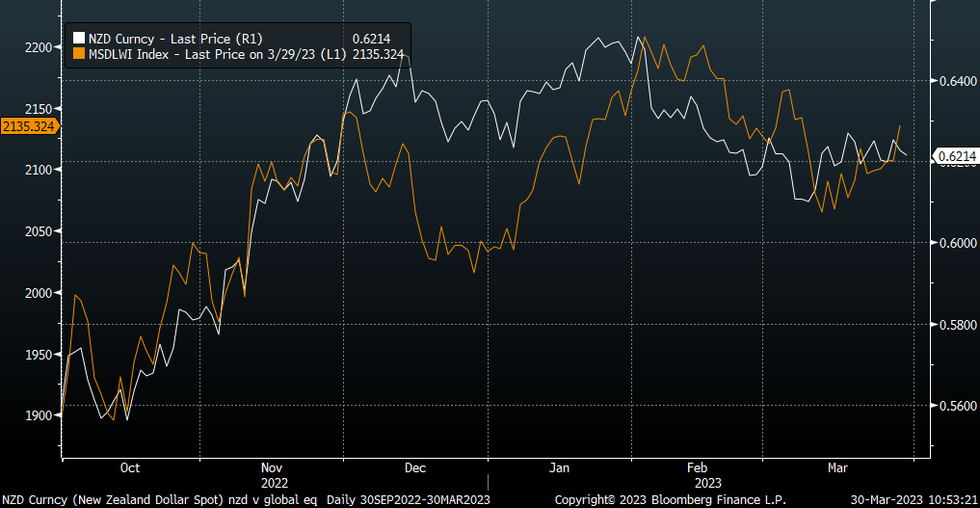

- NZD/USD has lagged the better equity tone globally since the start of the week, see the chart below, although the divergence is modest at this stage.

Fig 1: NZD/USD Versus Global Equities

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok