Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

ASIA FX

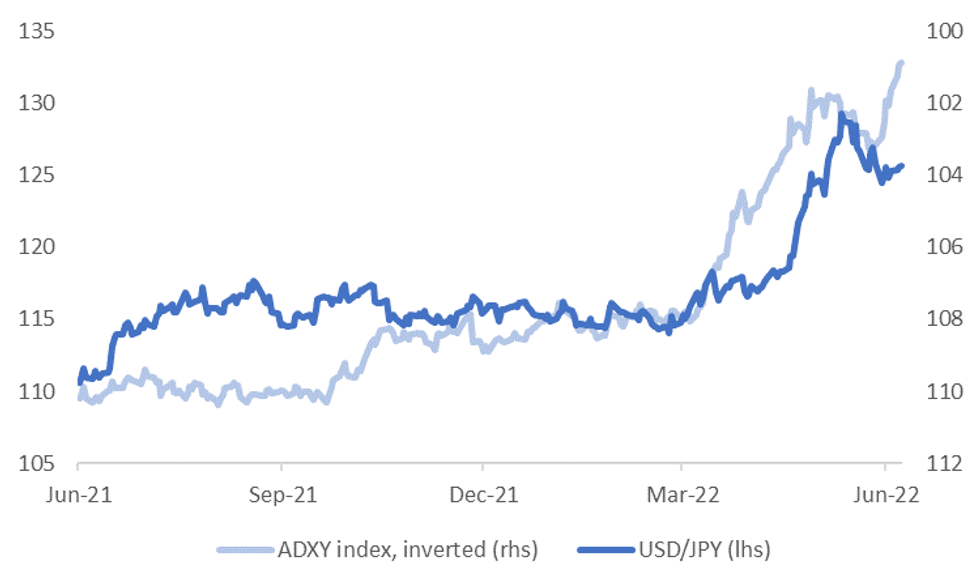

All of Asia FX has outperformed the JPY sell-off this year. That's not to say higher USD/JPY moves can't influence USD/Asia pairs. As we outline below, correlations this year between USD/JPY and Asian FX have generally been positive, although more so for North East Asia FX and currencies with strong trade links to Japan, such as THB and PHP.

- The first chart below overlays USD/JPY against the ADXY index, which is inverted on the chart.

- The ADXY has only fallen modestly during the recent surge higher in USD/JPY. Still, higher USD/JPY levels can still influence USD/Asia pairs, even if we see this relative divergence persist.

Fig 1: USD/JPY & ADXY Trends

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

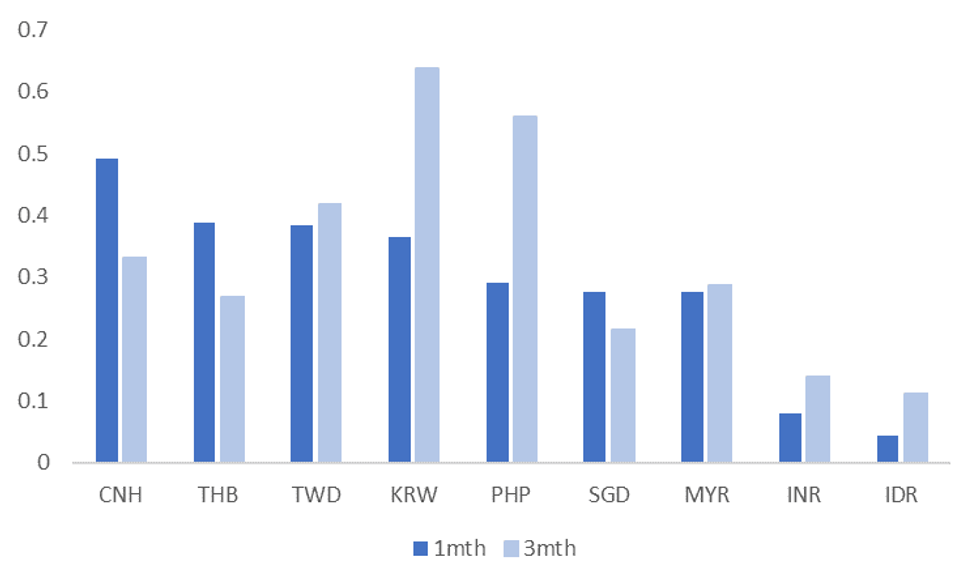

- The second chart below plots the average correlations between USD/JPY and all the major USD/Asia pairs for 2022. We do this for both rolling 1 month and 3 month correlations.

- Correlations are higher for north east Asia currencies, like CNH, TWD and KRW. They are also elevated for THB and PHP. Yen weights in trade weighted indices for THB and PHP are quite high at 15.7% and 15.3% respectively. They are also high for the NEA bloc.

- As we have also noted in relation to KRW, Japan represents export competition for Korea and other NEA economies to some extent. So, a weaker yen will leave the respective central banks mindful of reduced competitiveness.

- Correlations are lower for INR and IDR. For INR, trade linkages are much lower with Japan compared to the rest of the region. For IDR trade linkages are quite high, but relative IDR/JPY performance may be more influenced by capital flows, particularly in relation to carry trades, given IDR's high yielder status relative to JPY.

Fig 2: USD/JPY & USD/Asia Average 2022 Correlations

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok