Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

ASIA FX

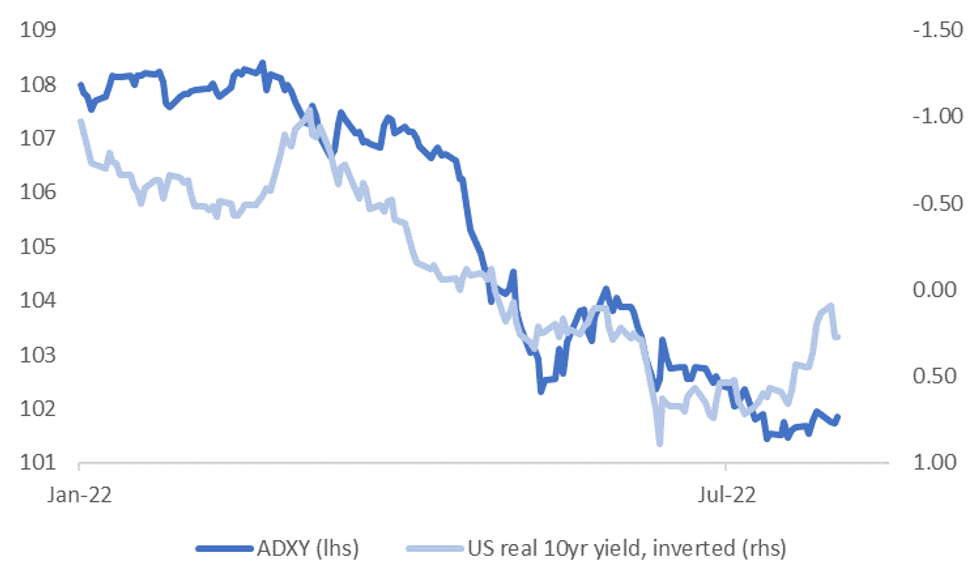

While the near term focus remains on US-China geopolitical tensions and China military exercises around Taiwan, the overnight bounce in US yields has the potential to undermine the recent outperformance in South East Asia (SEA) and INR FX.

- The chart below updates a recent one we produced of the J.P. Morgan Asian currency index (ADXY) against the real US 10yr yield (which is inverted on the chart). From July 20th to the start of the month we saw a sharp drop in the US real yield from +60bps to +9bps, although this was reversed somewhat overnight (back to +27bps).

- The ADXY didn't rally much with this move lower in real yields, as the index is heavily weighted to CNY, which has arguably been driven more by geopolitics in recent weeks.

Fig 1: ADXY & US Real 10yr Yield

Source: MNI/Market News/Bloomberg

Source: MNI/Market News/Bloomberg

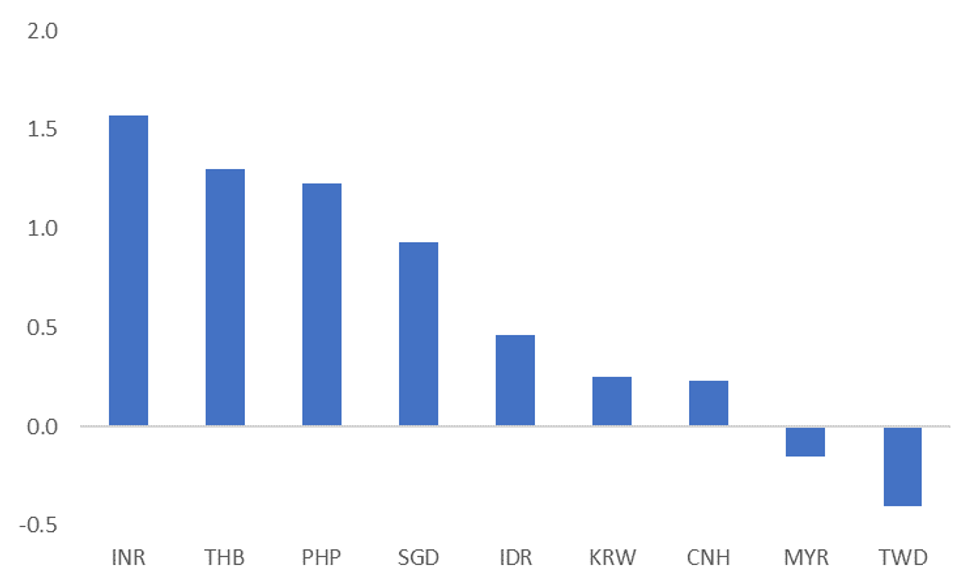

- The benefit was clearer for other Asian FX though, particularly in SEA/INR. The second chart below plots spot returns since that most recent peak in the real 10yr yield (July 20th).

- Stronger gains were seen in economies typically more sensitive to shifts in Fed policy, although this wasn't uniform, whilst TWD underperformance over this period is likely tied to Pelosi's visit.

- Still, gains have slowed in the likes of THB, PHP, IDR and INR today, with higher US yields no doubt a factor. Relative performance trends in Asian FX is something to be mindful of amidst on-going shifts in the US outlook.

- Fig 2: Asian FX Returns Since Recent Peak In US Real Yield (July 20th)

Source: MNI/ Market News/Bloomberg

Source: MNI/ Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok