Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SWEDEN

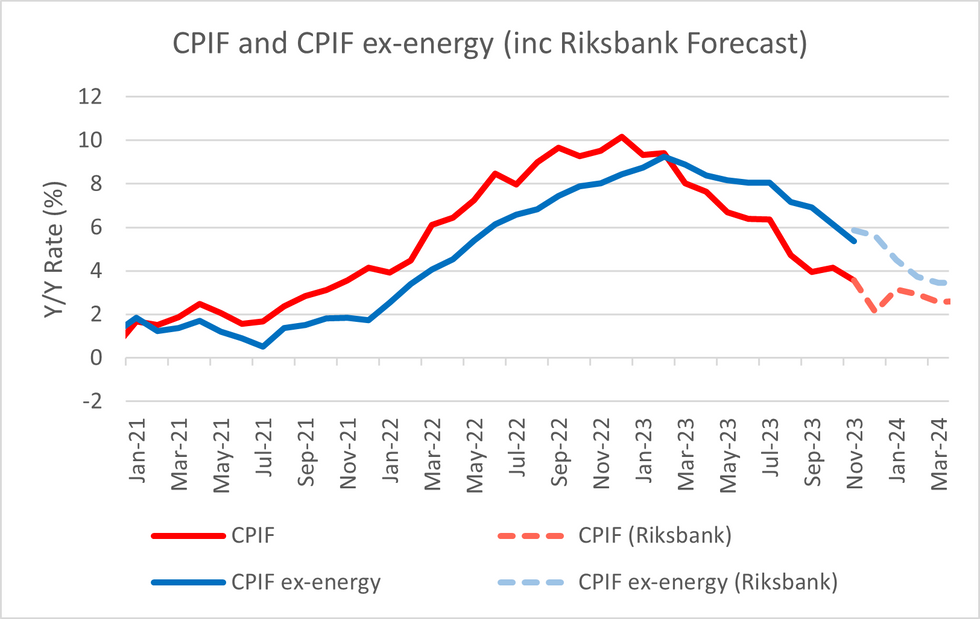

Sweden November CPI came in lower-than-expected on both the core and headline readings, further justifying the Riksbank's decision to hold rates last meeting.

- USDSEK AND EURSEK have risen 0.2% since the release - the somewhat muted reaction represents consensus views that the Riksbank has finished hiking even if inflation had surprised to the upside in November, but also that some of the downside surprise was likely due to the volatile package holidays component.

- CPIF ex-energy was an unrounded 5.37% Y/Y (vs 5.9% cons, 6.1% prior) and -0.55% M/M (NSA, vs -0.1% cons, 0.1% prior) . The Riksbank had forecasted core inflation at 5.86% Y/Y in its November MPR projections.

- Headline CPIF was 3.57% Y/Y (vs 3.9% cons, 4.2% prior) and 0.15% M/M (vs -0.5% cons, 0.1% prior).

- Electricity prices rose on a monthly basis as expected by analysts but seemingly less than forecast, still printing at -22.5% Y/Y.

- Package holidays fell -19.2% Y/Y. Package holidays are a volatile component, though, and the Riksbank has tended to look at measures of core inflation excluding international travel in its analysis.

- The fall in package holidays meant that the recreation and culture component inflation fell to 7.56% Y/Y (vs 9.80% prior), while restaurants and hotels also disinflated to 6.06% Y/Y vs 6.75% prior).

- All in all, the package holiday component was likely responsible for some of the downside surprise. However even without this, the broad-based nature of the slowdown in other core components likely would have seen inflation surprise to the downside.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok