Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

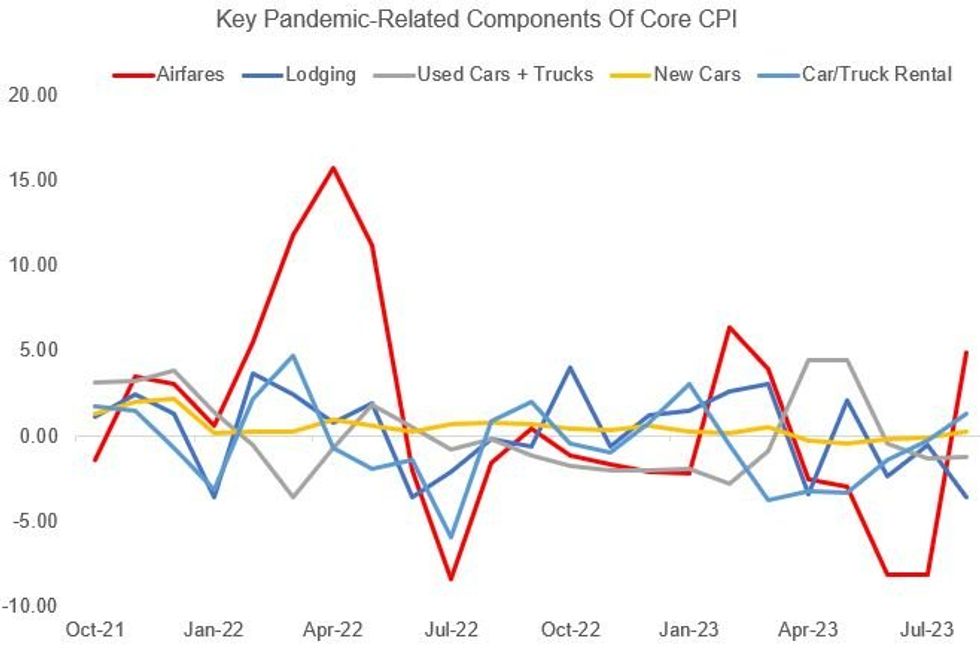

While the Covid pandemic continues to fade into the rear view mirror, volatility in multiple pandemic reopening categories of the CPI basket continue to have an outsized impact on month-to-month dynamics. August was mixed in this regard, but overall these line items dragged on CPI a little less (-0.03pp) than they did in July (-0.08pp), with a few categories bucking recent deflationary trends.

- As noted earlier, the standout among the pandemic reopening categories was Airfares which helped push supercore services prices higher with a rise of 4.9% M/M in August - the 2nd biggest increase since May 2022 and a little more than expected - after 4 consecutive monthly contractions. With that increase, airfares are 6% below pre-pandemic levels and 23% below the pandemic peak. (By comparison, the CPI basket as a whole is +18% vs Feb 2020).

- Lodging prices dropped the most since April (and much more than analysts had expected at -3.0% M/M) for the 4th drop in 5 months. They remain 9% higher vs pre-pandemic levels but 6% below peak.

- Used cars and trucks deflated for the 3rd consecutive month at -1.2% M/M, in line with expectations; prices are now 40% higher vs pre-pandemic levels in Feb 2020, but 10% below peak.

- New car prices ticked higher by 0.2% M/M (expectations on this category were mixed) after 4 consecutive declines and have essentially flatlined for the past 10 months. They're 1% below peak - but 20% above pre-pandemic prices.

- Car/Truck rental prices meanwhile picked up for the first time since January at +1.3% M/M. That leaves them 20% below peak levels but 25% up from pre-pandemic.

% M/M SASource: BLS, MNI

% M/M SASource: BLS, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok