Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

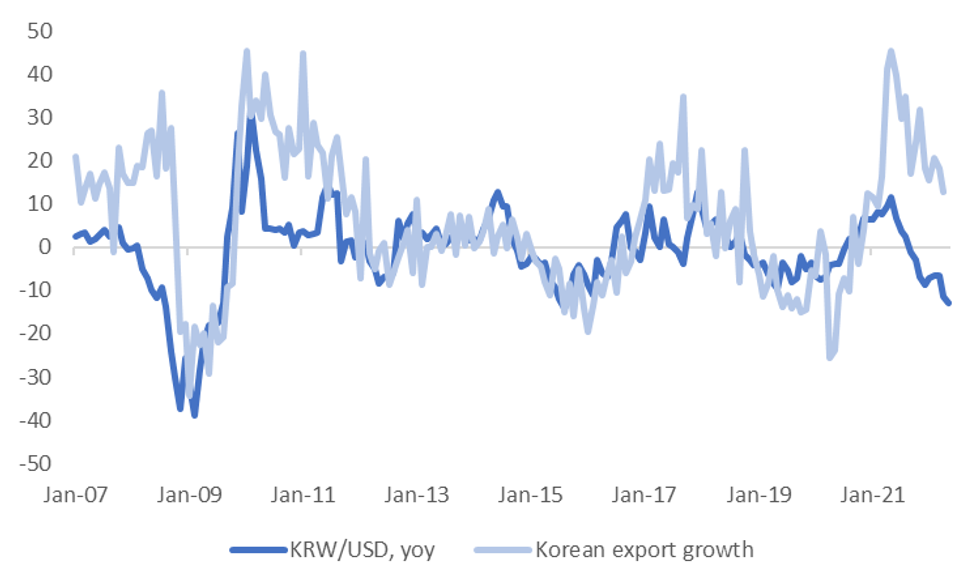

KRW

KRW has fallen too much relative to export growth, but there are factors that suggest this divergence can persist

- The chart below plots KRW/USD YoY versus Korean export growth. Historically, the correlation has been a tight one. However, YoY momentum for KRW looks far too weak relative to the current export trend, even assuming export growth slows further in May.

- There are a number of potential factors driving this divergence. The first is that the market is pricing in a sharp slowdown in export growth for Korea in the months ahead, hence weaker won levels.

- However, it's also important to highlight the trade deficit, which we did in an earlier post. The last meaningful trade deficit period for Korea was in 2007/2008 period, which also coincided with a breakdown in the relationship between exports and KRW performance.

- The Korean authorities may also be keeping an eye on export competitiveness, given JPY has fallen nearly 12% YTD, versus the won's fall of 7%.

- Domestic investors (both retail & institutional) continue to pressure the KRW from a capital flows perspective, particularly the National Pension Service, which is allocating more assets offshore. Such 'recycling' outflows will weaken the won all else equal, as the funds typically leave Korea on an FX-unhedged basis.

- Such factors could keep the divergence between KRW & export growth in play for sometime yet, although we would still expect the directional correlation between KRW and export growth to remain fairly strong.

Fig 1: KRW Looks Too Weak Relative To Export Trend

Source: MNI/Bloomberg

Source: MNI/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok