Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

KRW

Spot USD/KRW continues to push higher, with the won not seeing much benefit from a slightly weaker USD against the majors. We were last at 1267.25, with weaker onshore equities and continued net equity outflows remaining meaningful headwinds.

- Today has seen the Kospi dip a further 1.40%, while offshore investors have sold an additional $519mn in local equities so far. This comes on top of the $837 sold yesterday, which was the largest net daily outflow since early April.

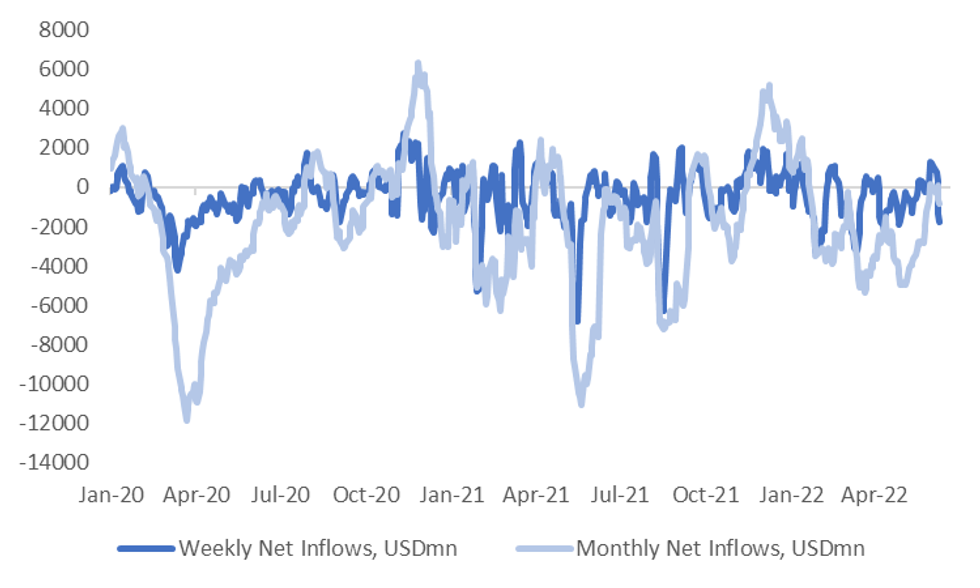

- The first chart below shows the rolling weekly and monthly net inflow trends. The past 5 trading sessions has seen just over $1.7bn in net outflows. For the past month it is a more modest -$858mn in net outflows.

- We did see a burst of positive inflow momentum at the end of May but this clearly hasn't carried over into June.

Fig 1: South Korean Equity Outflows Persist

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

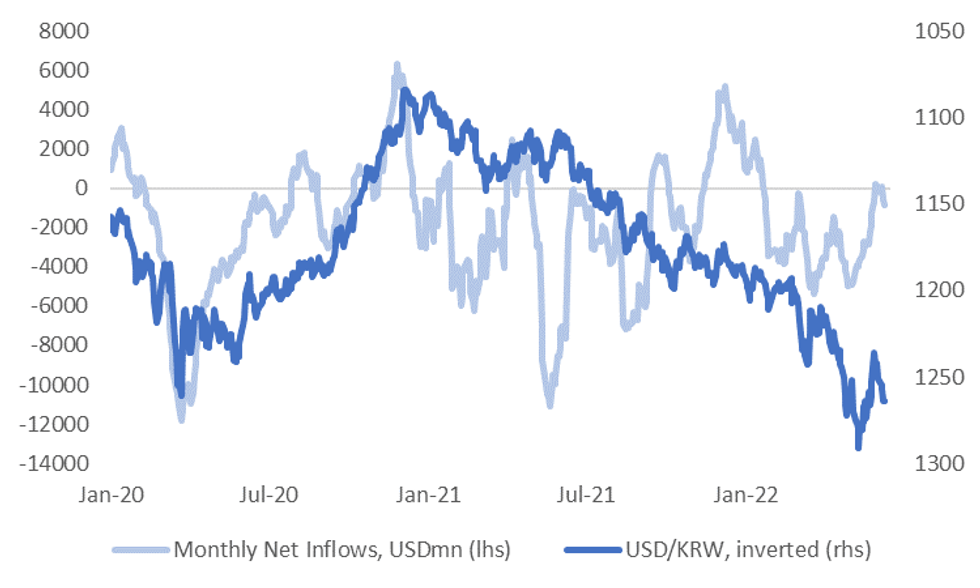

- Correlations between USD/KRW and equity flows remain fairly strong at the moment. The second chart plots USD/KRW, which is inverted on the chart, and the rolling monthly net inflow trend.

- If we see a period of sustained outflow momentum this could coincide with USD/KRW revisiting earlier highs of close to 1290, which would likely test the resolve of Korean authorities around FX stability.

- For flow prospects to improve, equity sentiment needs to be on a better footing, particularly in the tech space. Correlations between Korean equity inflows and local equities sits above 80%, likewise for the SOX semiconductor index and the MSCI IT index.

- These sectors haven't been able to sustain upturns this year, with tighter global monetary policy conditions and concern around the demand outlook weighing.

Fig 2: USD/KRW & Net Equity Inflows, Rolling Monthly Total

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok