Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SGD

The list of sell-side analysts calling for an out of cycle MAS tightening is growing. This should keep the SGD NEER close to the top end of the policy band

- To recap, yesterday's May inflation data showed headline inflation pressures stronger than expected. MoM rose by 1.0%, YoY by 5.6%, both 0.1% firmer than consensus. Core inflation came in as expected, but at 3.6% YoY is still the firmest pace since 2008.

- Earlier this week the government unveiled a support package worth $S1.5bn to combat cost of living pressures for low income households. Hence addressing inflation pressures remains front and centre for policy makers.

- As we noted earlier the rate of SGD NEER appreciation (just over 3% for the past year) is still lagging the rate of inflation.

- J.P. Morgan expects a tightening, via a re-centering of the NEER, after the next CPI print on July 25th. They also don't rule out a steeper rate of NEER appreciation.

- Such a backdrop should leave the SGD NEER biased higher and close to the top end of the policy band ahead of any such risk of a policy adjustment.

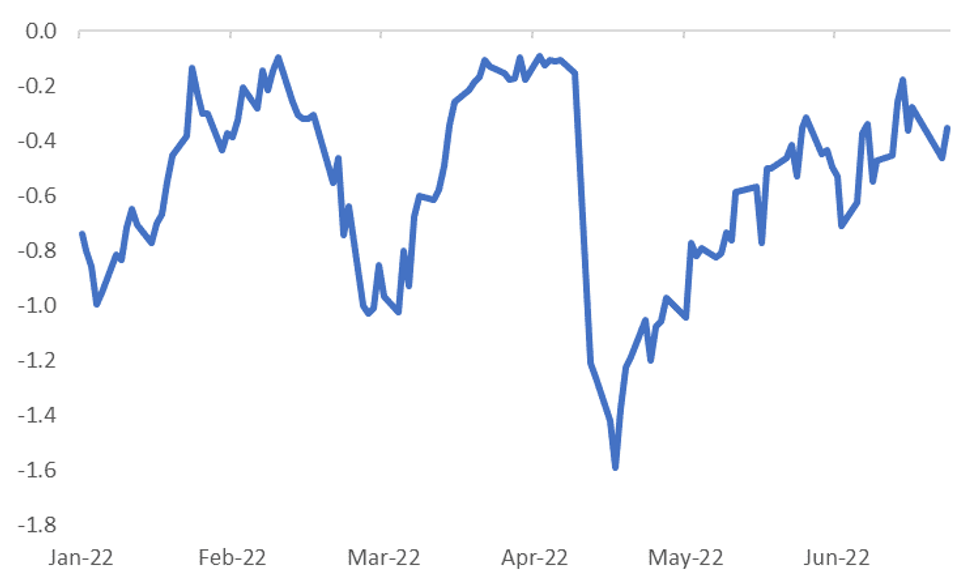

- The chart below plots the NEER deviation from the top end of the band, based off Goldman Sachs estimates. We currently sit 0.35% below the top end of the band, which is modestly lower than earlier YTD highs.

Fig 1: GS SGD NEER - Deviation From Top End Of The Policy Band (%)

Source: Goldman Sachs, MNI - Market News

Source: Goldman Sachs, MNI - Market News

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok