Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

KRW

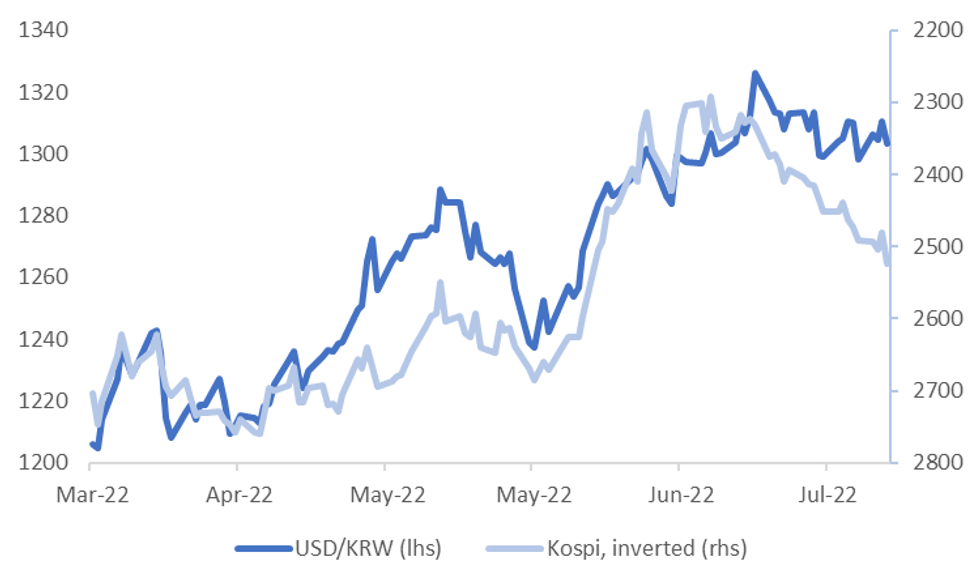

1 month USD/KRW got back below the 1300 level post the Asia close but couldn't sustain this breach. From just under 1298 the pair rebounded to 1308, before settling back to 1306 into the close. Note onshore spot ended onshore trading at 1303.2 yesterday.

- The turn around in USD/KRW coincided with a broader USD rebound. Softer equity sentiment in US markets into the close didn't help either. The SOX and MSCI IT indices giving up some of the previous session's gains.

- To recap, the Kospi had a solid session yesterday, up 1.73%, with offshore investors adding just under $160mn in local shares.

- Such a backdrop is widening the wedge between FX and equities, see the chart below, although onshore equities may unwind some of yesterday's bounce today.

- On the data front, earlier trade price prints for July showed drops in the month. The YoY paces also slowed, but import prices (+27.9%) still remained firmer than export prices (16.3%).

- China-South Korea tensions could also be in focus. The Yoon administration has stated the deployment of the THAAD missile defence system is a 'non-negotiable'. This comes after the previous Moon administration paused the deployment of the system in South Korea. China views the system as a threat to its security.

- Note that South Korea markets are closed on Monday for the Liberation Day holiday.

Fig 1: USD/KRW & Local Equity Trends

Source: MNI/Market News/Bloomberg

Source: MNI/Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok