Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HEALTHCARE

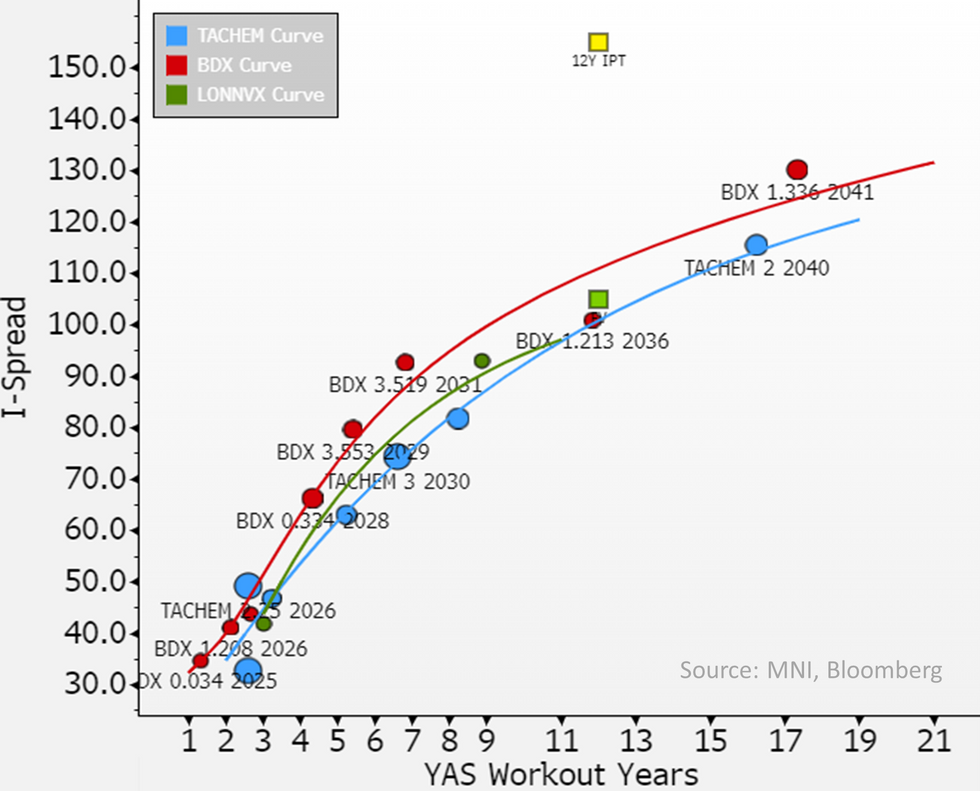

12Y IPT MS+155a vs. our FV of +105 - IPT is tad wide here. Our FV is +5 above both reverse Yankee BDX 36's and wide of the equal rated Japanese pharma Takeda. Comparisons of fundamentals below, Lonza does have cleanest BS but smallest scale and will run leverage up on rating headroom.

- BDX & Takeda are larger in scale ($20b+ vs. $8b for Lonza) - BDX operates as manufacturer of medical supplies, devices & laboratory equipment. Lonza & Takeda are more traditional pharma.

- Both BDX & Lonza run similar EBITDA margins (high 20s), healthy FCF for BDX & Takeda, while Lonza is more mixed as it runs sizeable capex given headroom on leverage (0.5x vs. target 1.5-2x, committed to current ratings) - it is guiding to bolt-on M&A down the road as well.

- BDX is more conservative with net leverage 2.7x vs. target 2.5x & Takeda coming off post-acquisition deleveraging & a one-notch upgrade currently at 3.1x. All 3 stable rated, Lonza & Takeda one-notch higher. We don't see near term rating risk for any, obviously dependent on acquisitions.

- Next earnings; BDX 2Q24 on 2nd of May (US pre-market), Takeda 4Q23 9th of May (Japan close), Lonza 1H24 in late July.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok