Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SWEDEN

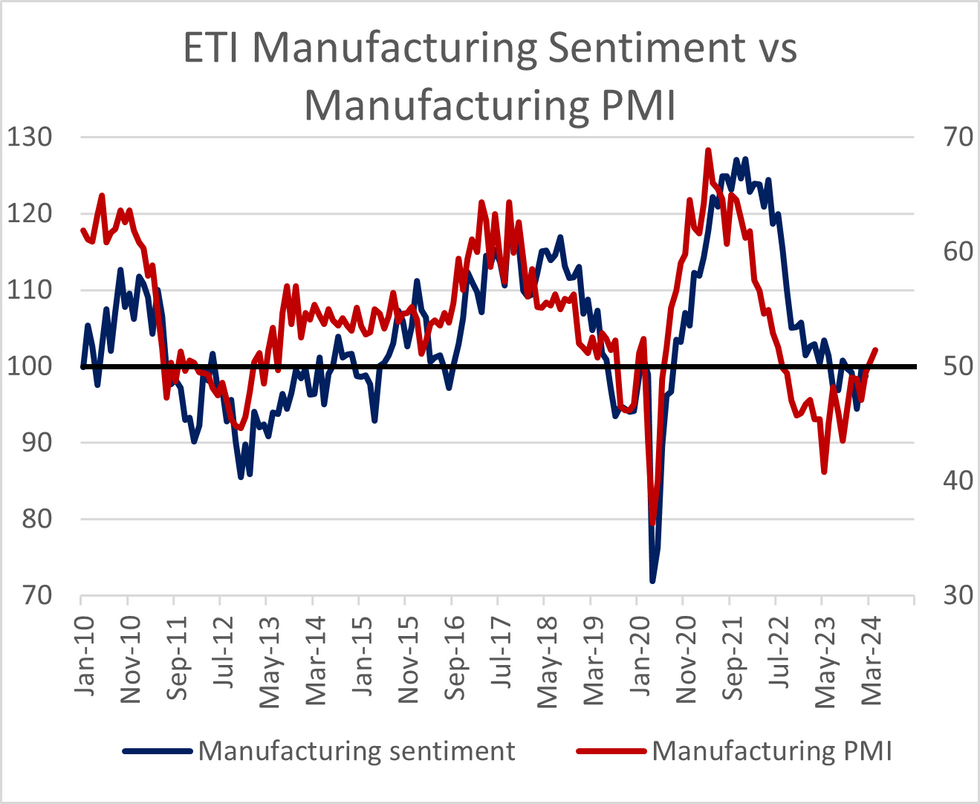

The Swedish manufacturing PMI rose for the third consecutive month in April, to 51.4 (vs an upwardly revised 50.4 prior). There was no consensus for the print.

- This is consistent with the increase in the manufacturing component of April’s Economic Tendency Indicator, which rose into expansionary territory at 100.5 (vs 98.6 prior).

- Looking at the sub-components, new orders rose to 54.6 (vs 51.5 prior) while employment rose to 49.1 (vs 46.8 prior). Production remained in expansionary territory at 52.2 (vs 54.9 prior).

- Raw material prices saw a notable rise to 53.4 (vs 46.8), though we note that expected manufacturing selling prices in the Economic Tendency Indicator remained at low levels in April.

- Overall, today’s print is consistent with analyst expectations for activity to recover through the remainder of this year, even after the Q1 flash GDP release was soft at -0.1% Q/Q.

- Elsewhere, we also note that company bankruptcy data released by UC this morning showed a 68% Y/Y rise in bankruptcies in April, a continuation of the trend flagged in the March Monetary Policy Report.

- Overall, this trend is another supportive factor for a Riksbank rate cut next week.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok