Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SWEDEN

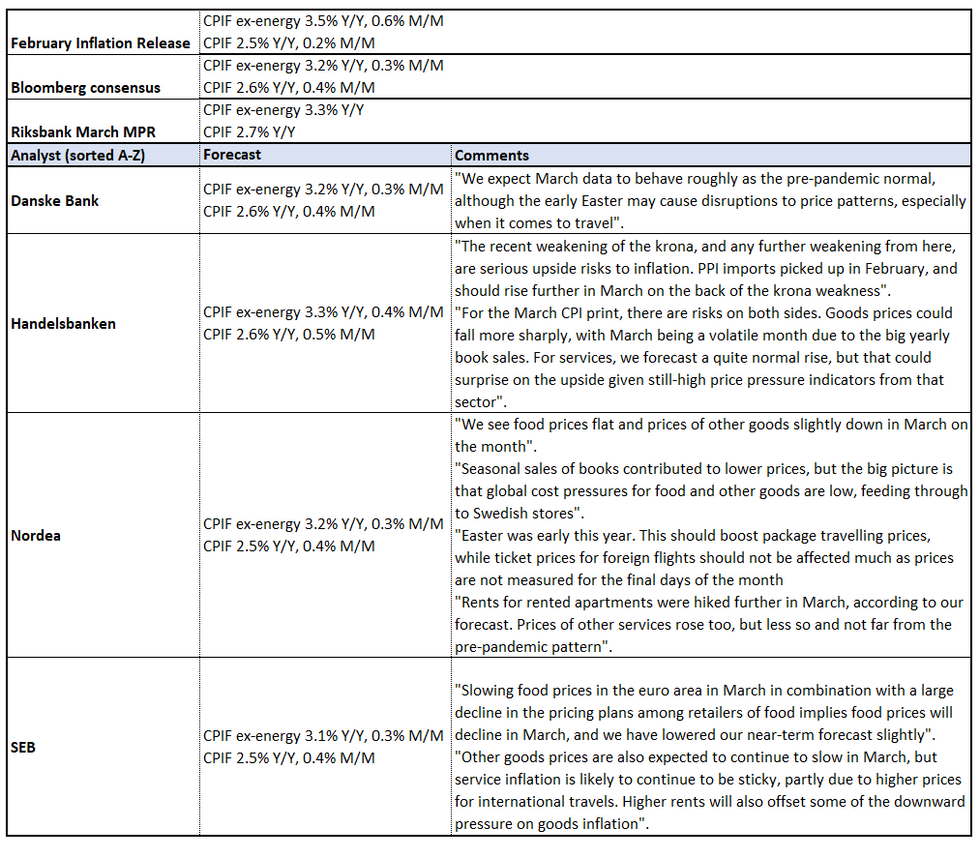

Swedish March CPI is due tomorrow, with analysts expecting CPIF ex-energy at 3.2% Y/Y (vs 3.5% prior) and CPIF at 2.6% Y/Y (vs 2.5% prior). The Riksbank’s March MPR forecasted CPIF ex-energy at 3.3% Y/Y and CPIF at 2.7% Y/Y.

- This is the only CPIF report before the Riksbank’s May 8 meeting, and thus will be pivotal in determining whether the Executive Board can confidently cut rates ahead of the ECB and the Fed.

- Markets currently price 14bps of rate cuts through the May meeting, according to estimates from SEB.

- If the data prints in line with the Riksbank’s forecast, it would tilt expectations further in favour of a May rate cut. However, the development of the SEK between now and the May meeting will still be a key input before cementing that case (we also note that Q1 GDP appears to be tracking above the current forecasts, an additional hawkish factor on the margin).

- A higher-than-expected reading (vs the Riksbank’s forecast) may tilt favour back towards a June cut though, especially when coupled with the hawkish impetus of yesterday’s US CPI data on the Fed policy outlook (and therefore the SEK).

- Analysts note that services prices may pose upside risks to tomorrow’s print, particularly from travel-sensitive components owing to the early Easter-weekend this year.

- See the image below for a selection of analyst views:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok