Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

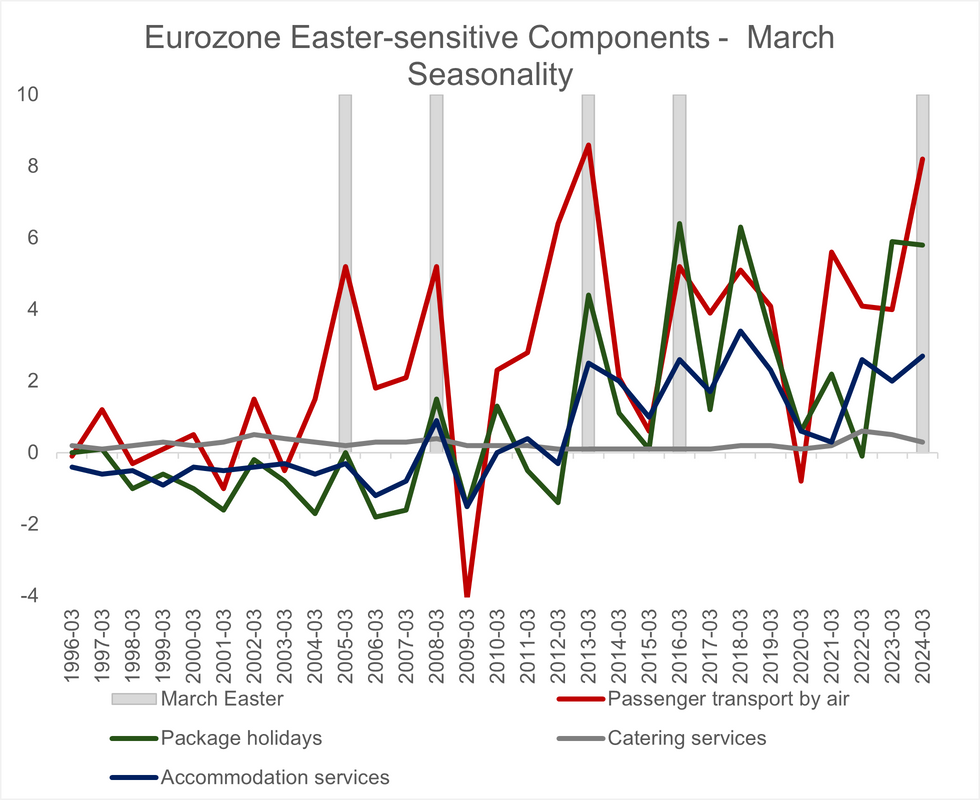

A closer look at the final Eurozone March HICP data suggests upward “Easter-effects” in key services categories were largely limited to airfares, denting expectations for a strong reversal in April.

- Many analysts expected sub-components sensitive to the early 2024 Easter weekend (e.g. airfares, package holidays, catering services and accommodation services) to push inflation higher in March, before having an opposite (i.e. downward) effect in April.

- Eurostat data shows that airfares rose 8.2% M/M NSA in March ’24, above the 4.0% M/M print in March 2023 and the 1996-2023 average of 2.4% M/M. This was the second highest March print since 1996, with March 2013’s 8.6% M/M also occurring in tandem with an early Easter weekend.

- Other relevant components saw less obvious “Easter effects”. Package holidays were 5.8% M/M (vs 5.9% in March 2023) while accommodation services were 2.7% M/M (vs 2.0% in March 2023).

- This suggests that while airfares may see a sizeable monthly NSA reversal in April 2024, smaller changes are likely in other components.

- Overall, the data indicate that March’s stickiness in services inflation (at 4.0% Y/Y for the fifth consecutive month) cannot fully be attributed to Easter-related calendar effects.

- Furthermore, airfares only contributed 0.04pp to the 2.4% Y/Y headline HICP rate, so even that component may exert only a small drag on services inflation in April, leaving the need for more broad-based disinflation to help the category finally break through the 4.0% handle for the first time in 6 months.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok