Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSY SUMMARY: This Indecision's Buggin' Me

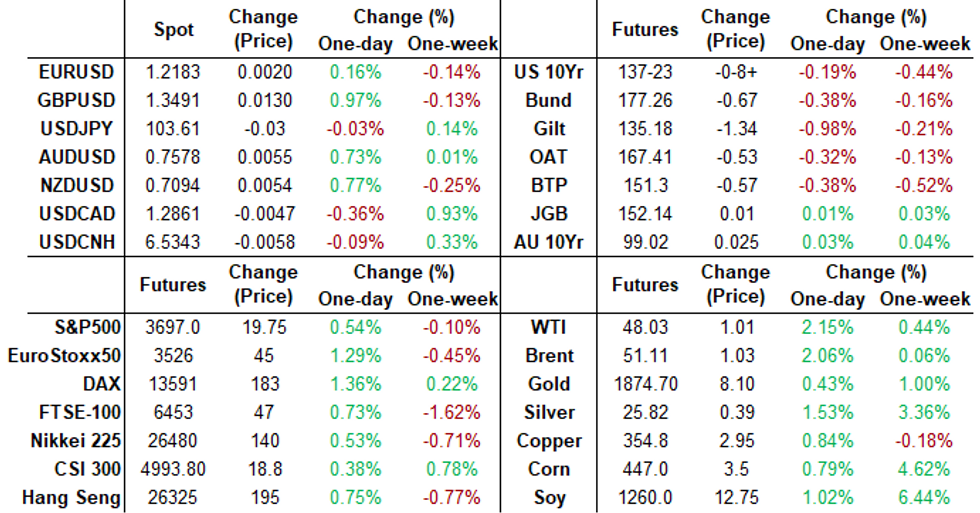

Tsys weaker across the curve by the bell, more than making up for Tue's rally with yield curves bear steepening back to mid-2017 levels before scaling back slightly in late trade.

- Risk-on: Seasonal bid for equities (ESH1 +17.0) despite Pres Trump not signing Covid relief bill in favor of $2k checks, spurred partially by late hour hopes of UK/EU Brexit deal (GBP surged to 1.3571 high on midmorning chatter deal was done only for Sterling to recede back to 1.3476 when wires walked back the rumor).

- After early post-data chop, Tsy futures extended pre-open lows, yld curves rebounding after flattening last couple sessions. Noted pick-up in sell volumes in 10s-30s, TYH appr 320k at moment; sources reported prop and fast$ selling 5s-10s.

- Jan serial Tsy options expire Thursday due to Friday Christmas holiday.

- The 2-Yr yield is up 0.6bps at 0.1189%, 5-Yr is up 1.3bps at 0.375%, 10-Yr is up 3.5bps at 0.9513%, and 30-Yr is up 4.6bps at 1.6938%.

US TSY: Short Term Rates

US DOLLAR LIBOR: Latest settles

- O/N +0.00050 at 0.08563% (+0.00125/wk)

- 1 Month +0.00475 to 0.14800% (+0.00425/wk)

- 3 Month +0.01287 to 0.25100% (+0.01525/wk)

- 6 Month +0.00100 to 0.26375% (+0.00525/wk)

- 1 Year +0.00138 to 0.33863% (+0.00463/wk)

- Daily Effective Fed Funds Rate: 0.09% volume: $66B

- Daily Overnight Bank Funding Rate: 0.08%, volume: $158B

- Secured Overnight Financing Rate (SOFR): 0.07%, $923B

- Broad General Collateral Rate (BGCR): 0.06%, $360B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $328B

- (rate, volume levels reflect prior session)

- Tsy 4.5Y-7Y, $6.001B accepted vs. $11.485B submitted

- Next scheduled announcement:

- Mon 12/28 Forward schedule release at 1500ET

EURODOLLAR/TREASURY OPTIONS: Summary

Eurodollar Options:

- +10,000 Blue Mar 92 puts, 3.5

- +10,000 short Mar 95 puts, 0.25

- +2,500 Mar/Jun 100 call strip, 0.75

- Overnight Trade

- 2,000 Jan/Feb 99.812 straddle strip

- 1,500 Jun 99.812/99.87 1x2 call spds

- over 35,000 TYF 137.5 puts, 1

- over 16,000 TYF 137.75 puts, 6

- Block 20,000 FVF 126 calls, 3/64 at 1155:33ET. Open interest 46,840 on the soon to expire Jan option

- Overnight Trade

- 13,000 TYG 137 puts, 12 incl 3,750 Block

- 2,000 TYG 135/136/137 put trees

- Modest volumes in Jan and Feb puts

- 4,200 TYF 137.5 puts, 1 last

- 8,600 TYF 137.75 puts, 2 last

- 8,900 TYF 138 puts, 7

- 7,700 TYG 136 puts, 3 last

*Reminder, January serial ops expire Thursday, earlier than usual due to Christmas holiday early close Thursday, full close Friday. Decent amount of options coming off the sheets for a serial expiry. Sell-off in underlying crossing several strikes.

| EXPIRY | CALLS | PUTS | TOTAL | NEAREST ATM STRIKE TOTALS |

| Jan 30Y | 251,399 | 202,159 | 453,558 | 172.00 w/ 22,654 (6,229c, 16,425P) |

| 172.50 w/ 27,857 (20,202c, 7,655P) | ||||

| 173.00 w/ 33,531 (16,521c, 17,010P) | ||||

| Jan 10Y | 549,349 | 636,383 | 1,185,729 | 137.75 w/ 36,599 (21,167c, 15,432p) |

| 138.00 w/ 83,528 (49,319c, 34,209p) | ||||

| 138.25 w/ 25,123 (20,967c, 4,156P) | ||||

| Jan 5Y | 343,732 | 164,318 | 508,050 | 125.75 w/ 29,314 (14,117c, 15,197p) |

| 126.00 w/ 58,651 (46,840c, 11,811p) | ||||

| 126.25 w/ 84,296 (83,676c, 620p) | ||||

| Jan 2Y | 2,923 | 10,037 | 12,960 | 110.38 w/ 9,504 (1,475c, 8,029p) |

| 110.50 w/ 1,436 (1,426c, 10p) |

EGBs-GILTS CASH CLOSE: UK Long End Blows Out As Brexit Deal Said Imminent

Long-end UK yields blew out Wednesday (5s30s rose the most since June) and German Bunds weakened alongside as the UK and EU appeared to be on the precipice of a Brexit deal as soon as today.

- Many headlines from multiple sources to that effect began in earnest around 1340GMT when the UK curve really began to sell off. MNI's Policy team reported "the EU and the UK seemed to be closing in on a post-Brexit trade agreement on Wednesday, though EU sources cautioned that a deal was still not in the bag."

- Elsewhere, Italy and Greece unveiled their 2021 funding plans; see our Bullets service for details.

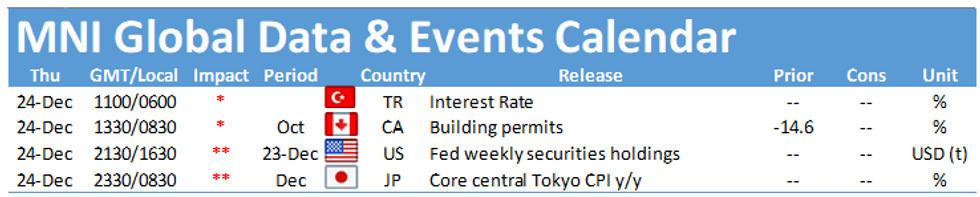

- With little on the calendar on a holiday-shortened Thursday, all attention will be on Brussels and London to see if a deal finally crosses the line.

Closing Levels / 10-Yr Periphery EGB Spreads:

- Germany: The 2-Yr yield is up 3.2bps at -0.704%, 5-Yr is up 4.3bps at -0.719%, 10-Yr is up 4.8bps at -0.547%, and 30-Yr is up 4.8bps at -0.15%.

- UK: The 2-Yr yield is up 1.2bps at -0.121%, 5-Yr is up 6.9bps at -0.037%, 10-Yr is up 10.3bps at 0.286%, and 30-Yr is up 13bps at 0.863%.

- Italian BTP spread down 1.8bps at 113.2bps / Spanish spread down 2.4bps at 62.1bps

EUROPE OPTIONS SUMMARY: Sterling Vol Sold As Brexit Deal Nears

Wednesday's options flow included:

- RXH1 176.00/178.00 combo sold at 59 in 1.4k

- LH1 100.00 call bought for 3.75 in 3.2k (v 99.985)

- LM1 99.875/100.125 ^^ sold at 4 in 5k

- LM1 100.00^ sold down to 10.75 in 3k

- 0LU1 100.00/99.875/99.625 broken put fly bought for 1.5 in 6k

- 2LH1 99.75/99.625 put spread bought for 1.5 in 5k

FOREX: GBP Shoots Higher as Brexit Deal Seen as Done

A veritable flurry of source reports from various outlets drove GBP higher, as news rolled in that a Brexit deal was as good as done, with negotiators going over the final details ahead of a convening of EU ambassadors on Thursday to go over the details.- As a result, GBP firmed sharply, prompting GBP/USD to add well over a cent and narrow the gap with (but not quite challenge) the Dec17 highs of $1.3624.

- The sole currency outstripping the GBP Wednesday was NOK, which firmed well alongside a near 3% oil price rally. USD/NOK remains well within reach of the 8.5520 cycle lows.

- Focus Thursday turns to the passage of any Brexit bill and the Turkish central bank rate decision. Outside of that, volumes are likely to be light, with news flow thin ahead of the Christmas break.

OPTIONS: Expiries for Dec24 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.2100(E536mln), $1.2200-20(E1.4bln)

- USD/JPY: Y100.20($1.3bln-USD puts), Y102.50($600mln), Y103.75-85($674mln)

- GBP/USD: $1.3150(Gbp640mln)

- USD/CNY: Cny6.5750($600mln)

EQUITIES: Stocks Firm as Brexit Deal Looks More Certain

Stocks across Europe and the US traded well Wednesday, with several reports circling that a Brexit deal is more than likely before Christmas, avoiding any further economic pressure that may stem from an abrupt end to the transition period on January 1st.- GBP strength countered any significant advance in UK equities, with the FTSE-100 adding around 0.7% and underperforming its continental peers.

- In the US, equities followed suit, with the S&P rising just over 0.5%. Gains were driven by energy and financials, with tech the sole sector in the red and largely responsible for the NASDAQ's softness into the close. The VIX retreated, falling back below the 23 point mark.

COMMODITIES: Oil Bounces Well on Sizeable Gasoline, Distillates Draw

Larger than expected draws in US gasoline and distillate reserves helped oil bounce well ahead of the Wednesday close, after a softer showing in the European morning. WTI and Brent crude futures both managed to gain near 3% apiece, with a resumption of USD weakness also a contributory factor.- WTI narrowed the gap with, but failed to top, the mid-December highs at $49.28.

- In metals markets, gold and silver traded well after an uninspiring start to the session. Spot gold built on gains made through the overnight highs of $1872.31, adding around 0.7%. Trading is likely to thin further headed into the final few trading sessions of 2020.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.