Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSY SUMMARY: Democracy Under Siege

Not how you would expect markets to finish: risk-appetite evaporating as DC protestors breach the Capitol, Congress that had been in process of counting electoral votes in recess, DC Mayor orders 1800ET curfew. Heavy volumes (TYH>2.4M) as yields surged (10YY tapped 1.0524%).

- Tsys opened weaker along with equities after GA special run-off election points toward Democrats gaining one if not two Senate seats.

- Shrugging Off Big ADP Employment Data Miss: Tsy futures headed back toward late overnight lows after bouncing in lead-up to Dec ADP data: Huge miss: -123k bs. +75k est (+307k in Nov). Very heavy volumes early as yield curves bear steepen to 4+ year highs.

- Tsys made new session lows as equities bounced lows (still inside overnight range w/ESH1 +4.0 at moment). Decent full day volumes just over hour after NY open: TYH1>1.3M. Sources reported real$ and bank portfolio selling across the curve, prop and fast$ two-way in short end, deal-tied selling getting lost in the mix, curve steepeners.

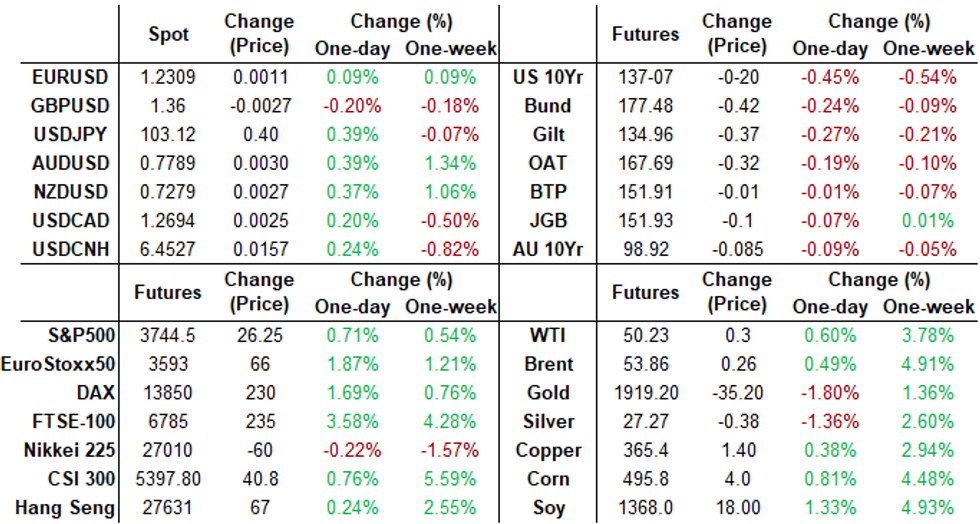

- The 2-Yr yield is up 2bps at 0.1408%, 5-Yr is up 5.1bps at 0.4274%, 10-Yr is up 8.1bps at 1.0355%, and 30-Yr is up 10.2bps at 1.8099%.

US TSY: Short Term Rates

US DOLLAR LIBOR: Latest settles:

- O/N +0.00012 at 0.08650% (+0.00887/wk)

- 1 Month +0.00112 to 0.13200 (-0.01188/wk)

- 3 Month -0.00288 to 0.23400% (-0.00438/wk)

- 6 Month -0.00150 to 0.25238% (-0.00525/wk)

- 1 Year +0.00263 to 0.33238% (-0.00950/wk)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 0.09% volume: $55B

- Daily Overnight Bank Funding Rate: 0.08%, volume: $140B

- Secured Overnight Financing Rate (SOFR): 0.11%, $986B

- Broad General Collateral Rate (BGCR): 0.08%, $358B

- Tri-Party General Collateral Rate (TGCR): 0.08%, $336B

- (rate, volume levels reflect prior session)

FED: NY Fed Operational Purchases

- TIPS 7.5Y-30Y, $1.201B accepted vs. $2.367B submission

- Next scheduled purchase:

- Thu 1/07 1100-1120ET: Tsy 20Y-30Y, appr $1.750B

- Fri 1/08 1100-1120ET: Tsy 0Y-2.25Y, appr $12.825B

EURODOLLAR/TREASURY OPTIONS: Summary

Eurodollar Options:- +5,000 Green Dec 98.87/99.125/99.37 put flys, 4.25 legs

- Block, 11,250 Green Sep 93 puts, 8.5 at 1012:05ET

- +10,000 Red Dec 92/95 put spds, 2.75

- +5,000 Green Sep 93 puts, 8.0

- +10,000 Apr 99.687/99.75/99.81 put flys, 0.5

- Block -20,000 short Sep 97 straddles 2.5 over Green Sep 95 puts

- Overnight

- +12,500 Mar 98/100.25 call spds, 0.5

- 5,000 Mar 98 calls, 0.5

- 7,500 Blue Apr 95/96 1x2 call spds

- 4,500 Blue Jan 93 puts, 2.5

- -9,000 TYG 135.75/136.25/136.75/137.5 put condors, 19-20

- 6,000 TYH 135.5/138.5 put over risk reversals, 1

- 2,000 TYG 137.25/137.75 put spds, 21

- -1,000 TYH 135/136/137 1x4x3 put flys earlier 49/64

- 4,000 TYH 135.5/138.5 put over risk reversals, 1

- 12,000 TYG 136.25/138 call over risk reversal, 0.0

- +4,000 TYH 135.5 puts, 2

- Block -13,861 wk3 TY 137.5 puts, 25/64 vs. 137-10/0.60% at 0947:17ET, still bid (open interest 24,126)

- 2,600 TYH 136/137/138 put flys, 1-0

- Overnight:

- Block, +20,000 TYG 139 calls, 2, another 13k on screen

- Block, +22,000 FVG 126.25 calls, 2.5

- 6,000 TYG 136.5 puts, 6-9

- 5,000 TYH 136.5 puts, 20-23

- 4,000 TYH 135/136/137 2x3x1 put flys, 2

- 2,000 TYH 134/135/136 put flys, 3

- 2,000 TYG 138 calls, 9

- -3,000 FVH 125.5 puts, 8.5

EGBs-GILTS CASH CLOSE: Bear Steepening Post-US Senate Elections

Bunds and Gilts bear steepened Wednesday, with periphery spreads tightening, largely on greater anticipation of US fiscal expansion following the Georgia Senate elections.

- Broadly disappointing Dec services PMI helped core FI recover some lost ground in the morning.

- We saw a rally in Gilts to session highs and buying throughout the Short Sterling strip, following our MNI BoE exclusive on Negative rates just before 1400GMT.

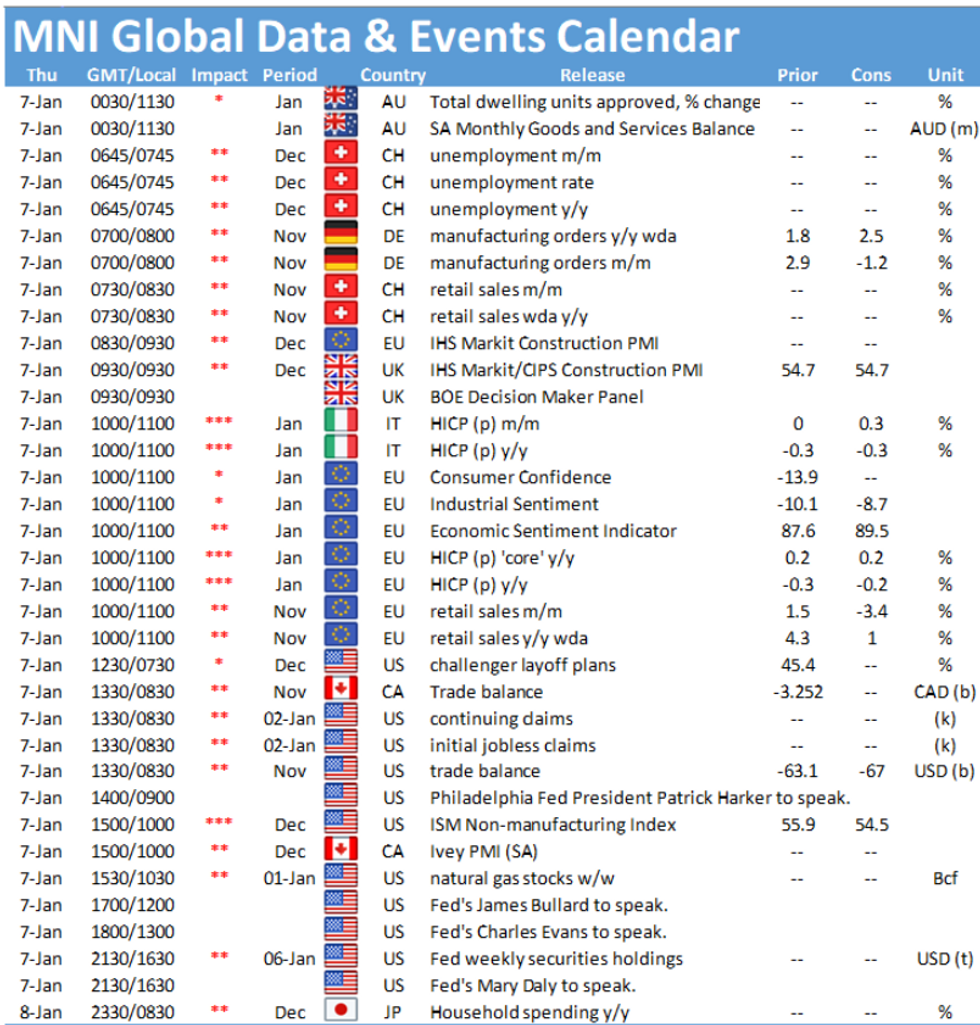

- Thursday sees French and Spanish bond auctions, German factory orders and Italy+Eurozone Dec flash inflation data. Closing Levels / 10-Yr Periphery EGB Spreads:

- Germany: The 2-Yr yield is up 1.4bps at -0.702%, 5-Yr is up 1.8bps at -0.729%, 10-Yr is up 5.7bps at -0.52%, and 30-Yr is up 2.9bps at -0.137%.

- UK: The 2-Yr yield is up 0.9bps at -0.134%, 5-Yr is up 1.4bps at -0.078%, 10-Yr is up 3.4bps at 0.243%, and 30-Yr is up 4.4bps at 0.823%.

- Italian BTP spread down 5.6bps at 108.7bps / Spanish down 4.6bps at 56.6bps

EUROPE OPTIONS: Summary

- Largely Short-Sterling Upside:

- DUG1 112.30/20/00p fly, sold at 3 in 2.5k

- RXG1 177.50/177.00ps vs 178.00/178.50cs, sold the ps at -13 in 5k

- RXG1 180 calls, bought for 4 in 10k.

- RXH1 177.50/176.00/174.50p fly 1x3x2, bought for 3 in 1.5k

- LH1 100.00/100.125/100.25 call fly bought for 1.75 in 8k

- LH1 100.00/100.125 1x2 call spread sold at 1 in 2.5k

- LM1 100p, sold at 4 in 2k

- LM1 100.00/12/25/37c condor, bought for 3.5 in 7k

- LM1 100.25c x2 vs LU1 10012/100.25cs, sold the June at 1 in 6kx3k

- LZ1 100p, sold at 4.75 in 4k

- ERM1 100.00p x1.5 vs 100.62c, bought the p for 0.5 in 17.5kx26.25k

- 3Rz1 100.25/100.00ps 1x2, bought for 1.5 in 5k

FOREX: USD Chop, Risk-On Prevails Despite Protests

With US TSY Futures under pressure, an initial rally in the USD was quickly reversed as Equities remained firm and risk-on theme dominated the markets.

- EURUSD had a wild ride today after testing 1.2350 during the first half of the session. A rebound in the USD saw us take out the lows of the day through 1.2275 to a low of 1.2266. Short term positioning likely caused a round of stops to be triggered before late USD selling took us back above 1.23. * Cross JPY remained bid throughout the day with the clearest barometer for risk, AUDJPY, up 0.92% on the day. EURJPY also benefitting +0.55% with USDJPY also heading into the close, up 0.5% at 103.23.

- GBPUSD was heavy amid the usd buying, combined with an MNI story regarding potential negative rates in the UK. Lows were made at 1.3540, however, the pair also rebounded healthily back above the 1.36 handle.

- In EM, USDMXN was a notable mover down 1.2% with a notable technical break of 19.70 and the Peso benefitting from the rally in risk.

- The Dollar Index finds itself exactly in the middle of its 60 tick range at 89.50.

- There was little to no movement in the FX space on the release of the FOMC minutes amid ongoing protests at the Capitol Building.

FX OPTIONS: Expiries for Jan 7 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.2155(E1.3bln-EUR puts), $1.2250(E727mln-EUR puts), $1.2340-50(E499mln), $1.2700(E924mln-EUR puts)

- USD/JPY: Y102.50-60($640mln), Y103.20-25($794mln), Y103.70($670mln), Y104.00($1.2bln)

- EUR/GBP: Gbp0.8800(E1.1bln-EUR puts), Gbp0.8850(E649mln), Gbp0.9300(E510mln)

- AUD/NZD: N$1.0690(A$640mln-AUD puts)

- USD/CNY: Cny6.4894($500mln-USD puts), Cny6.50($555mln), Cny6.5960($500mln)

- Larger Option Pipeline

- EUR/USD: Jan11 $1.2095-1.2110(E1.6bln), $1.2295-1.2300(E3.5bln-EUR puts), $1.2310-15(E1.4bln-EUR puts); Jan12 $1.2200(E1.3bln-EUR puts), $1.2300(E1.2bln)

- USD/JPY: Jan12 Y104.00($1.2bln-USD puts); Jan13 Y103.00($1.3bln)

- GBP/USD: Jan11 $1.3700-15(Gbp1.2bln-GBP puts); Jan12 $1.3995-1.4000(Gbp986mln-GBP puts)

- AUD/USD: Jan11 $0.7625(A$1.2bln-AUD puts), $0.7724-25(A$1.3bln-AUD puts)

PIPELINE: $12.9B High-Grade Debt To Price Wednesday

- Date $MM Issuer (Priced *, Launch #)

- 01/06 $4B *ADB 10Y +15

- 01/06 $3B #Toyota Motor Cr $1B 3Y +25, $750M 3Y FRN SOFR+33, $700M 5Y +40, $550M 10Y +62.5

- 01/06 $2.25B #BNP Paribas 6NC5 +90

- 01/06 $2B *Kommunalbanken 5Y +9

- 01/06 $1B *AerCap Ireland 5Y +155

- 01/06 $650M #Ares Capital +5Y +180

- On tap for Thursday

- 01/07 $Benchmark World Bank (IRBD) 2Y FRN SOFR+14, 2027 Tap SOFR+35a

EQUITIES: US Equity Indexes Paring Gains Amid DC Protests

- Dow Jones mini up 414 pts or +1.37% at 30709, S&P 500 mini up 30 pts or +0.81% at 3749.25, NASDAQ mini down 115.75 pts or -0.9% at 12679.

- Japan's NIKKEI down 102.69 pts or -0.38% at 27055.94 and the TOPIX up 4.96 pts or +0.28% at 1796.18

- China's SHANGHAI closed up 22.2 pts or +0.63% at 3550.877 and the HANG SENG ended 42.44 pts higher or +0.15% at 27692.3

- The German Dax up 240.75 pts or +1.76% at 13891.97, FTSE 100 up 229.61 pts or +3.47% at 6841.86, CAC 40 up 66 pts or +1.19% at 5630.6 and Euro Stoxx 50 up 63.23 pts or +1.78% at 3611.08.

COMMODITIES: Metals Recede, Energy Bid

Precious metals paring early week gains, energy markets show modest gains in late trade as electoral vote count disrupted by protesters breaching Capitol security.

- WTI Crude up $0.39 or +0.78% at $50.35

- Natural Gas up $0.02 or +0.85% at $2.725

- Gold spot down $31.42 or -1.61% at $1918.73

- Copper up $1.5 or +0.41% at $365.6

- Silver down $0.38 or -1.39% at $27.1783

- Platinum down $5.53 or -0.5% at $1107.9

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.