Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSY SUMMARY: Low Variance

Rates traded steady/mixed after the bell, Tsys near the middle of a narrow range on light volumes (TYH1<955k). Trading desks chalked up the muted trade to positioning ahead Wednesday's FOMC policy annc -- steady rate and asset purchases expected, talk of tapering last few week's deemed premature.

- MNI Fed Preview: Chair Powell and other key Fed members have batted away speculation of such an early taper, and absent extraordinary upside surprises in the labor market and inflation, the Fed will almost certainly remain cautious on tapering for the next few FOMC meetings at least.

- Janet Yellen Sworn In As 78th Secretary US Treasury Dept; Anthony Blinken confirmed as Sec of State.

- Tsy-way flow, modest option and deal-tied hedging kept prices close to home. Possibly contributing to light participation, "Verizon says technicians are aware of a a fiber cut in Brooklyn; Internet Outage Hits Broad Swath of Eastern U.S. Customers" Bbg

- Treasury Auction: small stop through on record $61B 5Y note auction, US Tsy $61B 5Y Note auction (91282CBH3) draws high yld of 0.424% (0.394% last month) vs. 0.425% WI; 2.34 bid/cover vs. 2.39 prior.

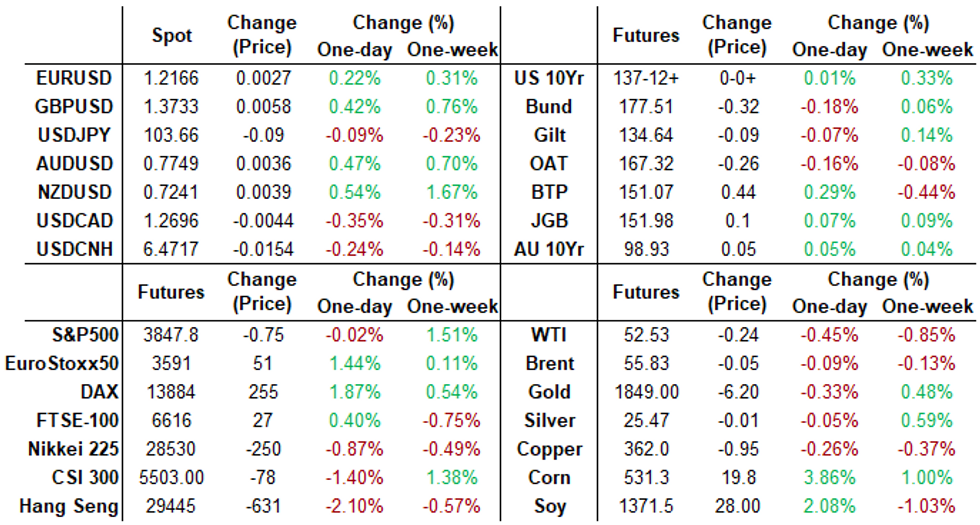

- The 2-Yr yield is up 0.8bps at 0.123%, 5-Yr is up 0.8bps at 0.4103%, 10-Yr is up 0.9bps at 1.0381%, and 30-Yr is up 0.8bps at 1.8004%.

MONTH-END EXTENSIONS: Prelim Barclays/Bbg Extension Estimates

Forecast summary compared to the avg increase for prior year and the same time in 2020. TIPS -0.16Y; Govt inflation-linked, 0.23.

| Estimate | 1Y Avg Incr | Last Year | |

| US Tsys | 0.08 | 0.09 | 0.07 |

| Agencies | 0.12 | 0.06 | -0.03 |

| Credit | 0.07 | 0.09 | 0.09 |

| Govt/Credit | 0.08 | 0.09 | 0.07 |

| MBS | 0.06 | 0.06 | 0.07 |

| Aggregate | 0.08 | 0.08 | 0.08 |

| Long Gov/Cr | 0.08 | 0.09 | 0.05 |

| Iterm Credit | 0.08 | 0.08 | 0.09 |

| Interm Gov | 0.09 | 0.08 | 0.07 |

| Interm Gov/Cr | 0.08 | 0.08 | 0.08 |

| High Yield | 0.07 | 0.08 | 0.09 |

US TSY: Short Term Rates

US DOLLAR LIBOR: Latest settles:

- O/N -0.00088 at 0.08375% (-0.00250/wk)

- 1 Month -0.00500 to 0.12250% (-0.00225/wk)

- 3 Month +0.00562 to 0.21850% (+0.00325/wk)

- 6 Month +0.00150 to 0.23450% (-0.00150/wk)

- 1 Year -0.00075 to 0.31150% (-0.00075/wk)

- Daily Effective Fed Funds Rate: 0.08% volume: $74B

- Daily Overnight Bank Funding Rate: 0.08%, volume: $217B

- Secured Overnight Financing Rate (SOFR): 0.06%, $885B

- Broad General Collateral Rate (BGCR): 0.05%, $354B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $319B

- (rate, volume levels reflect prior session)

- Tsy 20Y-30Y, $1.734B accepted vs. $5.131B submission

- Next scheduled purchases:

- Thu 1/28 1010-1030ET: Tsy 20Y-30Y, appr $1.750B

- Fri 1/29 1010-1030ET: TIPS 7.5Y-30Y, appr $1.225B

- Fri 01/29 Next forward schedule release at 1500ET

EURODOLLAR/TREASURY OPTIONS: Summary

Eurodollar Options:- -20,000 Sep 99.75/99.81 put spds, 1.5

- +2,500 short Dec 95/96/97 put flys, 2.75

- +1,500 Dec 100 calls 1.0

- +25,000 Blue Mar 90/91 put spds, 1.0

- +2,500 Blue Sep 83/87 put spds, 3.75

- +5,000 Blue Jun 88/91 3x2 put spds vs. 10k 95 calls, 1.0 net

- 1,000 Blue Feb 92/93 2x1 put spds

- Overnight trade

- +4,000 Blue Apr 90/91 put spds, 2.5

- +10,000 Blue Mar 92 puts, 4.0

- +10,000 Blue Mar 92/93 put spds

- +12,000 Blue Jun 90/91/92/95 broken call condors, 0.0

- 3,000 TYH 137.75/138.25 call spds 4 under TYH 136.75 puts

- 3,000 TYJ 135/136/137 2x3x1 put flys, 3

- 1,200 FVJ 125.5/135.75/137 1x1x2 call trees, 4

- 5,000 TYH 135/136 2x1 put spds, 2

- 3,000 USH 164/165 put spds

- Overnight trade

- >28,000 TYH 136 puts, 6-7

- +7,000 TYJ 133.5 puts, 8

- 6,200 USH 168 puts, 42 last

- Block, total 20,000 TYH 138 calls, 15-13 (total volume >45k)

- Block, +10,000 TYJ 133.5/138 put over risk reversal, 0.0

- Block, +5,000TYH 136.5/138.25 put over risk reversals, 4

EGBs-GILTS CASH CLOSE: Supply A Key Theme, To Be SURE

Gilts and Bunds traded weaker but in fairly erratic fashion throughout Tuesday's session, with periphery EGB spreads tighter.

- Italian spreads compressed, with optimism that stability will return following PM Conte's decision to resign this morning in order to form a new government.

- Bund yields came off the highs late in the session with the EUR weakening on a BBG report: "ECB Studying If Differences With Fed Policy Are Boosting Euro".

- Issuance was a key theme today with E14bn of E.U. SURE syndication (on books >E132bn!), and the UK, Netherlands and Italy holding auctions. We also had Greece, Austria, and Slovenia announce mandates. Closing yields/10-Yr Spreads to Bunds:

- Germany: The 2-Yr yield is up 0.4bps at -0.723%, 5-Yr is up 1bps at -0.734%, 10-Yr is up 1.7bps at -0.533%, and 30-Yr is up 2bps at -0.116%.

- UK: The 2-Yr yield is down 0.5bps at -0.138%, 5-Yr is down 0.1bps at -0.063%, 10-Yr is up 0.3bps at 0.265%, and 30-Yr is up 0.4bps at 0.838%.

- Italian BTP spread down 4.8bps at 118bps / Spanish down 1.7bps at 60.6bps

OPTIONS EUROPE SUMMARY: Schatz Condor Takes Tuesday's Size Prize

Tuesday's options flow included:

- RXH1 177/175.50/172p fly, sold at 18 in 1k

- RXH1 177.00/176.50/176.00/175.50p condor, bought for 8 in 1.25k

- OEH1 134.5/134ps, bought for 1.5 in 2k

- DUH1 112.30/112.40cs vs 112.20/112.10ps, sold the cs at 2 in 5k

- DUH1 112.30/40/50/60c condor vs 112.20/112.10ps, sold at 2 in 20k

- LK1 100.00/100.125 1x2 call spread (vs 100.20) vs LH1 100.00 call (vs 99.99), bought for 0 in 8.5k

- LM1 100.25c, bought for 1 in 2.5k (ref 100.035)

FOREX: EUR Knocked as ECB Study Exchange Rates

After staging a decent late-session recovery, EUR/USD was knocked lower just after the London close as Bloomberg sources reported that the ECB were studying the recent resilience of the EUR/USD exchange rate. The study is to focus particularly on the Fed and ECB's stimulus packages delivered throughout 2020, which was sufficient to knock around 20 pips off the rate.- Elsewhere, GBP traded well alongside the slightly steeper UK yield curve, prompting a show above 1.3740 in GBP/USD. The strength stopped just short of the Jan21 high at 1.3746, the highest since 2018.

- NZD, AUD and CAD all traded well as equities traded to new all time highs. The S&P500 touched 3870.90, with real estate and communication services outperforming.

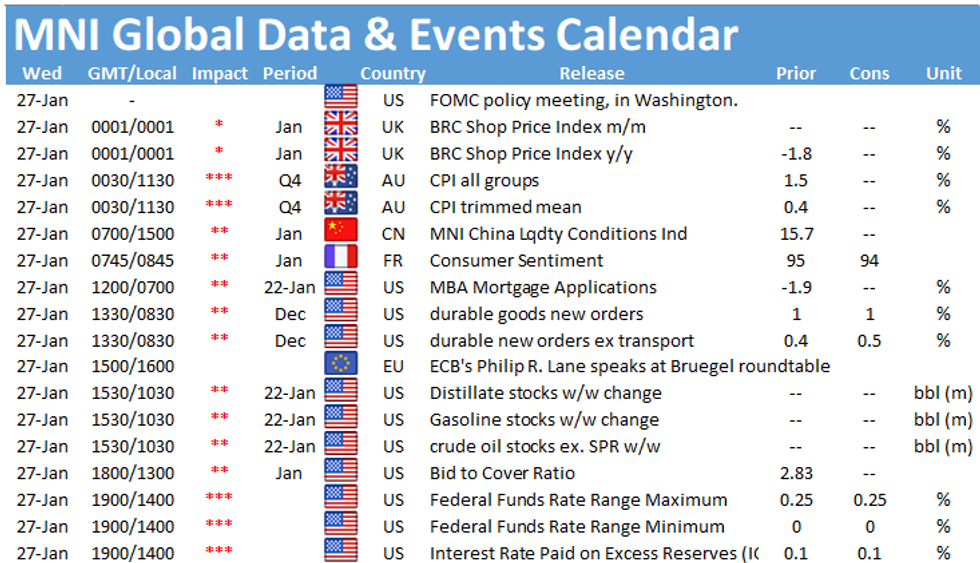

- Australian CPI & NAB business confidence numbers and prelim US durable goods orders are the calendar highlights Wednesday. The FOMC rate decision is due later in the day.

FX OPTIONS: Expiries for Jan 27 NY Cut 1000ET (Source DTCC)

- EUR/USD: $1.2000(E594mln), $1.2100(E714mln), $1.2150(E612mln), $1.2190-00(E1.4bln), $1.2250(E1.45bln), $1.2285-00(E715mln)

- USD/JPY: Y102.00-13($514mln), Y103.25-45($585mln), Y103.95-10($819mln), Y104.50-65($922mln)

- AUD/USD: $0.7500(A$1.2bln), $0.7750-65(A$551mln)

- AUD/NZD: N$1.0665(A$530mln)

- USD/CAD: C$1.2600($940mln), C$1.2750-65($845mln)

- USD/CNY: Cny6.42($1.0bln), Cny6.4960($880mln)

PIPELINE: Saudi Arabia, Credit Suisse Launched

- Date $MM Issuer (Priced *, Launch #)

- 01/26 $5B #Saudi Arabia $2.75B 12Y +130, $2.25B 40Y 3.45%

- 01/26 $4B #Credit Suisse 3Y +32, $1B 3Y FRN SOFR+39, $2B 6NC5 +90

- 01/26 $2.5B #Hong Kong Gov $1B 5Y +22.5, $1B 10Y +37.5, $500M 30Y +62.5

- 01/26 $1.5B *Oesterreichische Kontrollbank (OKB) 5Y +5

- 01/26 $1.25B #SVB Fncl $500M 10Y +80, $750M perpNC10 4.1%

- 01/26 $800M #New York Life 2Y FRN SOFR+22

- 01/26 $750M *Armenia 10Y 3.60%

- 01/26 $Benchmark 7-Eleven investor call, est $11B multi-tranche jumbo

EQUITIES: Stocks Hit an All Time High Before Consolidating

After a positive open on Wall Street, the S&P500 hit new all time highs, showing above 3870, with real estate and communication services names outperforming. This quickly gave way to consolidation, with markets deciding to trade sideways ahead of the FOMC on Wednesday.- Earnings season continues, with Tuesday's reports including Johnson & Johnson and American Express. Johnson & Johnson traded higher by as much as 3%, whereas the American Express report missed forecast, slipping by 3% to trade among the index's poorest performers.

COMMODITIES: Oil Comes Off Weekly Highs

Both WTI and Brent crude futures traded with early gains to make a decent attempt on last week's best levels, but this soon faded as equities consolidated on the Wall Street open. The weekly DoE crude oil inventories numbers take focus going forward, with markets seeing a build of around 500k barrels for the headline inventories number.- Precious metals were more mixed. Gold finished flat having traded in a particularly tight range while silver posted gains of 0.5% or so as recent pullbacks find support at the 50-dma. Last week's highs at $26.05 are the primary upside target.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok