Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSY SUMMARY: It's Not Headline Driven This Time

Game plan for Wednesday: Unless ADP comes out well off mean est (currently +860k): Set your clock for 0800ET for tomorrow's Tsy gap bid that runs to 1030ET, followed by a 50% retraces over next hour. This is how Bonds have reacted last two days. This wk's moves are not headline (China incursion into Taiwan airspace) driven or immediate risk-off in nature.

- Bond futures gap-bid at appr 0800ET the last two sessions, weaker stocks adding impetus to new duration highs in Tsys (ESM1 -47.0 at 4139.0 late), yield curves bull flattening, while the CBOE vol index VIX climbing +3.55 to21.85 high.

- Support Impetus speculation: not risk-off but accts unwinding net shorts as mean est' for Fri's NFP nears 1M, some desks say prop, fast$ and dealers that have been scaling back net short positions in Tsy and MBS inventories since February have accelerated. Blocks and stops exacerbating the current moves with cross asset hedging weighing on equities.

- 10Y futures Block buy (8.4k at 132-14, through a -13.5 offer) a more visible factor for support as 30YY slips to 2.2334% low, 10YY 1.5552%. Eurodollar and Tsy option trades consistently favored buying low delta puts outright or funded via upside calls.

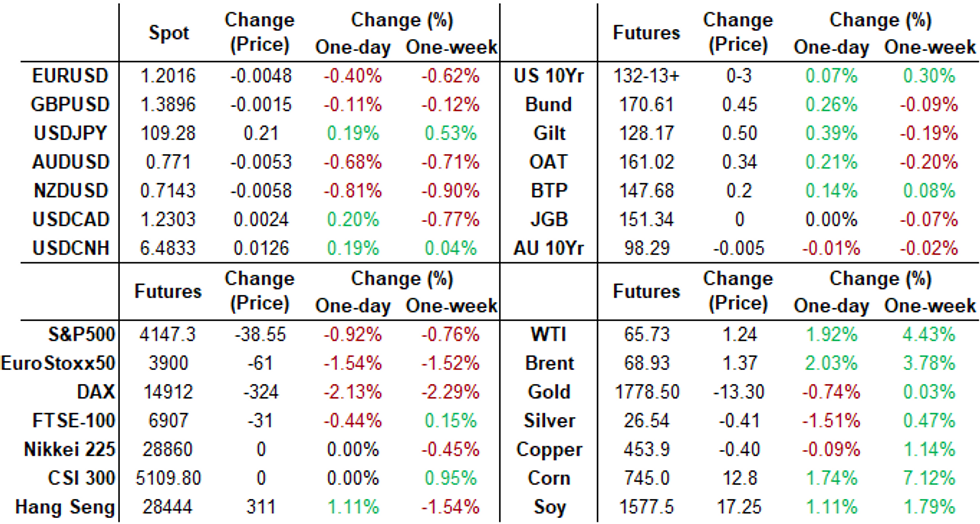

- The 2-Yr yield is up 0.2bps at 0.1605%, 5-Yr is down 0.3bps at 0.8205%, 10-Yr is down 0.5bps at 1.5924%, and 30-Yr is down 1.7bps at 2.2668%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest Settles

- O/N -0.00675 at 0.06450% (-0.00212 total last wk)

- 1 Month +0.00113 to 0.10838% (-0.00375total last wk)

- 3 Month -0.00100 to 0.17538% (-0.00500 total last wk) ** (Record Low 0.17288% on 4/22/21)

- 6 Month +0.00175 to 0.20663% (+0.00075 total last wk)

- 1 Year +0.00175 to 0.28288% (+0.00025 total last wk)

- Daily Effective Fed Funds Rate: 0.06% volume: $74B

- Daily Overnight Bank Funding Rate: 0.05% from Mon's 0.03% all-time low, volume: $248B

- Secured Overnight Financing Rate (SOFR): 0.01%, $930B

- Broad General Collateral Rate (BGCR): 0.01%, $376B

- Tri-Party General Collateral Rate (TGCR): 0.01%, $349B

- (rate, volume levels reflect prior session)

- Tsy 20Y-30Y, $1.734B accepted vs. $5.551B submission

- Next scheduled purchases:

- Wed 5/05 1100-1120ET: Tsy 4.5Y-7Y, appr $6.025B

- Thu 5/06 1010-1030ET: TIPS 7.5Y-30Y, appr $1.225B

US TSYS/OVERNIGHT REPO

Cooling ever so slightly: 2s-7s, 10s and 30s continue to lead specials. Other current levels: T-Bills: 1M 0.0025%, 3M 0.0051%, 6M 0.0279%; Tsy General O/N Coll. 0.01%

| Duration | Current | Old Issue |

| 2Y | 0.01% | -0.01% |

| 3Y | 0.00% | -0.08% |

| 5Y | 0.00% | -0.08% |

| 7Y | 0.01% | 0.00% |

| 10Y | -0.18% | -0.10% |

| 30Y | -0.15% | -0.07% |

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- +3,500 Red Dec 92/95 put spds 1.5 over short Oct 92/95 put spds

- +5,000 Red Mar 88/93 put spds 0.5 over Red Sep 95 puts, +7.5k Mon

- +10,000 Blue Dec 75/88 put over risk reversals, 1.0

- -20,000 short Aug 99.687 straddles 6.0 over 99.62 puts

- Block, 13,500 Green Jun 99.37/99.437 1x2 call spds, 1.5 net

- +5,000 Blue Sep 80/82/85 put flys, 3.5

- +10,000 short Sep 95/96 2x1 put spds, 0.25cr

- +1,500 short Dec 92/95/97 put flys, 7.0

- +2,000 short Dec 95/96 1x2 call spds, 1.0 after

- -15,000 short Sep 95/96 2x1 put spds, 0.25

- +2,000 Green May 90 calls, cab

- Overnight trade

- 4,000 Blue Sep 81/83 put spds vs. 86/88 call spds

- 5,700 Blue Dec 77 puts, part tied to 77/81 2x1 put spds

- 1,400 Blue Dec 70 puts, 2.5

- 1,000 Blue Jun 83/85 put spds vs. 86/87 call spds

- 1,400 Green Sep 90/91 put spds vs. 92/93 call spds

- 5,000 USM 159.5 calls, 43

- 16,000 TYM 132.5 calls, 33

- 6,000 TYM 131/132.5 put spds, 29

- -5,000 TYN 130/131.5 and 129.5/131 put spd strips, 16 total

- 2,700 TYN 131.5 straddles, 154-153

- Block, 7,500 TYM/TYN 133.5 call calendar spd, 6 vs. 131-28.5/0.05%

- -2,100 TYN 131.5 straddles, 154

- Overnight trade

- 5,000 wk1 TY 131/131.5 put spds

- 9,800 TYM 132 puts

- 4,000 TYM 133 puts

- 3,000 FVN 124.5 calls, 5

EGBs-GILTS CASH CLOSE: Reversal Of Fortune

Bunds and Gilts traded with a weak tone in the morning, until a sudden rout in US equities after midday London time triggered a significant risk-off move benefiting safe havens.

- No particular trigger to the risk-off move, though it was led by tech stocks, and could be some squaring ahead of Friday's US payrolls figured. Curves flattened as long-end yields fell sharply, with periphery spreads widening a couple of bps vs Bunds.

- That said, EGBs/Gilts ignored comments by US Treas Sec Yellen on the potential need for rising rates to stop the economy overheating on gov't spending (Tsys sold off sharply).

- Greece underperformed 5-Yr EUR benchmark syndication was announced.

- Weds sees Germany sell Bobl, UK sells 2031/ 2046 Gilts, final EZ/UK and IT/ES Apr PMI data.

Closing yields/10-Yr Spreads to Bunds:

- Germany: The 2-Yr yield is down 1.1bps at -0.697%, 5-Yr is down 2.4bps at -0.607%, 10-Yr is down 3.4bps at -0.238%, and 30-Yr is down 4.4bps at 0.315%.

- UK: The 2-Yr yield is down 3.3bps at 0.047%, 5-Yr is down 4bps at 0.349%, 10-Yr is down 4.7bps at 0.795%, and 30-Yr is down 5.2bps at 1.29%.

- Italian BTP spread up 2.1bps at 109.9bps / Greek spread up 4.5bps at 124.2bps

OPTIONS/EUROPE SUMMARY: Focus On Greens

Tuesday's options flow included:

- DUN1 112.10/112.00ps, bought for 2.5 in 1.25k

- 0RH2 100.37/100.50cs 1x3, bought for flat in 7.5k

- 2RM1 100.25/100ps, bought for 1 in 2.5k

- 2RH2 100.125/100.00/99.75 1x1.5x0.5 broken put fly bought for 1 in 7k

- 3RU1 99.87p, sold down to 4 in circa 4k

- LZ1 99.875^ sold down to 8 in 4k

- 2LZ1 99.62/99.75cs 1x2, sold the 1 at flat in 2.5k

- 3LM1 99.20/99.00/98.75p fly sold at 6 in 5k

FOREX: USD Moves From Strength to Strength

- In a relatively eventful session, the greenback surged, bouncing well off the Monday lows, as renewed equity weakness helped boost haven currencies and undermine growth-proxy and commodity-tied FX. Notable weakness in the global chipmakers helped shake sentiment, with the S&P 500 knocked to new multi-week lows to open a near 70 point gap with the all time highs posted in late April.

- The strong dollar sentiment was also reinforced by commentary from US Treasury Secretary (and former Fed chair) Yellen, who stated that rates may need to move higher to temper an economy that may 'overheat'.

- The bouncing greenback prompted the USD Index to narrow the gap with next key resistance at the 91.718 50-dma. A clean break and close above here opens initially 91.980 ahead of 92.286.

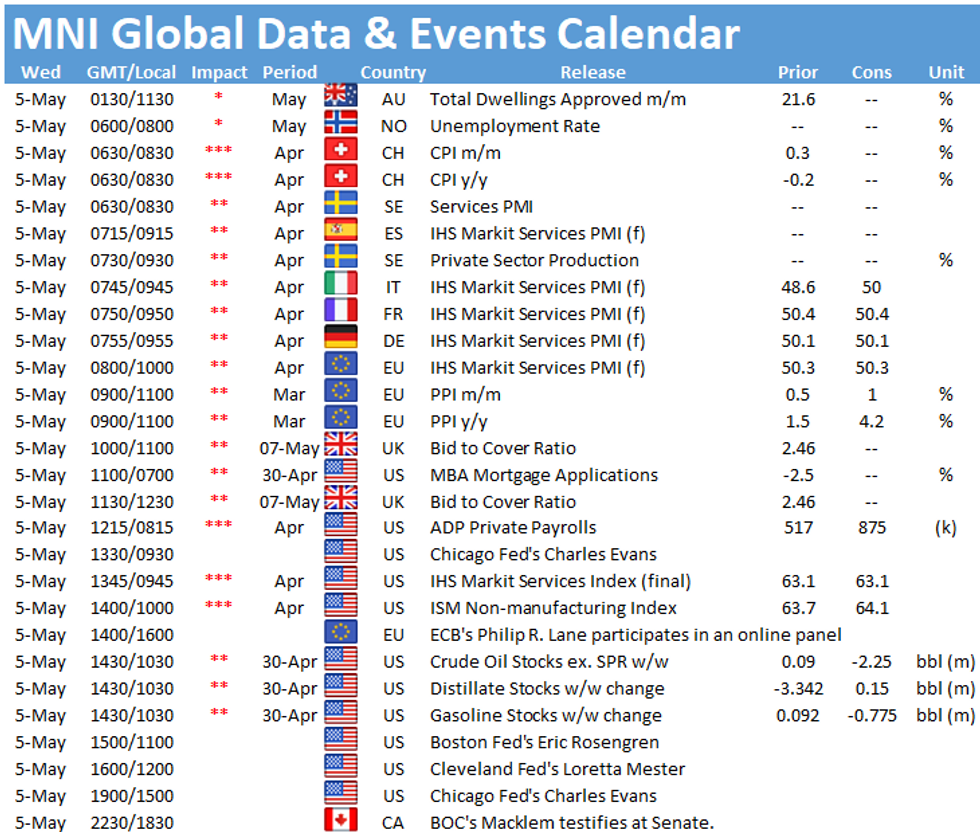

- Focus Wednesday turns to final April PMI data from across the Eurozone and US, European PPI number s for March and the April US ISM Services data. The ADP employment change report will also be watched for any read through to Friday's NFP release. Central bank speakers include Fed's Evans, Rosengren and Mester as well as ECB's Lane.

FX OPTIONS: Expiries for May05 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.2025-30(E561mln), $1.2040-55(E1.4bln), $1.2120(E650mln)

- AUD/USD: $0.7750(A$959mln)

- USD/CAD: C$1.2300($1.1bln)

PIPELINE: $2B NXP Semiconductors 2Pt Launched

- Date $MM Issuer (Priced *, Launch #)

- 05/04 $2B #NXP Semiconductors $1B 10Y +95, $1B 20Y +115

- 05/04 $Benchmark Rep of Chile tap 10Y +100a, 20Y +145a

EQUITIES: Chip Shortage Undermines Tech, Dragging Global Indices

- Stocks were sold globally Tuesday, with the S&P 500 opening a near 70 point gap with the alltime as weakness in the global semiconductors sector dragged sentiment.

- Sour sentiment started well ahead of the NY open with a sizeable surge in volumes denting the e-mini S&P, which fell through the 20-day EMA at 4132.59. Tech firms bore the brunt, pressuring the NASDAQ future to erase the early April rally.

- The semiconductors sub-sector was largely responsible, as the worldwide chip shortage curtails production plans. Germany's Infineon said they see 2.5mln 'lost cars' due to bottlenecks in specific chip products. This prompted the likes of NVIDIA, Qualcomm and Intel to trade sharply lower, falling as much as 4%.

- The e-mini S&P showed below the 20-day EMA of 4132.59, opening further losses toward key support at the Apr20 low of 4110.50.

COMMODITIES: Oil Benchmarks Resume Rally, Gold Rejects $1,800 Level

- Markets are maintaining a degree of optimism surrounding the expected resumption of economic activity in the U.S. and around Europe. These hopes are by far outweighing the lingering anxieties posed to the demand outlook in places such as India and Brazil.

- WTI and Brent Crude futures gained around 1.5% on Tuesday. The breach of last week's resistance in WTI at $64.38 strengthens a short-term bullish case and negates any prior bearish signals. Attention is now on $66.15, March 15 high ahead of the key hurdle for bulls at $67.29.

- Notably, gasoline gains outpaced crude. There are already signs in several countries that drivers are getting back in their cars with retail gasoline prices in the U.S. at the highest since October 2018.

- Spot gold rose to the best levels since February 25th at $1,799.12 before a quick spike in the US dollar sapped any momentum and capped gains for the yellow metal. Additionally, the $1,800 an ounce level provided some psychological resistance that may have fueled short term profit taking. As of writing spot prices trade 0.85% lower on the session at $1,777.75.

- Palladium futures touched their highest levels on record Tuesday, above $3,000 an ounce, as positive U.S. vehicles sales data along with recovery hopes bode well for the metal used in catalytic converters, which reduce emissions from gasoline-powered engines.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.