Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MNI ASIA MARKETS ANALYSIS - Inflation Concerns

HIGHLIGHTS

- Stocks have been unsettled by intensifying concern about inflation

- US and EZ forward inflation swaps continue to push higher

- Currencies, in comparison, have been relatively calm.

US TSYS SUMMARY: Inflation Concerns Underpin Bear Steepening

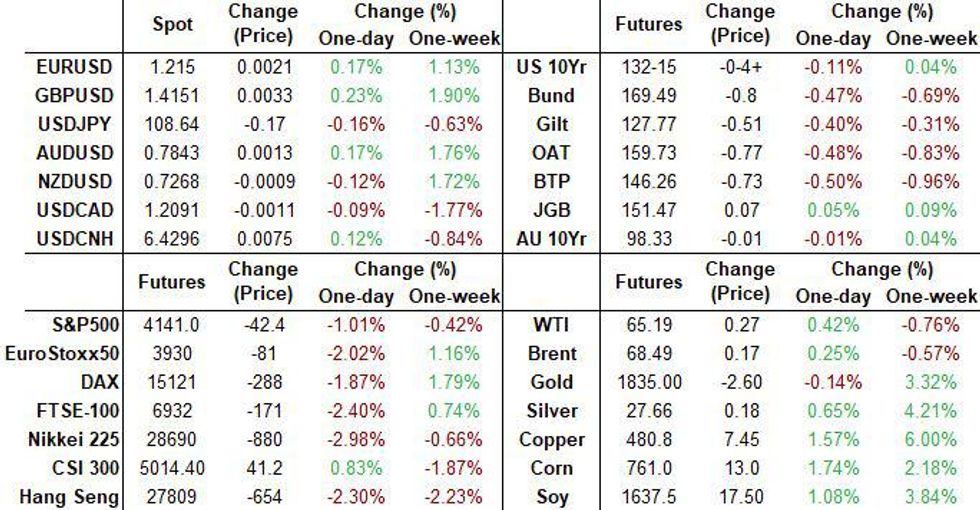

USTs have been under pressure on the back of intensifying concerns about inflation which have unsettled equity markets and caused sovereign bond curves to bear steepen.

- UST cash yields are 1-3bp higher with the curve 1-2bp steeper. Last yields: 2-year 0.1568%, 5-year 0.7950%, 10-year 1.6182%, 30-year 2.3474%.

- TYM1 trades at 32-15+, towards the bottom end of the day's range (L: 132-12+ / H: 132-23+)

- There have been a slew of Fed speakers hitting the wires this afternoon. The San Francisco Fed's Daly stated that the modal outlook is positive, while the Atlanta Fed's Raphael Bostic stressed that the recovery still has a long way to go and that policy should remain accommodative.

- The latter was reiterated by James Bullard who stated that it was too early to discuss tapering.

USD LIBOR FIX - 11-05-2021

O/N 0.06063 (-0.00275)

1W 0.07125 (-0.00025)

1M 0.09375 (-0.00438)

2M 0.12713 (-0.00537)

3M 0.16025 (-0.00725)

6M 0.19100 (-0.0015)

12M 0.26513 (-0.00187)

Fed Funds, OBFR Steady

| New York Fed EFFR for prior session (rate, chg from prev day): |

| * Daily Effective Fed Funds Rate: 0.06%, no change, volume: $66B |

| * Daily Overnight Bank Funding Rate: 0.05%, no change, volume: $271B |

SOFR Unchanged

| REPO REFERENCE RATES (rate, change from prev. day, volume): |

| * Secured Overnight Financing Rate (SOFR): 0.01%, no change, $869B |

| * Broad General Collateral Rate (BGCR): 0.01%, no change, $374B |

| * Tri-Party General Collateral Rate (TGCR): 0.01%, no change, $350B |

NY Fed Operational Purchases

Accepts $2.401bn of 1-7.5Y TIPS, Total Submitted $7.715bn

Coming up:

* Wed 5/12 1500ET Update NY Fed Operational Purchase Schedule

US OPTIONS SUMMARY

Wednesday's options flow included:

- EDM2 93/96 p/s ppr pays 2.25 on 10k (bid 5k) f=9977

- EDZ2 96/97/98 c-fly ppr pays 4 on 10k (bid)

- 2EM1 9918/9925/9937 broken p-fly trades 1.75/2.25

- 2EM1 9912/9925/9937 p-fly trades 1.5/2.75

EGBs-GILTS CASH CLOSE: Core FI Falls Alongside Equities

A rout in global equities (FTSE-2.5%, DAX -1.8%) did nothing to offset a big drop in core global FI, with Bunds and Gilts underperforming Treasuries amid strong bear steepening.

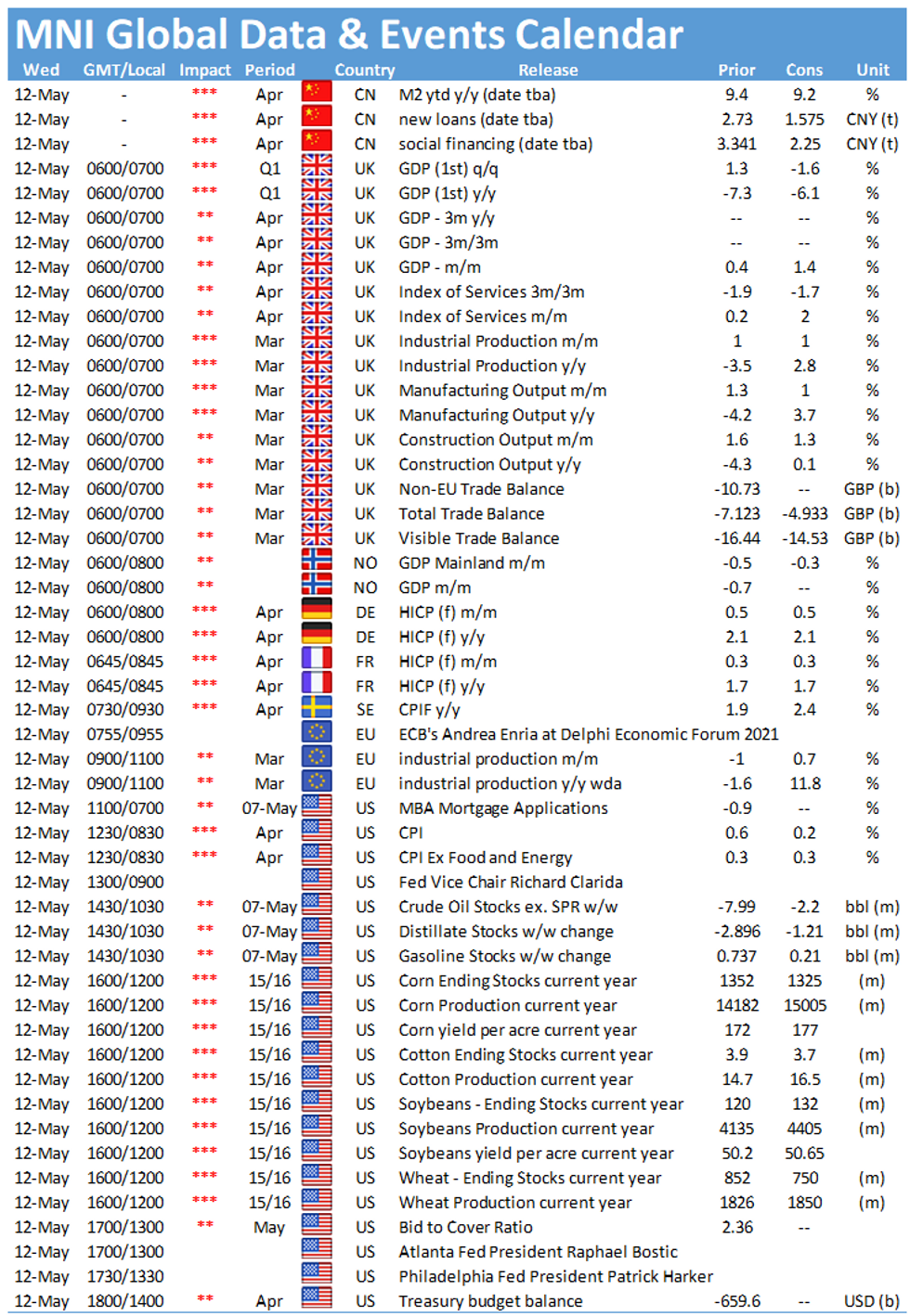

- The overall risk-off tone was set early with tech stocks continuing to fall; but on the bond side it appeared to be more concern on the inflation / supply side of things that roiled markets, particularly ahead of Wednesday's key US CPI release.

- Bund / Gilt yields closed near session highs, with curves on the steeps. Periphery EGBs largely contained though, with BTP spreads barely changed.

- In data, German ZEW sentiment beat expectations (21-year high). No surprises in UK Queen's Speech.

- In supply, today we got GBP4.5bn in Gilt sales, and German syndication of 30-Yr Green Bond.

- Wednesday sees a Portugal OT auction, UK GDP, and some EZ Final CPI data.

Closing yields/10-Yr Spreads to Bunds:

- Germany: The 2-Yr yield is up 1.8bps at -0.668%, 5-Yr is up 4.2bps at -0.549%, 10-Yr is up 5.1bps at -0.161%, and 30-Yr is up 4.9bps at 0.408%.

- UK: The 2-Yr yield is up 2.6bps at 0.064%, 5-Yr is up 3.4bps at 0.355%, 10-Yr is up 4.5bps at 0.833%, and 30-Yr is up 5.9bps at 1.388%.

- Italian BTP spread up 0.7bps at 114.7bps / Spanish spread up 0.3bps at 68.2bps

EUROPE OPTIONS SUMMARY: Mix Of Rates Trades

Wednesday's options flow included:

- RXM1 171/169/168 broken p fly sold at 101 in 2.75k (profit taking)

- RXM1 171/170.5ps. Sold at 35,in 4.5k (profit taking)

- RXM1 168/167ps, bought for 6 in 3k

- DUM1 112.10/112.20/112.30c fly, bought for 1.5 in 1.25k

- 3RZ1 99.87/99.62ps vs 100.25/100.37cs, bought the ps for flat in 2k (ref 100.09, -30 del)

- 2LM1 99.62c, bought for 0.75 in 5k (ref 99.47, 12d)

- 3LZ1 99.00/98.62ps vs 2LU1 99.25p, bought the 3yr os for 4.25 in 5k

FOREX: Currencies Calm Despite Equity Market Rout

- Currency markets were a relative calm Tuesday, despite the continued volatility in equity markets, which spread beyond the tech sector to draw the Dow Jones Industrial Average lower by near 1.5%.

- The USD's weakness on Monday carried through for much of the Tuesday session, with the likes of EUR/USD and GBP/USD hovering just below the week's highs. After an uneventful European morning, JPY and EUR shook to the top of the G10 pile, while CHF and NZD traded poorly.

- Inflation concerns remain a primary driver, with underlying gyrations in stocks to value from growth sectors prompting some appetite for haven currencies.

- Focus Wednesday rests on the US CPI release for April, with the Y/Y headline CPI release seen lurching higher to 3.6% from 2.6% previously. Other key releases include UK GDP and Eurozone industrial production numbers.

- Fedspeak remains key for the market outlook, with speeches scheduled from Fed's Clarida, Rosengren, Bostic and Harker. BoE's Bailey is also on the docket.

FX OPTIONS: Expiries for May12 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.2000(E542mln)

- USD/JPY: Y108.25-35($769mln), Y109.95-00($783mln)

- AUD/USD: $0.7900(A$619mln)

- USD/CAD: C$1.2800($610mln)

EQUITIES: Tech Bounce Saves NASDAQ Blushes

- After an impressive open for US equity markets (volumes surged in futures markets to the highest level since late January), markets were met with sizeable dip-buying, which helped spare the NASDAQ and broader US equity indices from further pronounced losses.

- At the open, the TICK Index detected what looked like the biggest equity selling program in decades, with 2,069 names sold. This coincided with new one-month lows of 4103.75, but a decent recovery in Tech giants including Tesla, Amazon, Facebook and others limited downside.

- Instead, the Dow Jones was Tuesday's underperformer, with energy the weakest sector alongside industrials and financials.

- S&P 500 heads into the close lower by 0.9%, the Dow Jones lower by 1.4%, while the NASDAQ has limited losses to 0.3%.

COMMODITIES: Oil Erases Early Losses on Supply Scramble

- WTI and Brent crude futures initially followed equity markets lower, with both benchmarks shedding close to 1% before a supply scramble in the US underpinned prices.

- The cyber-attack on the Colonial Pipeline over the weekend had a limited impact on prices initially, but supply is now dwindling. There have been sporadic reports of empty gas pumps, limited refinery activity and no visibility on when the pipeline will be back to full capacity, underpinning a recovery in WTI prices. WTI futures briefly showed back above $65/bbl.

- The gold/silver ratio resumed the multi-month downtrend Tuesday despite a recovery off the session lows for the yellow metal. Gold continues to find firm resistance ahead of the 200-dma at 1850.05, with this level successfully containing prices for a third session. 1811.41 undercuts as first support.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.