Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSY SUMMARY

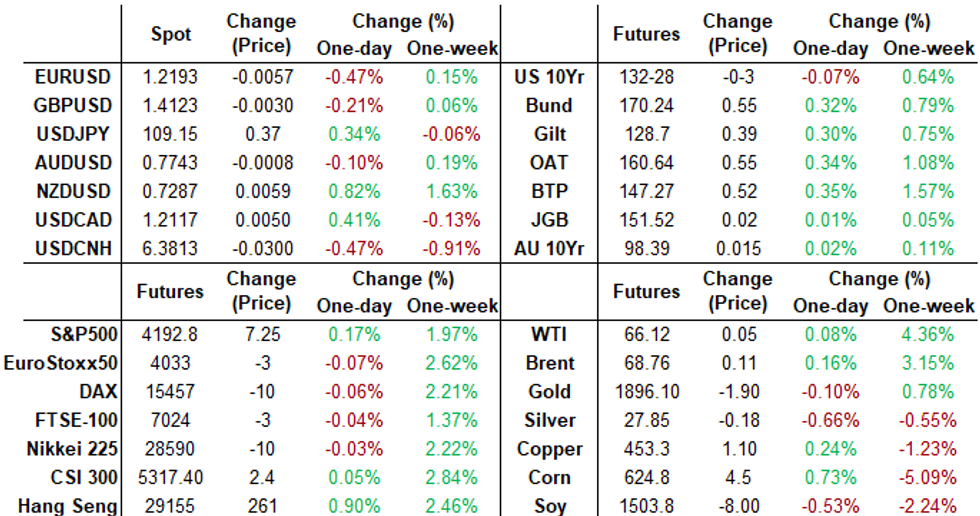

Hectic midday trade was book-ended by rather sedate trade through much of the first half and later in the second half Wednesday.- Tsys gradually inched higher through the first half, as did the greenback, USD index climbing back above the 90.00 and off yesterday's multi-month lows.

- No substantive data, focus was on rolling Jun/Sep quarterly Tsy futures ahead Fri's first notice when Sep takes lead, and the $61B 5Y Note auction.

- Complete debacle in 30Y roll around 1220ET saw spd gap up to 2-26 high on appr 16,300 -- since adjusted by exchange: all spds from 1-26.25 to 2-26 adjusted to 1-26.25 (new session high). While the spd looks to set around 1-19.25, there were appr nine 30k clips that traded at 1-18.25 AFTER the gap bid. Unintended consequence of fat finger: bonds extended session highs briefly after the error but quickly retraced, trading lower in last hour. It also appears more spds traded than needed rolling: % complete appr 108% according to CME site. B

- The $61B 5Y note (91282CCF6) auction traded through .7bp: high yield of 0.788% vs. 0.795% WI. Bid-to-cover highest since September 2020 at 2.49x vs. 2.33x 5 month average.

- The 2-Yr yield is up 0.5bps at 0.1466%, 5-Yr is up 0.8bps at 0.7791%, 10-Yr is up 1.9bps at 1.5774%, and 30-Yr is up 1.8bps at 2.2654%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest Settles

- O/N -0.00175 at 0.05888% (-0.00088/wk)

- 1 Month +0.00250 to 0.09250% (+0.00088/wk)

- 3 Month -0.00350 to 0.13500% (-0.01200/wk) ** (Record Low)

- 6 Month -0.00500 to 0.17175% (-0.00700/wk)

- 1 Year -0.00412 to 0.25188% (-0.00775/wk)

- Daily Effective Fed Funds Rate: 0.06% volume: $65B

- Daily Overnight Bank Funding Rate: 0.04% volume: $261B

- Secured Overnight Financing Rate (SOFR): 0.01%, $877B

- Broad General Collateral Rate (BGCR): 0.01%, $376B

- Tri-Party General Collateral Rate (TGCR): 0.01%, $353B

- (rate, volume levels reflect prior session)

- Tsys 2.25Y-4.5Y, $8.401B accepted vs. $40.237B submission

- Next scheduled purchases:

- Thu 5/27 1010-1030ET: Tsy 22.5Y-30Y, appr $2.025B

- Fri 5/28 1010-1030ET: Tsy 0Y-2.25Y, appr $12.425B

MONTH-END EXTENSIONS/PRELIM: Barclays/Bbg Extension Estimates for US

Preliminary forecast summary compared to avg increase for prior year and same time in 2020. TIPS 0.02Y. Note: fairly steady to year ago levels, while MBS extension est gains.

| Estimate | 1Y Avg Incr | Last Year | |

| US Tsys | 0.12 | 0.08 | 0.11 |

| Agencies | 0.04 | 0.11 | 0.01 |

| Credit | 0.10 | 0.08 | 0.08 |

| Govt/Credit | 0.10 | 0.08 | 0.10 |

| MBS | 0.13 | 0.06 | 0.05 |

| Aggregate | 0.11 | 0.08 | 0.09 |

| Long Gov/Cr | 0.10 | 0.09 | 0.10 |

| Iterm Credit | 0.08 | 0.07 | 0.08 |

| Interm Gov | 0.09 | 0.08 | 0.08 |

| Interm Gov | 0.09 | 0.08 | 0.08 |

| High Yield | 0.1 | 0.06 | 0.04 |

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- Block total 33,000 short Jul 95/96/97 put flys, 2.0

- -4,000 long Green Dec'23 75 puts, 13.5

- +3,000 Blue Sep 80 puts, 3.5

- +3,600 short Sep 95 puts, 1.5

- +5,000 short Dec 95/96 puts, 3.25

- -5,000 short Dec 96 straddles, 18.5

- +5,000 short Mar 96 straddles, 27.5

- 1,750 Green Jul 98.93/99.25 strangle vs. Green Sep 98.93/99.31 strangle

- Update, +17,000 short Dec 99.12/99.50 3x2 put spds, 6.0, includes 10k total Blocked

- Overnight trade

- Block, +5,000 short Dec 99.12/99.50 3x2 put spds, 6.0, more in pit

- Block, 3,500 Blue Jul 98.75/98.87 2x3 call spds, 4.0 net vs. 98.625/0.10%

- +7,000 short Sep 96/97 put spds, 3.0

- +5,000 Sep 99.81 puts, 1.0

- 4,000 Blue Sep 80/82/83/8 put condors

- -3,000 TYN 132/133.5 strangles, 31

- Overnight trade

- +8,000 wk4 10Y 131.25/wk1 10Y 131 put spd, rolling Fri's expiring option to next Fri, 3 net

- 15,000 wk1 TY 131 puts, 4

- Block, 5,000 TYN 132.5 calls, 23

EGBs-GILTS CASH CLOSE: Dovish Tone Continues

Bunds and Gilts continued to bull flatten Wednesday, largely holding onto gains made in the morning (with further ECB-speak indicating a dovish stance on PEPP, today from Panetta). Periphery spreads basically unchanged.

- In supply, Germany held a very weak (technically uncovered, 0.73x bid-to-cover) 15-Yr Bund auction, allotting E1.73bln; Italy sold E4.75bln of BTPei and short-term BTP.

- Not much in data, though French May confidence indices beat expectations.

- Ex-Gov't aide Cummings' testimony in Parliament on the govt's handling of the pandemic made for dramatic headlines, but little market impact.

- Thursday sees several speakers (ECB's de Guindos/Schnabel/Weidmann, BOE's Vlieghe) and Italian and German confidence data but no bond issuance.

Closing yields/10-Yr Spreads to Bunds:

- Germany: The 2-Yr yield is down 0.3bps at -0.666%, 5-Yr is down 2.4bps at -0.577%, 10-Yr is down 3.9bps at -0.206%, and 30-Yr is down 4.7bps at 0.349%.

- UK: The 2-Yr yield is up 0.7bps at 0.023%, 5-Yr is down 1.9bps at 0.302%, 10-Yr is down 3.4bps at 0.752%, and 30-Yr is down 3.8bps at 1.282%.

- Italian BTP spread up 0.1bps at 112.7bps / Spanish spread down 0.2bps at 65.8bps

OPTIONS/EUROPE SUMMARY: Large Bund Short Cover Features

Wednesday's options flow included:

- RXN1 167.5/166.5 ps, bought for 2 in 33.5k total. This is a short cover from the RXN1 169.5/168.5/167.5/166.5p condor, when it was bought for 24 in 35k

- 0LZ1 99.87/99.75/99.50p fly, bought for 0.25 in 1k

- 0LZ1 99.62/99.75/100.00 broken call fly bought for 2.75 in 7k. (Was bought for 2.5 yesterday in 20k)

- 2LU1 99.625/99.50 p/s sold to buy 2LZ1 99.375/99.125 p/s, bought for 0.25 in 20k

- 3LU1 98.62/37/25 broken p fly sold at 0.75 in 4k (closing)

- 3LU1 99.00/99.12/99.25/99.50c condor, bought for 0.5 in 4k

FOREX: USD Regains Lustre, Markets Suspect Month-End Flow

- The greenback initially traded steady-to-lower Wednesday, with EUR/USD holding close to recent highs ahead of NY hours. Markets changed tack into the WMR fix, however, with the USD index climbing back above the 90.00 and off yesterday's multi-month lows.

- Most sell-side month-end models pointed toward USD demand into the May close, and with May's final fix falling on a UK bank holiday, markets suspect some of this flow may be brought forward into the final few sessions of this week.

- NZD held its place among the day's best performers, although markets drifted off the multi-month highs printed at 0.7316 post-RBNZ decision. NOK and SEK were among the day's worst performers.

- Notable data releases pick up Thursday, with Italian consumer confidence, weekly US jobless claims and prelim April durable goods orders on the docket. Pending home sales data also crosses which may be worth watching given the sizeable miss in new home sales earlier in the week.

FX OPTIONS: Expiries for May27 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.2200(E549mln)

- AUD/USD: $0.7770-80(A$654mln)

- USD/CAD: C$1.2100-25($1.2bln-USD puts), C$1.2195-1.2205($1.4bln)

PIPELINE: $3B Morgan Stanley Launched

- Date $MM Issuer (Priced *, Launch #)

- 05/26 $3B #Morgan Stanley 4NC3 fix to FRN +48

- 05/26 $2B #UniCredit 6NC5 +145a, 11NV10 +180a

COMMODITIES: Gold Rally Extends, Oil Flat

- The recent gold rally extended Wednesday, boosting the spot price north of $1900/oz to hit new multi-month highs. Gold gains came despite broad USD strength into the fix, extending the rally from the March lows to over $200/oz.

- Gold bulls may be wary of the over-extended RSI, which has crept to its most overbought level since August of last year. Markets watch for a price signal reversal pattern in the near-term to confirm the significance of the RSI at this stage.

- Oil markets were largely inactive, with WTI and Brent crude futures inside the week's range. Weekly DoE crude oil inventories numbers had little market impact, despite the headline draw of 1.7mln bbls being larger than expectations.

EQUITIES: Steady Trade, But Inside Tuesday Range

- Global equity markets had a more steady session Wednesday, with the e-mini S&P trading wholly inside the Tuesday range throughout. This keeps directional parameters unchanged for now, with the first upside level resting at 4212.75.

- In cash markets, the NASDAQ outperformed core S&P and Dow Jones indices as sentiment steadied.

- The consumer discretionary sector traded particularly well thanks to a 2.5% rally in Nike and Under Armour shares. Re-opening linked names continue to outperform, with Penn National Gaming, Las Vegas Sands and Wynn Resorts among the best performers in the S&P 500. Gains in these sectors were tempered somewhat by healthcare and materials names, which traded somewhat softer.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok