Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY: Dovish Cues

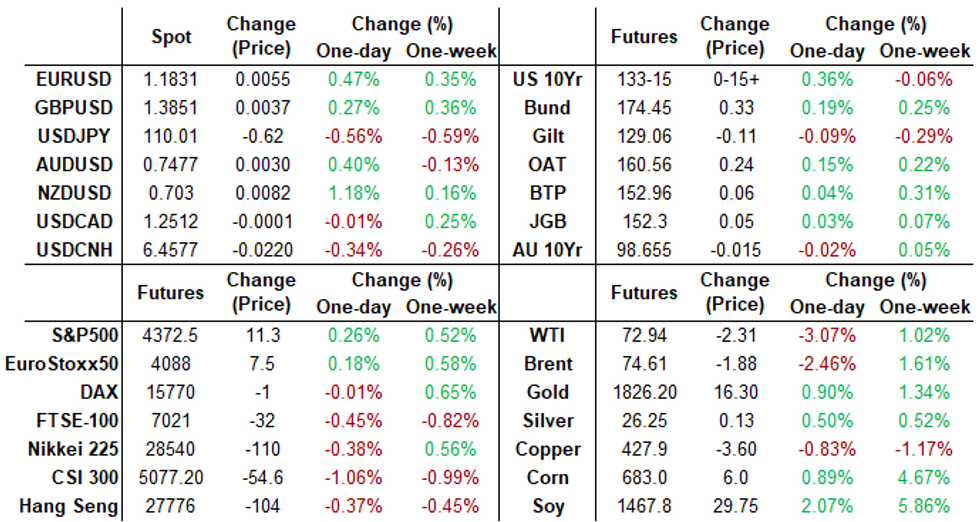

Tsy futures finished strong Wednesday, near late session highs after the bell, long end leading on moderate volumes (TYU >1.3M), curves bull flattening.- Rates took early dovish cues from prepared text of Fed Chairman Powell's testimony to the House Committee on Financial Services. Cooling the chances of tapering in July after Chairman Powell noted the need for continued discussions "in coming meetings".

- JUN FINAL DEMAND PPI (+1.0%, EX FOOD, ENERGY +1.0%) largely ignored. Sources reported real- and fast$ buying in intermediates, dealer buying in long end in early trade. Rates continued to drift back into Mon-Tues range as Chairman Powell's Q&A portion got underway.

- Large Eurodollar flow: +50,000 EDM2 99.755 (+0.035) 99.76 last, lent further support for lead into Red packs (EDU2-EDM3) as tighter policy expectations cooled slightly.

- Bonds climbed higher following US/CHINA geopolitical risk headline: U.S. TO EXTEND TRUMP-ERA HALT TO ECONOMIC DIALOGUE WITH CHINA, Bbg, Excerpt: "While Yellen's team, and those of other departments, are in touch with Chinese counterparts, the expectation for now is not to restart formal high-level talks, according to people familiar with the situation" Bbg.

- The 2-Yr yield is down 2.6bps at 0.227%, 5-Yr is down 4.8bps at 0.7977%, 10-Yr is down 6.2bps at 1.3543%, and 30-Yr is down 5.8bps at 1.9889%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest Settles

- O/N -0.00025 at 0.08538% (-0.00125/wk)

- 1 Month -0.00200 to 0.09113% (-0.00900/wk)

- 3 Month +0.00025 to 0.12638% (-0.00225/wk) ** (Record Low: 0.11800% on 6/14)

- 6 Month -0.00075 to 0.15075% (-0.00025/wk)

- 1 Year -0.00025 to 0.24300% (+0.00413/wk)

- Daily Effective Fed Funds Rate: 0.10% volume: $74B

- Daily Overnight Bank Funding Rate: 0.08% volume: $249B

- Secured Overnight Financing Rate (SOFR): 0.05%, $875B

- Broad General Collateral Rate (BGCR): 0.05%, $361B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $331B

- (rate, volume levels reflect prior session)

- Tsy 10Y-22.5Y, $1.401B accepted vs. $3.774B submission

- Next scheduled purchases

- Thu 7/15 1010-1030ET: Tsy 0Y-2.25Y, appr $12.425B

- Fri 7/16 1010-1030ET: Tsy 7Y-10Y, appr $3.225B

FED: Reverse Repo Operations

NY Fed reverse repo usage climbs to $859.975B from 75 counterparties vs. $798.267B on Tuesday. Remains well off June 30 record high of $991.939B.

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- +7,500 Red Sep'22 99.87 calls, 2.5 vs.99.66/0.18%

- -7,500 Green Sep 91 calls 4.0 over the 88/90 put spds vs. 99.10/0.64%

- +5,000 short Aug/short Sep 99.687 put strip, 10.5-1

- -1,500 Blue Sep 80/82/85 put flys, 3.25

- Overnight trade

- 8,400 Dec 99.81/99.87/99.93 call flys

- 5,000 Sep 99.81/99.87 put spds

- 3,500 Green Mar 100 calls

- -3,000 TYU 131 puts, 8

- +4,000 TYU 128.5 puts, 2

- Update, over 11,000 TYQ 132.25 puts on day from 5-2, 2 last

- +5,000 FVU 122.5

- +9,500 TYQ/TYU 133 put calendar spd, 27

- +5,000 FVU 123 puts, 10

- Overnight trade

- 25,000 TYU 132/133 2x1 put spds

- 10,000 TYU 130 puts, 5

- 15,000 TYQ 132.5 puts, 7-8

- 3,500 FVU 122.5 puts, 6

- 16,000 USU 158 puts, mostly 38

EGBs-GILTS CASH CLOSE: The Long End Comes Back

Bunds and Gilts bull flattened Wednesday after early weakness, following the lead of Treasuries which strengthened on dovish-leaning Congressional testimony by Fed Chair Powell.

- Gilts had sold off early on strong UK June inflation data out in the morning. Eurozone industrial production data disappointed, but that was considered stale (May).

- Periphery spreads widened slightly, with 10Y BTPs failing to break the 100bps mark.

- Supply came from Germany (Bund, EUR3.392bn allotted) and Portugal (OTs, EUR914mn).

- Thursday sees UK labor market data, and Spanish and French bond supply, plus comments from BOE's Saunders.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.6bps at -0.678%, 5-Yr is down 1.9bps at -0.618%, 10-Yr is down 2.5bps at -0.319%, and 30-Yr is down 3.4bps at 0.177%.

- UK: The 2-Yr yield is down 1.1bps at 0.082%, 5-Yr is up 0.2bps at 0.297%, 10-Yr is down 0.5bps at 0.627%, and 30-Yr is down 2.2bps at 1.103%.

- Italian BTP spread up 2bps at 102.9bps / Spanish up 1.6bps at 63.2bps

OPTIONS/EUROPE SUMMARY: All About Rates (Including Some SONIA)

Wednesday's options flow included:

- 0RQ1 100.50/100.37ps, bought for 3.25 in 2k

- 2RH1100.25/100.12ps vs 100.50/100.62cs, sold the ps at half in 8k (ref 100.36, -20 del)

- 0LV1 99.62/99.50/99.25p fly, bought for 2.25 in 2k

- 0LU1 with 0LZ1 99.87/100cs strip, bought for 0.5 in 2.5k

- 0LU1 99.50p, bought for 3 in 2k

- 0LU1 99.50/99.25ps, bought for 2 in 10k

- 0NZ1 (SONIA) 0NZ1 99.80/99.90/100c fly, bought for 1 in 2k

- 0LZ1 99.37/99.62 RR, sold the put at 0.25 in 20k (ref 99.52)

- 0LZ1 99.62/99.50/99.37p ladder, bought for 2.75 in 4.5k

- 3NV1 99.60c, bought for 2.5 in 2k (ref 99.30)

FOREX: Softer Greenback Helps Kiwi Extend Gains

- Federal Reserve Chair Jerome Powell reiterated that the central bank would continue its accommodative monetary policy despite a spike in CPI data. He described the U.S. job market as "still a ways off" from the progress the Fed wants to see before reducing stimulus.

- The dollar had been weaker in the lead up to the event and extended losses in the aftermath, in a fairly gradual and contained manner. The dollar index is 0.38% lower.

- USDCAD had a very brief spell of volatility following the BOC decision, where they left rates unchanged and tapered weekly buying to C$2B as expected. After a brief slip to 1.2428, USDCAD aggressively reversed, rising to 1.2521 as little indication was provided that these strong inflation readings are forcing the bank to re-evaluate their monetary policy.

- RBNZ inspired gains were extended in the Kiwi, the best G10 performer, rising 1.2% on Wednesday.

- EURUSD crept back above 1.18 and continued to slowly unwind yesterday's retreat to highs of 1.1836. Initial firm resistance is at 1.1881, the July 9 high.

- USDCNH had a flurry lower ahead of Powell's text release as lows from July 6th, 7th and 13th were all broken and the pair traded to the lowest level for a month. CNH held on to the majority of gains despite late negative headlines from the white house concerning US-China economic dialogue.

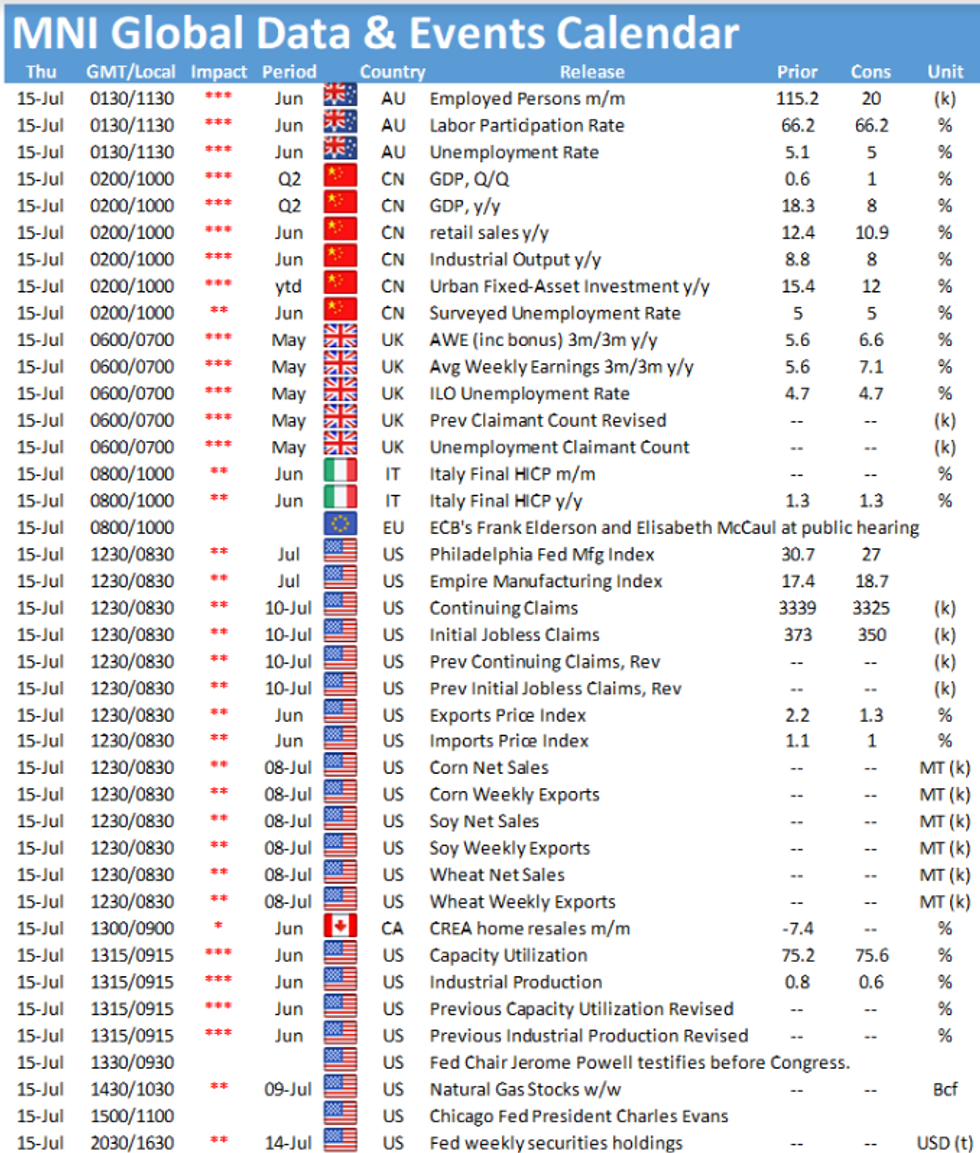

- Australian Employment data and Chinese GDP overnight before the UK also publish their employment figures on Thursday.

FX OPTION EXPIRY

- EURUSD: 1.1775 (342mln), 1.1800 (230mln), 1.1810 (761mln), 1.1850 (513mln)

- USDJPY: 110 (415mln), 110.50 (293mln), 110.75 (489mln)

PIPELINE: $5.5B Goldman Sachs 2Pt Lauched

- Date $MM Issuer (Priced *, Launch #)

- 07/14 $5.5B #Goldman Sachs $4B 11NC10 +103, $1.5B 21NC20 +100

- 07/14 $Benchmark New Development Bank 3Y +15a

- Rolled to Thursday:

- 07/15 $Benchmark African Development Bank (AFDB) 5Y +3a

EQUITIES

Key late session market levels:- DJIA up 50.93 points (0.15%) at 34888.79

- S&P E-Mini Future up 10.25 points (0.24%) at 4364

- European bourses closing levels:

- EuroStoxx 50 up 4.94 points (0.12%) at 4092.06

- FTSE 100 down 33.53 points (-0.47%) at 7090.55

- German DAX down 0.66 points (0%) at 15771.66

- French CAC 40 down 0.09 points (0%) at 6547.02

COMMODITIES: Oil Prices Retreat Roughly 2.5%

- Reports throughout Wednesday kept volatility in oil markets high and eventually led to a notable sell-off with WTI futures reaching $72.21 at its worst point of the day, residing down 2.7% as of writing.

- Overall, the UAE and Saudi Arabia appear to have resolved a dispute over a demand by the UAE to raise its production quota that could pave the way for an extension of producer cooperation and enable substantial volumes of oil supply to come back to the market.

- What happens next will depend upon deliberations at a yet-to-be announced, Opec+ ministerial meeting expected to take place this week ahead of the Islamic Eid on Jul. 19. The issue of the baseline change will also be discussed during the meeting by all members of the producer group.

- For reference, that meeting is not guaranteed to result in an agreement as other countries could raise similar requests on the back of the UAE's seeming success.

- Meanwhile, after an hour's delay, with the EIA citing a "technical issue," the U.S. government reported that U.S. crude inventories fell by 7.9 million barrels for the week ended July 9, marking an eighth weekly decline in a row.

- The broadly offered dollar propped up gold and silver prices, both rising just shy of 1%. Potential bullish technical developments in the yellow metal as the 50-day EMA at $1813.4 has broken today. The EMA represented a key resistance area. Price extended to a high of $1829.89, just below $1833.7, a Fibonacci retracement.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok