Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSY SUMMARY: No Hawks To Temper Tsy Rally, 30YY Sub-1.92%

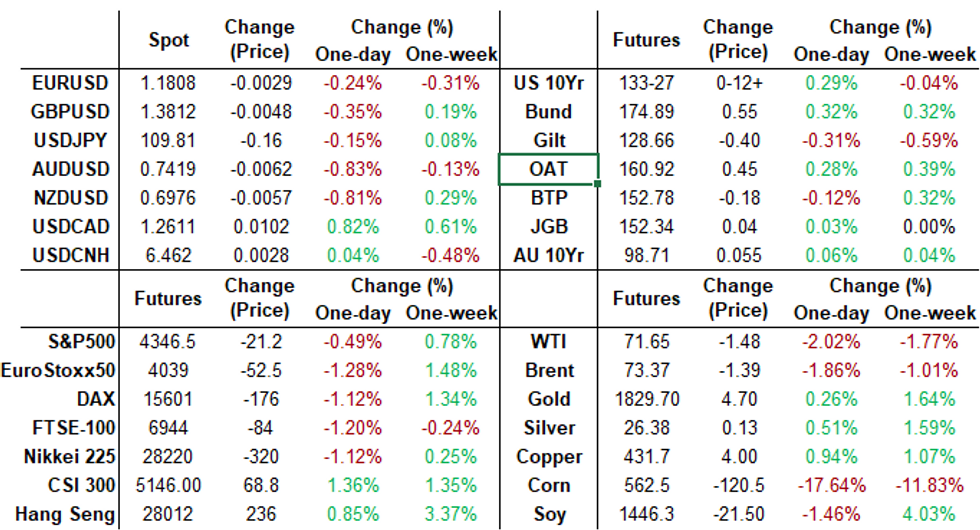

Overnight support for US rates carried through Thursday's session, 30Y Bonds lead the charge all day, finishing just off highs, yield curves flatter. Intermediates lagged slightly, 10Y futures tested first resistance of 133-26.5 several times before settling back around -25 to -25.5.

- Support for Tsys picked up early in the second half (30YY slips to 1.9160% low) as Chicago Fed Pres Evans headlines make the rounds:

- "The upside potential for inflation isn't quite as strong and sustainable as I would like," adding "SLIGHTLY MORE PERSISTENT INFLATION WOULDN'T BE BAD" while "I don't think you can get 2.5% to 3% year after year on the basis of these relative price increases".

- Tsy Sec Yellen also spoke on NPR later in day but didn't saying anything new, or particularly market moving: expecting inflation to fade over the mid-term.

- Fed Chair Powell's semiannual mon-pol report to the Senate failed to illicit much of a market reaction either.

- Bonds maintain strong bid after flurry of data, weekly claims little higher than exp at 360k vs. 350k est while continuing claims inch lower again: -126k to 3.241M vs. 3.3M est.

- The 2-Yr yield is up 0bps at 0.2231%, 5-Yr is down 2.1bps at 0.7736%, 10-Yr is down 4.9bps at 1.2972%, and 30-Yr is down 5.1bps at 1.9199%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest Settles

- O/N +0.00025 at 0.08563% (-0.00100/wk)

- 1 Month -0.00200 to 0.08913% (-0.01100/wk)

- 3 Month +0.00750 to 0.13388% (+0.00525/wk) ** (Record Low: 0.11800% on 6/14)

- 6 Month +0.00250 to 0.15325% (+0.00225/wk)

- 1 Year -0.00200 to 0.24100% (+0.00213/wk)

- Daily Effective Fed Funds Rate: 0.10% volume: $72B

- Daily Overnight Bank Funding Rate: 0.08% volume: $246B

- Secured Overnight Financing Rate (SOFR): 0.05%, $908B

- Broad General Collateral Rate (BGCR): 0.05%, $361B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $329B

- (rate, volume levels reflect prior session)

- Tsy 0Y-2.25Y, $12.401B accepted vs. $48.705B submission

- Next scheduled purchase

- Fri 7/16 1010-1030ET: Tsy 7Y-10Y, appr $3.225B

FED: Reverse Repo Operations

NY Fed reverse repo usage slips to $776.261B from 69 counterparties vs. $859.975B on Wednesday. Remains well off June 30 record high of $991.939B.

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- +12,000 Red Sep'22 99.87 calls, 3.0 vs. 99.685/0.18%

- +10,000 Mar 99.81/99.87 put spds, 3.0

- +8,000 Red Dec 99.50 puts, 16.5

- -5,000 Dec 99.75 puts, 1.0 vs. 99.825/0.05%

- -5,000 Dec 99.62 puts, 0.25

- +5,000 Gold Sep 97.87/98.00 put spds, 1.0

- +20,000 short Oct 99.12/99.37 put spds, 3.0

- +2,000 Green Dec 86.5/88 put spds even over 91/92.5 call spds

- -1,000 Blue Sep 98.75 straddles, 27.5

- Overnight trade

- +5,000 Jun'22 99.50/Red Sep'22 99.50/Red Dec'22 99.25 put strips, 23.0

- 2,000 Green Dec 99.00/99.12 put spds vs. 99.25/99.37 call spds

- 1,750 Blue Jul 98.62/98.75 call spds

- +5,000 FVQ 123.25/123.5 put spds, 2 vs. 123-27.25/0.10%

- -1,300 TYU 133.5 straddles, 133

- +2,500 TYQ 132.5 puts, 3

- Overnight trade

- >+13,000 TYQ 134.25 calls, 6-10

- 7,000 TYQ 134.5 calls, 5-6

- 6,000 TYU 130 puts, 4

- 4,000 TYU 134 calls, 39 last after trading up to 43

- 4,000 FVU 122.5 puts, 4.5

- 3,000 FVU 121.25/122.25/123.25 put flys

EGBs-GILTS CASH CLOSE: Hawkish Saunders Sinks Gilts

Gilts underperformed Thursday after the BoE's Saunders suggested that it may soon be appropriate to withdraw pandemic stimulus. The Gilt move also weakened Bunds (and Treasuries), with bear steepening in the curves and periphery spreads widening.

- Prior to Saunders' comments at 1100BST, it was shaping up as a constructive morning for core FI, with some bull flattening resuming from Wednesday.

- By comparison, data didn't really have much impact (UK jobs data basically in line with expectations). It was a fairly heavy supply day, with E10.5bln in French OATS and E1.7bln in linkers, and Spain selling E3.5bln - but again, no discernable impact.

- Friday sees no tier-1 data (Eurozone inflation figures are finals), no bond supply, and no scheduled ECB / BoE speakers.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany:

- Germany: The 2-Yr yield is up 0.1bps at -0.677%, 5-Yr is down 0.6bps at -0.624%, 10-Yr is down 1.5bps at -0.334%, and 30-Yr is down 2.5bps at 0.152%.

- UK: The 2-Yr yield is up 6.5bps at 0.147%, 5-Yr is up 6.1bps at 0.358%, 10-Yr is up 3.5bps at 0.662%, and 30-Yr is up 4.2bps at 1.145%.

- Italian BTP spread up 2.5bps at 105.4bps/ Spanish up 0.9bps at 64.1bps

OPTIONS/EUROPE SUMMARY: Sterling Put Spreads And Vol Trades

Thursday's options flow included:

- DUU1 112.20/112.10/112p fly 1x3x2, bought for 1 in 1.5k

- RXU1 173.50/172.50ps 1x1.5, bought for 9.5 in 2k

- RXU1 173.50/175cs 1x2 sold at 15 in 2.5k (ref 174.63)

- 0LU1 99.50/99.37ps with 0LQ1 99.50p, bought for 3.25 in 5k

- 0LU1 99.50/99.37ps 2x1, bought the 2 for 4.25 and 4.5 in 10k

- 0LZ1 99.50^, bought for 21 in 1k

- 0LZ1 99.62^ vs 99.50p, sold at 10.5 in 3k

- 2LU1 99.37/99.50cs 1x2, bought for 1.5 in 4k

- 3LU1 99.25/99.37cs vs 0LU1 99.62/99.75cs, bought the 3yr for 3.25 in 9k

FOREX: US Dollar Regains Poise As Equities Drift Lower

- The Greenback spent the latter half of Thursday reversing the prior day's losses. Dollar indices are roughly 0.3% above yesterday's closing marks.

- Significantly weak sessions for Aussie and Kiwi, retreating the best part of 1%, amid the decline in global equity indices and an extension lower in crude futures.

- Similar declines seen in the Canadian dollar, adding to negative price action following yesterday's BOC statement. Following a recent resumption of the uptrend in USDCAD that started Jun 1, a bullish price sequence of higher highs and higher lows has been established. Additionally, moving average studies are in a bull mode. July 8th highs have been breached through 1.2590, with stronger resistance noted at 1.2653, Apr 21 high.

- More contained price action in EURUSD, edging gradually back below the 1.18 handle and USDJPY appearing content around the 110 mark.

- The move lower in oil put pressure on the Norwegian Krone. EURNOK continued its most recent upward trajectory, briefly reaching the highest levels seen since March 1st in the pair at 10.4359.

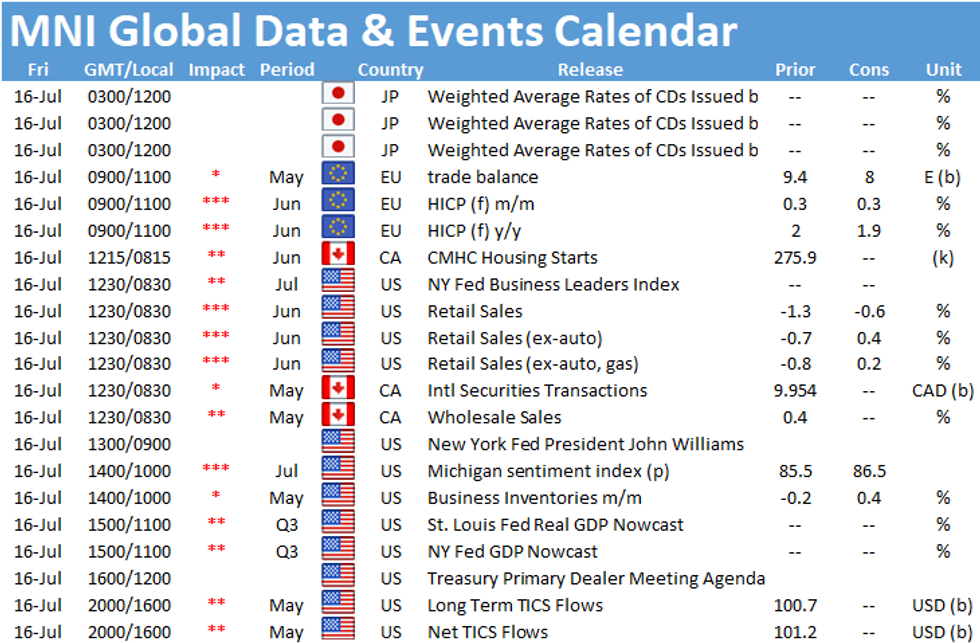

- New Zealand inflation data due later this evening, before the Bank of Japan will release their monetary policy statement and hold a press conference.

- Friday's docket will be headlined by final CPI readings from the Eurozone and then US Retail Sales.

FX OPTION EXPIRY

- EURUSD: 1.1800 (653mln), 1.1805 (250mln), 1.1900 (372mln), 1.1910 (366mln)

- USDJPY: 109.80 (500mln), 109.90 (200mln), 110.05 (545mln), 110.10 (370mln), 110.35(284mln)

- AUDUSD; 0.7470 (249mln), 0.7500 (2.15bn)0.7510 )297mln)

- USDCAD: 1.2500 (421mln)

PIPELINE: $7.75B BoA 3Pt Launched

- Date $MM Issuer (Priced *, Launch #)

- 07/15 $8.5B #Morgan Stanley $2B 3.5NC2.5 +57, $3B 6NC5 +75, $3.5B 11NC10 +95

- 07/15 $7.75B #Bank of America $2B 6NC5 tap +77, $3.75B 11NC10 +100, $2B31NC30 +103

- 07/15 $2.75B *African Development Bank (AFDB) 5Y +1

- 07/15 $2.25B *New Development Bank (NDB) 3Y +14

- 07/15 $1.3B #Royalty Pharma $600M 10Y +105, $700M 30Y +155

- 07/15 $1B ADT Security 8Y 4%a

- 07/15 $Benchmark Cibanco 10Y +325a

- 07/?? $1.2B Xiaomi $800M 10Y, $400M 30Y Green bond

EQUITIES

Late session market levels- DJIA down 16.18 points (-0.05%) at 34908.68

- S&P E-Mini Future down 22.75 points (-0.52%) at 4343.75

- Nasdaq down 127.7 points (-0.9%) at 14511.78

Prior European bourses closing levels:

- EuroStoxx 50 down 43.11 points (-1.05%) at 4056.39

- FTSE 100 down 79.17 points (-1.12%) at 7012.02

- German DAX down 159.32 points (-1.01%) at 15629.66

- French CAC 40 down 65.02 points (-0.99%) at 6493.36

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.