Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSY: Bull Flattening, Knock-On Effect Of BoC's Hawkish Forward Guidance

Knock-on effect of Bank of Canada's hawkish policy annc Wed (steady rate but ending QE/moves to reinvestment phase pushes forward rate liftoff from 2H22 to midyear) weighed heavily on short end rates, particularly Eurodlr Sep'22 to Red Jun'23, trading 0.085-0.100 lower at one point. A bit of "tail wags dog" scenario desks quipped, while inflation concerns supported the long end.- Heavy volumes (TYZ1>2.2M, USZ>1.4M) as Tsy yield curves bull flattened to new 18 month lows, 30YY tapped 1.9307% low.

- Active second half players include dealer and prop accts selling 2s-3s, fast and Real$ +5s-10s, Real$ and bank portfolio buying 30s, deal-tied unwinds and curve steepener stop-outs as well. After a large 2s5s steepener Block around midday, a 5s/30s ultra bond flattener block crossed.

- Post-Note auction support: Tsy futures gapped higher after 2.3bp stop -- decent $61B 5Y note auction (91282CDG3) with 0.157% high yield vs. 1.180% WI; 2.55x bid-to-cover surge vs Sep's 2.37x (lowest since 2008) well over five auction avg: 2.38x. Indirect take-up: 64.78% new 2021 high after 54.3% 2021 Low last month.

- Equities had been posting modest gains in late trade sold off after Bbg headline noted: SENATE FINANCE CHAIRMAN WYDEN SAYS BILLIONAIRES TAX IS NOT DEAD.

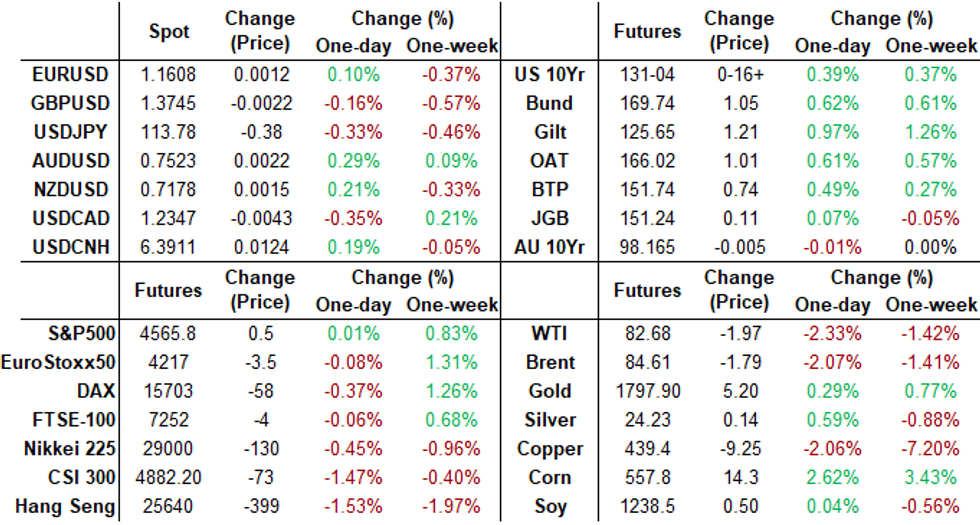

- The 2-Yr yield is up 4.8bps at 0.4872%, 5-Yr is down 3.9bps at 1.1351%, 10-Yr is down 8.2bps at 1.5256%, and 30-Yr is down 10.2bps at 1.9383%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N -0.00213 at 0.06950% (-0.00400/wk)

- 1 Month +0.00000 to 0.08700% (-0.00088/wk)

- 3 Month -0.00725 to 0.12863% (+0.00375/wk) ** Record Low 0.11413% on 9/12/21

- 6 Month +0.00338 to 0.17963% (+0.00763/wk)

- 1 Year +0.00950 to 0.33225% (+0.01538/wk)

- Daily Effective Fed Funds Rate: 0.08% volume: $77B

- Daily Overnight Bank Funding Rate: 0.07% volume: $276B

- Secured Overnight Financing Rate (SOFR): 0.05%, $877B

- Broad General Collateral Rate (BGCR): 0.05%, $356B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $326B

- (rate, volume levels reflect prior session)

- Tsy 10Y-22.5Y, $1.401B accepted vs. $4.300B submission

- Next scheduled purchases

- Thu 10/28 1010-1030ET: Tsy 0Y-2.25Y, appr $12.425B

- Fri 10/29 1010-1030ET: Tsy 10Y-22.5Y, appr $1.425B

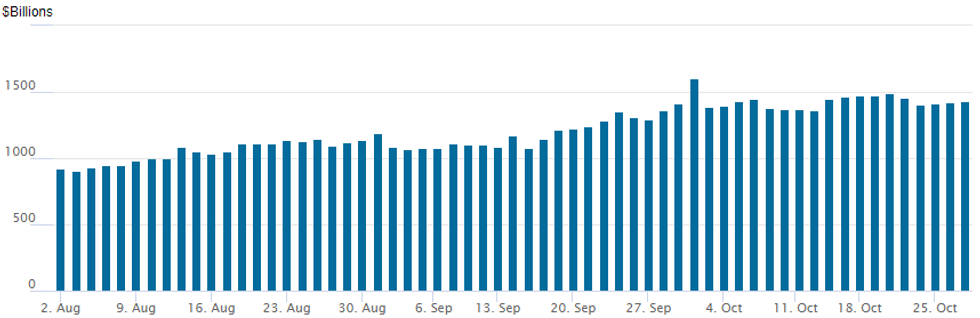

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage climbs to $1,433.370B from 75 counterparties from $1,423.198B on Tuesday. Record high remains at $1,604.881B from Thursday, September 30.

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- Block, 10,000 Mar 99.62 puts, 3.25 vs. 99.765

- -15,000 Dec 99.12 puts, 10.0

- -5,000 short Dec 99.25/99.37 put spds, 8.5

- Block, -70,000 short Dec 99.25/99.37 put spds, 7.5

- -20,000 short Dec 99.37/99.62 1x2 call spds

- +10,000 short Nov 99.37/99.62 2x1 put spd 0.25 over 99.37 calls

- +4,000 short Dec 99.25/99.37/99.50 1x3x2 call fly earlier

- Overnight trade

- 7,250 Blue Dec 98.25/98.50 put spds vs. 98.75/98.87 call spds

- 1,500 Green Dec 98.62/98.75 put spds vs. Blue Dec 98.25/98.37 put spds

- 3,000 Jun 99.00/99.25 put spds

- 5,600 FVZ 121/121.25/121.75 put trees, 4 net/2-legs over

- -8,000 FVZ 121.5 puts, 21.5

- Block, 7,500 TYZ 129/130 2x1 put spds, 4

- Overnight trade

- 7,000 FVZ 121.75 puts, 25

- Block, 20,000 FVZ 121.25 puts, 15.5

- Block, 5,000 TYZ 129/130 3x2 put spds, 18

EGBs-GILTS CASH CLOSE: Gilts Rally Amid Big Issuance Reduction

Long-end Gilt yields fell by the most since March 2020 Wednesday, outperforming Bunds (which still saw one of the biggest rallies of 2021).

- Alongside today's UK budget release, DMO announced a reduction in Gilt issuance of GBP57.8bln in 2021-22 vs the amount projected in April, which was beyond even the biggest sell-side expectations.

- That accelerated a Gilt rally that started in the morning, with yields closing near the lows.

- Periphery EGBs couldn't quite keep pace with Bunds, leaving spreads a little wider. GGBs underperformed; Portugal weaker too amid continued political uncertainty and a short- for long-term bond exchange operation.

- Focus turns to flash October CPI and the ECB decision Thursday.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.3bps at -0.645%, 5-Yr is down 2.8bps at -0.469%, 10-Yr is down 6.3bps at -0.18%, and 30-Yr is down 8.9bps at 0.155%.

- UK: The 2-Yr yield is down 6.7bps at 0.559%, 5-Yr is down 9.8bps at 0.702%, 10-Yr is down 12.5bps at 0.985%, and 30-Yr is down 18bps at 1.136%.

- Italian BTP spread up 0.5bps at 111.8bps / Portuguese up 1.9bps at 55.2bps

EGB Options: Sterling Spreads Bought As UK Budget Unveiled

Wednesday's Europe bond / rate options flow included:

- DUZ1 112.10/112.00/111.90p fly was sold at 1.25 in 2k

- RXF2 170.5/174.5cs, bought for 135 in 2k vs 800 RXH2 at 170.93

- 0RU2 100p, was bought for 16.5/16.75 in 4k (ref 100.05)

- ERZ2 100.25^, was bought for 30.5/31 in 1.75k (ref 100.305)

- 0LZ1 98.87/99.00cs,1x1.5 bought for 4 in 10k

- 0LZ1 98.87/99.12cs, bought for 6 in 5k

- 2LZ1 98.62/98.37ps, bought for 5.25 in 10k

FOREX: USDCAD Sharply Lower Following Hawkish Bank of Canada

- A more hawkish than expected BOC statement prompted a strong immediate rally in the Canadian dollar. USDCAD had been in positive territory throughout early trade on Wednesday due to declining oil prices, however, appeared offered approaching the decision, trading from 1.2420 down to 1.2400.

- Following the release, the pair traded quickly down to 1.2340 and remained under short-term pressure as it traded down to 1.2301 lows in the aftermath. Cad gains consolidated throughout the US trading session with USDCAD content around 1.2340.

- Technically, the focus turns to the mid-October lows now well in range at 1.2288, with 1.2253 the most significant support of note, the June 23rd low.

- Elsewhere, GBP was under pressure as Chancellor Sunak announced details on the UK budget. Cable traded down to lows of 1.3710 but has since bounced back to 1.3750. EURGBP had a strong relief rally after holding above 0.8400 yesterday, to highs of 0.8465.

- A poorer day for the commodity complex did little to stifle the bid in AUDUSD and NZDUSD, which continue to both consolidate above the September highs.

- USDJPY, however, did suffer and made a new marginal low for October at 113.39 before bouncing into the close.

- EURCHF continues its steady retreat, edging below 1.0650 for the first time since July 2020. While the price action remains very slow, this may be worth monitoring if we start to approach lows at 1.0607 and the 2020 lows close to the 1.05 handle.

- Overnight, markets will await the Bank of Japan before German CPI data. Later on Thursday, the focus will turn to the ECB statement/press conference and the advance reading of US Q3 GDP.

FX: Expiries for Oct28 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600-10(E1.5bln), $1.1620-30(E811mln), $1.1650-65(E695mln)

- USD/JPY: Y113.00($1.5bln), Y113.70-90($2.3bln)

- AUD/USD: $0.7475(A$975mln), $0.7505(A$502mln)

- USD/CAD: C$1.2360-80($1.8bln)

- USD/CNY: Cny6.3900($805mln)

PIPELINE: $4B Citgroup 3Pt Launched, IBRD Priced Earlier

- Date $MM Issuer (Priced *, Launch #)

- 10/27 $5B *World Bank 10Y +7

- 10/27 $4B #Citigroup $1B 4NC3+52, $1.75B 11NC10+98, $1.25B 21NC20+98

- 10/27 $1.3B #NextEra 2NC.5 FRN/SOFR+40

- 10/27 $Benchmark US Bancorp 15NC10 +95a

- 10/27 $Benchmark Fifth Third investor calls

- Reverse Yankee

- 10/27 Yen/Benchmark Proctor & Gamble 5Y 0.11%a, 10Y 0.23%a

EQUITIES: Markets Balk at Billionaire Tax

- The Democrats released further details on a possible billionaires tax, with asset price gains seen being charged at a rate of 23.8% on an annual basis - a report which sent equity markets into negative territory ahead of the opening bell. This sentiment was reinforced by a solidly hawkish turn from the Bank of Canada, who brought forward the potential timing of the beginning of a tightening cycle.

- In cash equity markets, tech outperformed, helping boost the NASDAQ to outstrip both the S&P 500 and the Dow Jones thanks to solid earnings updates from Microsoft and Alphabet, which both added over 4% apiece following their reports.

- Earnings remain a focus through the end of the week, with reports due from Caterpillar, Merck, Mastercard and Amazon among others. Full timetable with analyst expectations here: https://marketnews.com/mni-us-earnings-schedule-bu...

COMMODITIES: Crude Hits Reverse as Iran Come Back to Negotiating Table

- WTI and Brent crude futures traded lower Wednesday, showing through the Monday and Tuesday lows as markets dipped after Iran announced a return to the negotiating table, an effective resumption of nuclear talks with Western powers that could unlock Iranian crude supply to the still toppy market.

- Downside in crude was compounded by a sizeable build in US crude inventories, with the DoE tracking a build of over 4.2mln bbls relative to expectations of just 1.5mln.

- Despite the turn lower, the broader outlook remains bullish, but markets remain cognizant of firm short-term support defined at $80.78, Oct 20 low, which represents a key near-term level.

- Gold maintains a positive short-term tone despite Tuesday's pullback and remains above the 50-day EMA. The yellow metal recently cleared resistance at $1800.6, Oct 14 high and this highlights a short-term bullish theme. Further gains would open $1834.0, the Sep 3 high. On the downside, a key short-term support has been defined at $1760.4, the Oct 18 low.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok