Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SWITZERLAND DATA

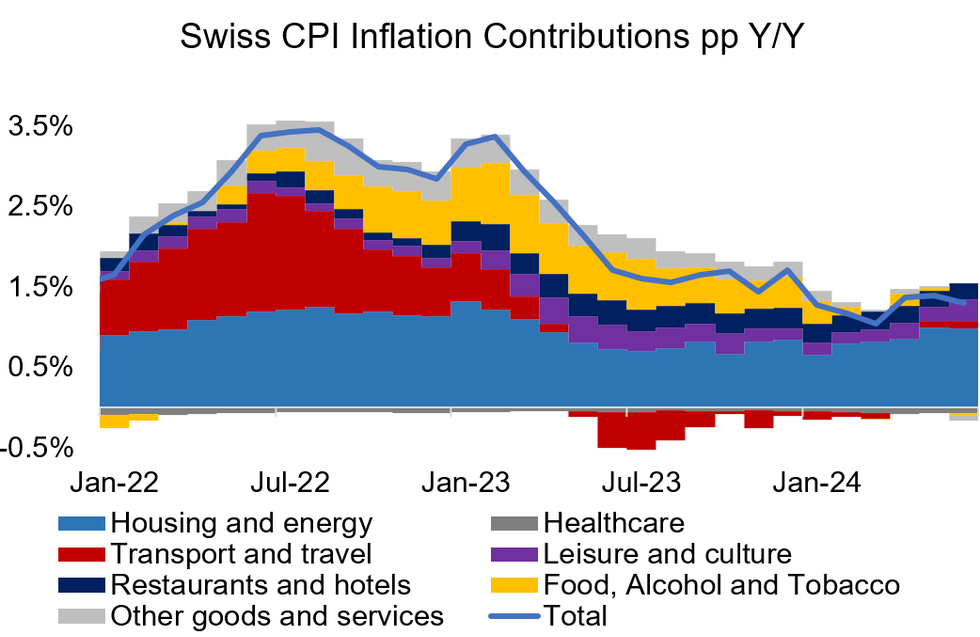

Swiss June CPI inflation came in slightly softer than expected and 0.1pp lower than in May at +1.3% Y/Y (1.4% cons and prior). On a sequential comparison, CPI remained flat at 0.0% M/M (+0.1% cons; +0.3% prior). Core inflation meanwhile also printed below expectations, at 1.2% Y/Y (1.3% cons; 1.2% May).

- For the Y/Y headline rate, this marks the first decline since three months.

- Overall, domestic second-round effects overall do not seem to have seen a broad-based decline on first sight regardless of the headline decline.

- On first sight, contributions of individual categories to the Y/Y headline rate were a bit mixed (although overall lower leading to the headline decline): We see significantly lower contributions from food / non-alcoholic beverages (-0.07pp change for a -0.04pp contr in June) and household products (-0.05pp chg to a -0.09pp June contr).

- Meanwhile, the contribution of the recreation category appears to have jumped (+0.09pp to 0.27pp).

MNI, SECO

MNI, SECO

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok