Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: Fed VC Clarida on Taper Talk Weighs on Short End

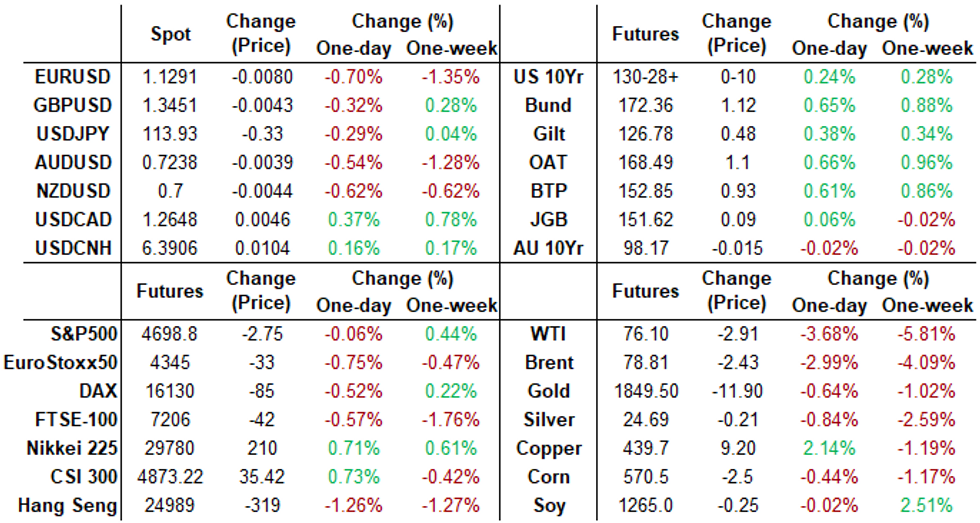

Shorter-dated Tsys have almost fully unwound today's earlier rally after relatively more hawkish commentary from both Fed Waller then VC Clarida on potential for Fed accelerating taper.- Long-end held onto a sizeable rally though, with 10Y yields down -5bps at 1.536% and the 30Y down -6.1bps at 1.907%, driven by European lockdown fears and at weekly lows. Combination has seen a 5bp bull flattening in 2s/10s on the day to 103.7bps, the lowest this week and getting towards the low end of the monthly range.

- Earlier, BBB passed in the House now moves to the Senate.

- Heavy overall volumes (TYZ1 >1.9M) tied to surge in Dec/Mar futures rolling (first notice on Nov 30); large selling Eurodollar Whites-Reds EDZ1-EDU3) following Fed VC Clarida comments re: taper debate in Dec.

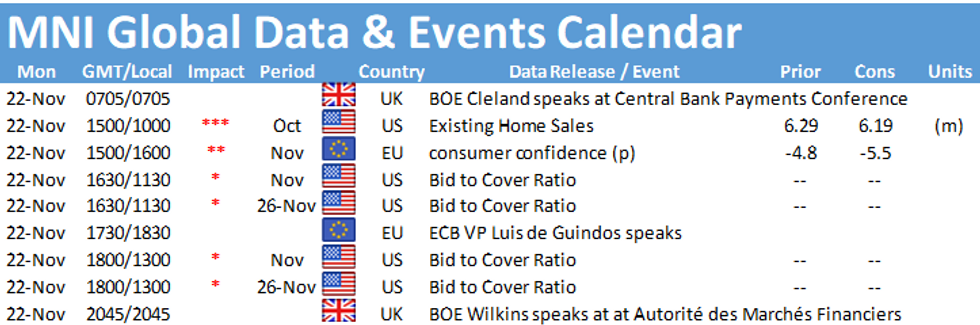

- Ahead: Fed minutes on Wed amidst heavy data week including the Nov PMI,PCE/incomes for Oct and the second Q3 GDP print before Thanksgiving on Thursday. Next wk's Tsy auction schedule is front-end focused ahead of Thanksgiving, with 2s, 5s and 7s on offer. Markets see full day Wed, closed Thu and early close Fri.

- The 2-Yr yield is down 0.4bps at 0.4986%, 5-Yr is down 1.8bps at 1.2018%, 10-Yr is down 5bps at 1.536%, and 30-Yr is down 6.3bps at 1.9059%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N +0.00175 at 0.07600% (+0.00125/wk)

- 1 Month +0.00225 to 0.09338% (+0.00425/wk)

- 3 Month +0.00437 to 0.16400% (+0.01125/wk) ** Record Low 0.11413% on 9/12/21

- 6 Month +0.00588 to 0.22938% (+0.00325/wk)

- 1 Year +0.00200 to 0.39175% (-0.00675/wk)

- Daily Effective Fed Funds Rate: 0.08% volume: $77B

- Daily Overnight Bank Funding Rate: 0.07% volume: $273B

- Secured Overnight Financing Rate (SOFR): 0.05%, $898B

- Broad General Collateral Rate (BGCR): 0.05%, $358B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $337B

- (rate, volume levels reflect prior session)

- Tsy 1Y-7.5Y, $1.751B accepted vs. $6.036B submission

- Next scheduled purchases

- Mon 11/22 1010-1030ET: Tsy 10Y-22.5Y, appr $1.425B

- Tue 11/23 1010-1030ET: TIPS 7.5Y-30Y, appr $1.075B

- Operational purchases paused until Nov 29

FED Reverse Repo Operation

NY Federal Reserve

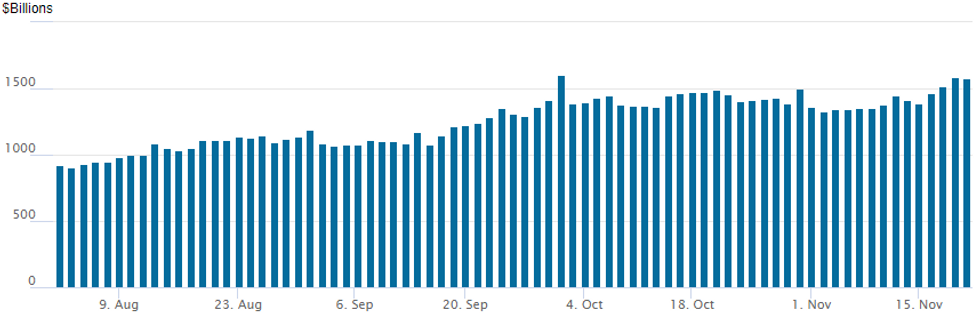

NY Fed reverse repo usage recedes to $1,575.384B from 74 counterparties vs. $1,584.097B on Thursday (Nov high and second highest on record). Closing in on record high of 1,604.881B from Thursday, September 30.

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- 30,000 Jun 99.18/99.37/99.50 put fly, 0.5

- -10,000 Red Dec 98.75/99.00 put spds, 7.5

- +5,000 Mar 99.37/99.62/99.75 put flys, 1.0

- 2,500 Blue Mar 97.62/97.87 put spds, 4.0 vs. 9828/0.10%

- -10,000 Green Dec 98.62/99.00 2x1 put spds, 15.5-15.0

- +10,000 short Dec 99.18/99.31 call spds

- Overnight trade

- 2,500 Blue Dec 97.75/98.00 2x1 put spds

- Block -8,000 short Dec 98.87/99.0 put spds vs.

- Block +8,052 Blue Dec 98.00/98.25 put spds, 4.0 net

- 3,250 Blue Dec 98.00/98.62 call spds

- 2,500 Green Dec 98.50/98.75 call spds

- +7,000 Green Jan 97.75/98.00 put spds, 2.5

- 5,900 USZ 166 calls, 1

- Update, +26,000 TYZ 129.5/130 put spds, 2.0 -- adds to 20k overnight

- 4,150 TYZ 130/130.25/130.5/130.75 put condors, 2/wings over

- Overnight trade

- +20,000 TYZ 129.5/130 put spds, 2.0

- 13,500 TYZ 132.25 calls, 1

- 8,500 TYF 131 calls, 22

- +5,000 TYZ 131.5 calls, 3

- 2,500 TYF 127.5/128.5/129.5 put flys, 10

- Block, -10,000 TYZ 129.75 puts, 5

FOREX: Volatile Session Results In Euro Weakness Amid Fresh Lockdown Concerns

- A fresh wave of euro weakness to kick off the US trading session on Friday saw EURUSD make fresh weekly lows, printing 1.1250.

- Renewed virus concerns in Europe benefitted safe haven FX and as such, EURJPY came under significant pressure, trading below 1.28 for the first time in 2 months, just shy of the August/September lows residing at 1.2793/4. In unison, EURCHF extended below the 1.0505 break level down to 1.0448 at its worst point.

- Despite the significant weakness, the Euro did find some support and volatile price action sparked a strong recovery off the early NY session lows. Two main reasons behind the bounce were some slightly more firm remarks from Weidmann on inflationary persistence as well as the German Foreign Minister excluding any national lockdowns.

- EURUSD rose back above 1.13 while EURJPY completed a +100 pip recovery above the 129 handle before both pairs settled a little lower into the close.

- With bouts of equity weakness and heavy energy prices, the dollar was a beneficiary overall on Friday, with the dollar index gaining 0.5%. This erases the majority of Wed/Thu losses and keeps the greenback in strong positive territory for the week.

- Given the strong performance of haven FX, AUD and NZD naturally gravitated around 0.6% lower throughout the day.

- A light data calendar to kickstart next week, before European Flash PMI data headlines Tuesday's docket.

FX: Expiries for Nov22 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1350(E774mln), $1.1380-90(E677mln), $1.1450(E1.5bln), $1.1580(E1.3bln)

- GBP/USD: $1.3360-70(Gbp811mln)

- EUR/GBP: Gbp0.8360(E507mln)

- AUD/USD: $0.7400-15(A$604mln)

- USD/CAD: C$1.2485-95($1.0bln), C$1.2685($1.1bln)

EQUITIES: NASDAQ Charges to New Highs, Shrugging Off Europe's Lockdown Woes

- Friday proved a choppy session, with equity futures across Wall Street and Europe slipping sharply on news that Austria was to become the first Western nation to re-enter pandemic-era lockdowns for both the vaccinated and non-vaccinated populations. Fears that Germany could soon follow were swiftly refuted, as the German foreign minister ruled out a 'general' lockdown, but indicated that options remain for restrictions on those without immunization.

- As Germany ruled out a broad lockdown, sentiment recovered somewhat, allowing futures to recover off bottom and help buoy the NASDAQ to new record highs. Underpinning the tech outperformance, semiconductors traded firmly, with strong earnings this week and a statement from South Korean and US authorities easing concerns over tight supply chains.

COMMODITIES: Energy Prices Down On Lockdown Fears

- Brent and WTI crude futures were weighed down by lockdown fears, falling -3-3.5% as Austria re-instated pandemic measures for both vaccinated and unvaccinated populations alike.

- News later in the day that Germany wasn't planning a "general" lockdown helped prices stabilise but no material bounce was forthcoming. Prices continued to trade heavy, with White House spokesperson Psaki reiterated that the US has been in touch with a number of countries about oil prices.

- Brent retains a bearish near-term outlook, having broken the short-term support of $80.20 (Nov 4 low) and is closing in on the first support level of $78.42 (Oct 7 low).

- Similar story in WTI, which at $76.24 is through $77.23 (Nov 4 low) and is approaching the first support level of $75.02.

- Separately, gold has dipped -0.6% in recent trade to $1848.45 in a partial retracement after a clear break of resistance at $1834 last week (Sep 3 high).

- Key event risk next week include Biden's long-awaited decision on Fed chair at some point, preliminary global PMI data on Tue and the Fed minutes on Wed before Thanksgiving in the US on Thu.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok