Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: Omicron? There's a Vacc For That

Early whipsaw action Wednesday -- Tsys and Bunds reversed late overnight bid (tied to reports suggested that the UK Govt will announce stricter Covid restrictions in face of Omicron variant) promptly sold off on headlines that a third dose Pfizer, Biontech vaccine "neutralized" Omicron variant in lab tests.- Not quite the risk-on move some had hoped for: equities sat this one out, trading only modestly higher late in the day (EDZ1 +10.5 at 4695.5), Gold gained 2.0 and WTI crude held around 72.40.

- Early trade, trading desks reported domestic real$ buying 2-3s, leveraged accts buying 5s after chunky 5Y futures block sales (-16.9k) and sell-stops triggered on first and second downdrafts.

- Yield curves bear steepened/bonds extending session lows after huge JOLTS openings rate of 11.033M -- near record high, quits rate 2.8%. Equities holding near steady (ESZ1 4685.0 last). Trading desks report domestic and foreign real$ selling 10s and 30s. Central bank bought 2s, contributing to bear steepener.

- Tsy had firmed off session lows in lead-up to the Tsy auction, drew modest two-way after $36B 10Y note re-open (91282CDJ7) tailed slightly:1.518% high yield vs. 1.515% WI; 2.43x bid-to-cover better than last month's 2.35x but still shy a 2.51x 5-month average.

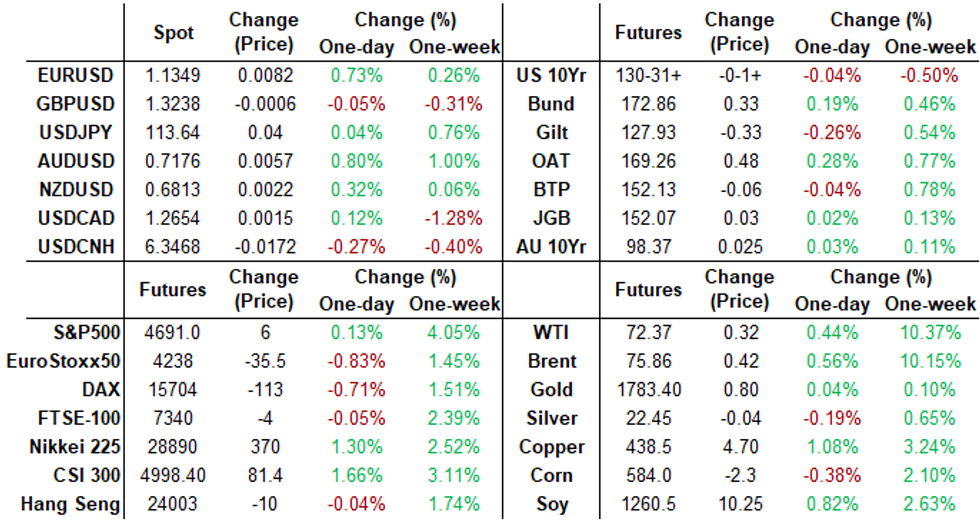

- The 2-Yr yield is down 1.6bps at 0.6735%, 5-Yr is down 0.2bps at 1.2532%, 10-Yr is up 2.9bps at 1.5024%, and 30-Yr is up 6.9bps at 1.8716%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N -0.00550 at 0.07025% (-0.00625/wk)

- 1 Month -0.00063 to 0.10138% (-0.00275/wk)

- 3 Month +0.00225 to 0.20050% (+0.01287/wk) ** Record Low 0.11413% on 9/12/21

- 6 Month +0.00475 to 0.28813% (+0.01700/wk)

- 1 Year +0.00625 to 0.48875% (+0.02725/wk)

- Daily Effective Fed Funds Rate: 0.08% volume: $74B

- Daily Overnight Bank Funding Rate: 0.07% volume: $257B

- Secured Overnight Financing Rate (SOFR): 0.05%, $989B

- Broad General Collateral Rate (BGCR): 0.05%, $349B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $338B

- (rate, volume levels reflect prior session)

- Tsy 2.25Y-4.5Y, $7.351B accepted vs. $19.865B submission

- Next scheduled purchases -- two for Thursday:

- Thu 12/09 1010-1030ET: Tsy 0Y-2.25Y, appr $10.875B

- Thu 12/09 1100-1120ET: Tsy 10Y-22.5Y, appr $1.425B

- Fri 12/10 1010-1030ET: Tsy 7Y-10Y, appr $2.825B

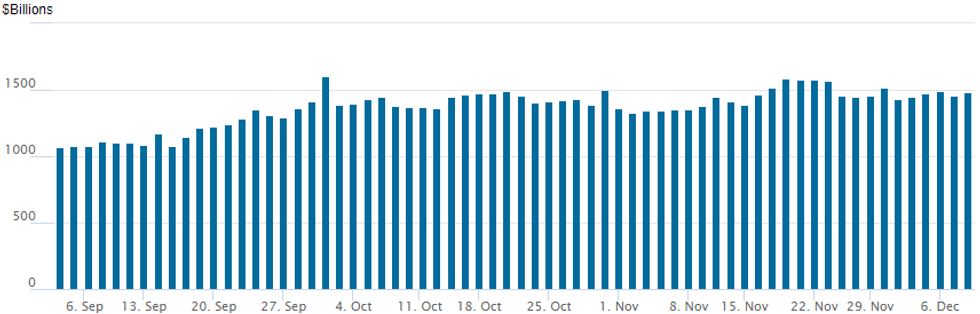

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage rebounds to $1,484.192B from 71 counterparties vs. $1,455.038B on Monday. Record high remains at 1,604.881B from Thursday, September 30.

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- +20,000 Blue Mar 97.87/98.12 put spds, 8.5 vs. 98.215/0.16%

- +5,000 Red Dec'22 98.62/98.87 put spds 5.5 over 99.50/99.62 call spds vs. 98.97/0.20%

- +2,000 Green Jun 99.37/99.50 call spds, 0.5

- 3,000 Green Sep 97.25/97.37 put spds

- +20,000 short Jun 97.75/98.25 put spds, 11.5

- +5,000 Blue Jun 97.75/98.00 put spds, 7.5

- +5,000 Apr 99.12 puts, 4.25

- Update, +15,000 Mar 99.25/99.43/99.50/99.62 put condors, 2.5

- -4,000 Jun 99.00 puts, 4.5

- Overnight trade

- 10,000 Blue Dec 98.25 puts

- 3,500 short Jan 98.43/98.56 put spds

- 6,000 short Dec 98.87 puts

- 1,500 short Dec 98.81/98.93 2x1 put spds

- -5,000 TYH 128/133 strangles, 44

- -7,500 TYG 128.5/132 strangles, 34-35

- Update, -18,100 FVG 121 calls, 16

- +7,000 TYG 125.5/128/129/130 put condors 1 over TYG 132/133.5 call spds on screen

- Overnight trade

- 20,000 TYF 128.5 puts, 3

- 10,000 TYF 128/128.5 put spds, 2

EGBs-GILTS CASH CLOSE: Gilts Outperform On "Plan B"

Gilts easily underperformed Bunds Wednesday, with periphery spreads also widening.

- UK yields had fallen sharply by late morning following reports that the gov't would move to "Plan B" Covid restrictions, but the move fully reversed and then some after a promising Omicron efficacy report just before midday from vaccine-makers Pfizer/Biontech.

- The latter saw 10Y Bund yields rise nearly 10bp from the low over the afternoon.

- No particular trigger for BTP weakness, but some big cash selling noted in the morning set off spread-widening (and equities weakened over the session, so modestly risk-off).

- ECB's Schnabel noted the bank would not hike before ending net asset purchases (contrasting w Holzmann's comments earlier in the week).

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 2.5bps at -0.676%, 5-Yr is up 4.6bps at -0.555%, 10-Yr is up 6.2bps at -0.313%, and 30-Yr is up 7.7bps at -0.016%.

- UK: The 2-Yr yield is unchanged at 0.462%, 5-Yr is up 1bps at 0.582%, 10-Yr is up 4.5bps at 0.775%, and 30-Yr is up 3.4bps at 0.837%.

- Italian BTP spread up 4.3bps at 133.9bps / Greek up 6bps at 169.6bps

EGB Options: German Put Spreads And Vol Trades

Wednesday's Europe rates / bond options flow included:

- RXF2 173.5/172.0 1x2 put spds, 12.5 paid in 2k

- DUG2 112.0/112.3 strangle, 10.5-12.0 paid in 4.5k

- DUG2 112.00/111.90ps, bought for 2 in 2k

FOREX: Greenback Under Pressure As Aussie Extends Gains

- The dollar index fell 0.45% on Wednesday, turning negative on the week, largely resulting from strong performances in CNH, AUD and the Euro.

- Commodity and risk-tied currencies remain optimistic, evident by the near 1% rallies in both AUDJPY and EURJPY.

- With the greenback weakness, AUDUSD has further distanced itself from major noted support below the 0.7000 mark and is now closing in on the 20-day EMA, at 0.7187. A clear breach of this average would strengthen the current bull phase.

- EURUSD has bounced well from the day’s low at 1.1267 and is now trading towards the upper bound of last week’s range. Key short-term resistance is unchanged at 1.1383, Nov 30 high where a break would signal scope for a stronger corrective bounce and open 1.1514, Nov 5 high.

- USDCAD had trended lower ahead of the Bank of Canada rate announcement, however, a marginally dovish-to-expectations statement prompted a 50-pip bounce for the pair, in the face of dollar weakness.

- GBP came under pressure following reports that the Government are set to announce further covid restrictions. ‘Plan B’ is widely expected to have a working from home which spooked GBPUSD to fresh 2021 lows below 1.3200 to a low print of 1.3163. The pair has since bounced amid a weaker dollar, however, remains lower on the day with EURGBP up 0.77%.

- EURGBP’s recent breach of 0.8544, 76.4% of the Nov 5 - 22 sell-off has prompted an extension towards a key short-term resistance at 0.8595, the Nov 5 high.

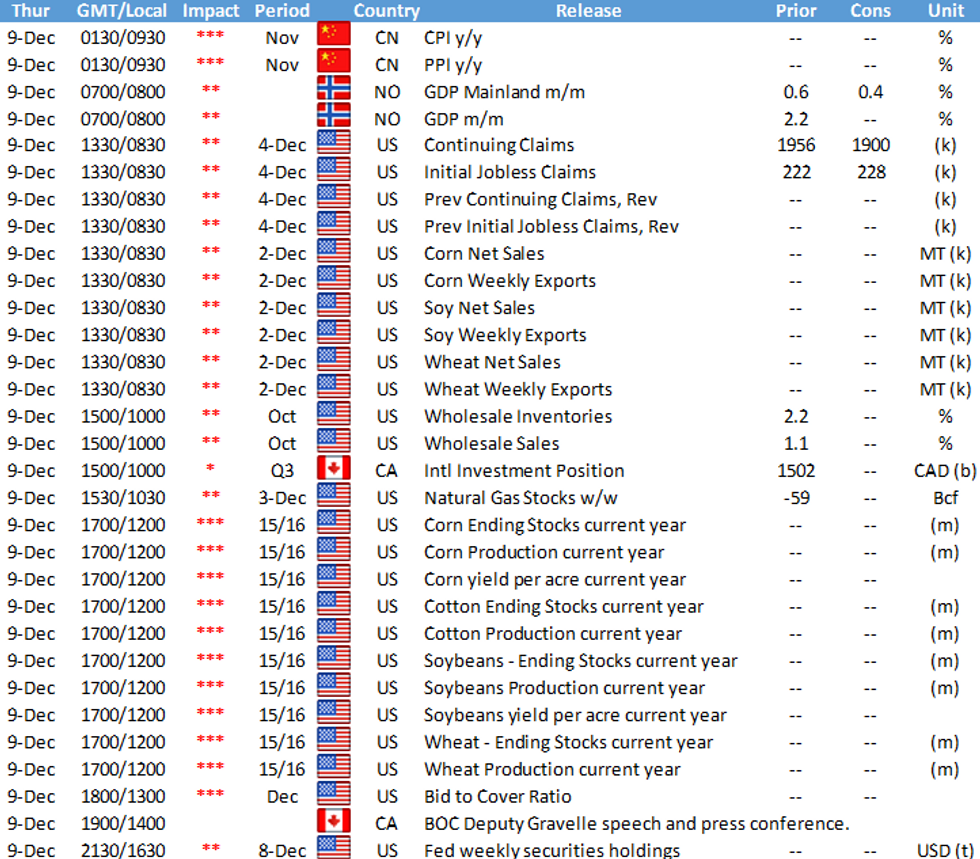

- Chinese CPI/PPI scheduled overnight, before a light European and US calendar ahead of Friday’s US CPI data. BOC’s Gravelle is due to speak about the Economic Progress Report with a Q&A expected.

FX: Expiries for Dec09 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1380-00(E978mln), $1.1425(E534mln), $1.1560-70(E1.1bln)

- USD/JPY: Y113.00-25($1.6bln), Y114.00-20($2.4bln)

- EUR/GBP: Gbp0.8550-60(E694mln)

- AUD/USD: $0.7250-60(A$567mln)

- USD/CNY: Cny6.34($2.3bln), Cny6.43($1.1bln); Cny6.3500($1.8bln)

EQUITIES: Markets Fade Off Vaccine-Induced Highs

- Equity markets faded off their highs into the Wednesday close, with the cash S&P500 dipping just below unchanged following the London close. Stock futures enjoyed an initial boost from a Pfizer/BioNTech press release which talked up the likelihood of a three jab regime protecting effectively against the new omicron variant. Sentiment faded from there, with weight in consumer staples and financials dragging headline indices across the US morning.

- Bearish pressure in the S&P E-minis has eased significantly this week and the contract rallied sharply higher Tuesday. Futures are once again back above the 50-day EMA, at 4569.94 today. This average highlights a pivot level and a stronger recovery through it would improve conditions for bulls. The focus is on 4717.00 next, the Nov 26 high ahead of the all-time high of 4740.50. Key support and the bear trigger is at 4492.00, the Dec 3 low.

COMMODITIES: Oil Sees Further Support From Vaccine Efficacy

- Oil futures are up a little over 1% today, supported by various positive headlines from Pfizer relating to three vaccine effectiveness against Omicron. This is a relatively modest move after sizeable rises over the past two days.

- US DOE inventories were mixed, with crude inventories seeing a smaller draw than forecast at -241k barrels but sizeable builds in both gasoline and distillates.

- WTI is +1.3% at $72.98, very close to the 20-day EMA of $73.07 whilst initial firm support lies at $65.60 (Dec 3 low). Latest price gains have been predominantly in shorter-dated contracts.

- Brent is +1.1% at $76.28, at the first resistance level of $76.27 (Dec 7 high) whilst first support is tighter at $73.20 (Dec 7 low).

- Gold meanwhile is flat at $1784.4. Short-term conditions remain bearish after breaching both the 20- and 50-day EMAs with attention on the base of a bull channel at $1763.8, drawn off the Aug 9 low.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok