Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US Tsys: Covid Surge Underpins Short End, Stocks Under Pressure

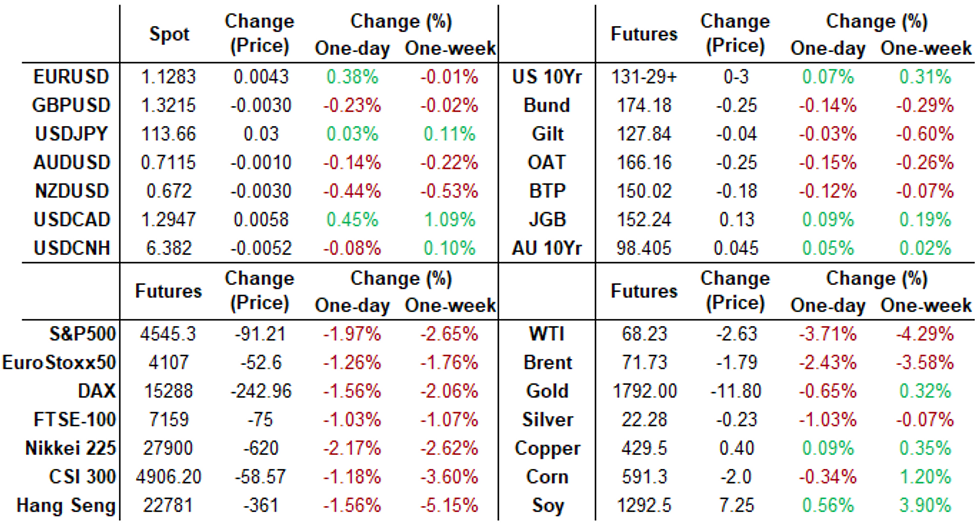

Tsys trading mostly weaker on moderate volumes after Monday's close, well off Asia/London crossover highs. Tsy 2s-5s outperformed while 10s-30s see-sawed to weaker levels/session lows by the close. Main drivers on day: concerns over measures to contain covid surge, and knock-on effect of Sen Manchin torpedoing Pres Biden's $2T BBB spending plan.

- Trading desks reported better real$ selling of long end Tsys during Asia hours, two-way with misc sellers in the belly on surprisingly robust volumes ahead the holiday. Volume surged around the Asia/London crossover included steepener Block package: 5s and 10s vs 30s at 0212:42ET.

- Bonds extended session lows (30YY 1.8545% high), equities holding weaker (ESH2 -65.0 at 4545.0 late vs. 4520.75 low), decoupling again after brief period negative correlation late last week. 5s30s back to Nov 30 levels, tapped 70.24.

- Trading desks reporting two-way flow in short end with leveraged fund buying vs. foreign real$ selling 2s, leveraged$ selling 5s, real$ selling 20s ($20B 20Y Bond sale Tuesday, 912810TC2). Sporadic flattener unwinds 2s10s, 5s and 10s vs. 30s.

- The 2-Yr yield is down 1.2bps at 0.6256%, 5-Yr is down 1.6bps at 1.1586%, 10-Yr is up 1.2bps at 1.414%, and 30-Yr is up 3.7bps at 1.8436%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N -0.00175 at 0.07250% (+0.00200 total last wk)

- 1 Month +0.00100 to 0.10350% (-0.00612 total last wk)

- 3 Month +0.00162 to 0.21425% (+0.01438 total last wk) ** Record Low 0.11413% on 9/12/21

- 6 Month +0.00388 to 0.31663% (+0.02450 total last wk)

- 1 Year +0.00225 to 0.53188% (+0.02025 total last wk)

- Daily Effective Fed Funds Rate: 0.08% volume: $71B

- Daily Overnight Bank Funding Rate: 0.07% volume: $257B

- Secured Overnight Financing Rate (SOFR): 0.05%, $910B

- Broad General Collateral Rate (BGCR): 0.05%, $338B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $326B

- (rate, volume levels reflect prior session)

- Tsy 4.5Y-7Y, appr $4.501B accepted vs. $11.752B submission

- Next scheduled purchases

- Tue 12/21 1010-1030ET: TIPS 7.5Y-30Y, appr $0.925B vs. $1.075B prior

- Wed 12/22 1010-1030ET: Tsy 10Y-22.5Y, appr $1.625B

- NY Fed buy-operations pause for holidays, resume Jan 3

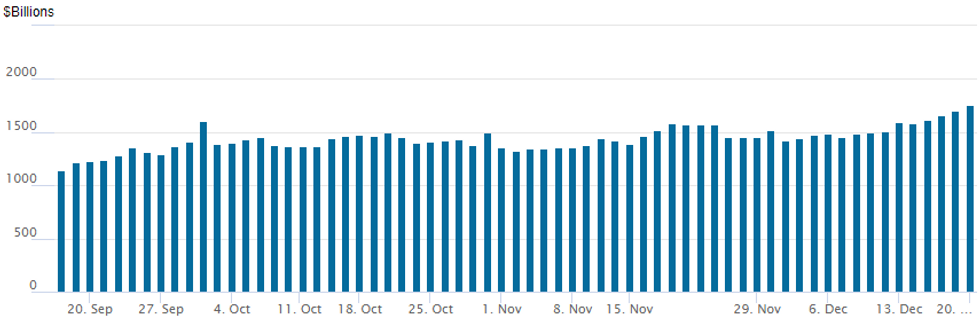

FED Reverse Repo Operation, Fourth Consecutive New High

NY Federal Reserve/MNI

NY Fed reverse repo usage climbs to fourth consecutive all-time high of $1,758.041B from 81 counterparties vs. Friday's $1,704.586B.

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- 11,300 Jun 99.18/99.25/99.31/99.37 put condors

- +5,000 short Mar 98.75/99.00/99.50 broken call flys, 1.75 on legs

- +60,000 short Mar 98.50/98.62 put spds 3.5 vs. 98.835/0.10%

- -5,000 Jun/Sep 99.75/99.87 1x2 call spd strip, 0.5 total

- +5,000 short Jan 99.00 calls, 3.5

- -1,500 Dec 99.00 straddles, 51.0

- +2,000 Green Mar 98.12/98.50 put spds vs. short Mar 98.62 puts, 4.25 net db/steepener

- Overnight trade

- 3,200 Sep 99.00 puts

- 1,000 USF 160/160.5 put spds, 3

- 6,600 TYG 128.5 puts, 4

- 8,000 TYH 128.5/129.5/131/131.5 broken put condors, 3 net/wings over

- Overnight trade

- 3,100 FVG 122.5 calls, 8

EGBs-GILTS CASH CLOSE: Drop In Yields Reverses Course

After dropping Monday morning on risk-off headlines and a sharp move lower in equities, Bund and Gilt yields bounced back in the afternoon.

- The risk-off tone was set overnight with sharp weakness in Asian stocks on resurgent Omicron concerns and news that US Pres Biden's expansive fiscal plans had been derailed.

- The flattening curve moves on the open later reversed as European equities came off lows, though Germany's moved decisively steeper by the cash close and the UK's remained flatter. Volumes were notably weak.

- Several headlines of note though none moved the market: Germany's Nagel nominated to head Bundesbank; UK not (yet) introducing tougher measures to combat Omicron; Italy released 2022 funding plans.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 1bps at -0.73%, 5-Yr is down 0.6bps at -0.613%, 10-Yr is up 1.1bps at -0.367%, and 30-Yr is up 2.9bps at -0.008%.

- UK: The 2-Yr yield is up 3.3bps at 0.542%, 5-Yr is up 2.6bps at 0.64%, 10-Yr is up 1.3bps at 0.772%, and 30-Yr is up 2bps at 0.952%.

- Italian BTP spread up 2.3bps at 129.6bps / Portugal down 0.1bps at 63.3bps

EGB Options: German Downside...Mostly

Monday's Europe rates / bond options flow included:

- OEG2 134.25/133.75 put spread vs 134.75 call (+ps, -c) in 2k, net received1.5 (-48% delta)

- RXG2 172/170 put spread bought for 18 in 1.4k (-11% delta)

- RXH2 172/171 put spread bought for 23 in 5.7k

- RXF2 173/172 put spread bought for 2 in 5k (expiry this Thursday)

- 2RJ2 100.00/99.75 put spread bought for 6.75 in 10k

FOREX: EUR Crosses Benefit From Risk-Off Tone, TRY Spikes

- Senator Manchin's one-handed tanking of Biden's Build Back Better bill combined with fresh Omicron-related restriction fears guided risk lower to start the week.

- The pressure on both equity and commodity markets weighed on the likes of NZD and CAD, both around 0.45% lower against the greenback.

- A mixed performance for the US dollar and a broadly unchanged dollar index was largely down to a higher Euro with EURUSD slowly eroding Friday’s retreat and briefly retaining the 1.13 handle. Naturally there was very supportive price in Euro crosses, with EURNZD and EURCAD rising close to 1%.

- In emerging markets, USDTRY is currently just above the 13.00 mark after a stunning 34% intra-day reversal from highs of 18.36 to lows around 12.27. Comments from President Erdogan sparked some renewed optimism for the Lira, with understandably poor liquidity exacerbating the price action.

- The government announced measures including the introduction of a new program that will protect savings from fluctuations in the local currency. The government will make up for losses incurred by holders of lira deposits should the lira’s declines against hard currencies exceed interest rates promised by banks. The pair reversed the entirety of the December rally.

- Despite the lack of event risk in the immediate pipeline with the holidays approaching, overnight markets will see the latest RBA minutes and Canadian retail sales will be the highlight of the North American data docket.

FX: Expiries for Dec21 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1150(E532mln), $1.1200-20(E676mln), $1.1250-70(E889mln), $1.1275-95(E780mln), $1.1315(E527mln), $1.1350(E742mln), $1.1500(E864mln)

- USD/JPY: Y112.70($562mln)

- USD/CAD: C$1.2800-10($524mln)

- USD/CNY: Cny6.40($650mln)

EQUITIES: Stocks Spiral, NASDAQ Shows Below Key Support

- Wall Street traded lower Monday, echoing the trend seen throughout the European session, as omicron concerns and a clouded US fiscal outlook dented sentiment.

- The NASDAQ was hit particularly hard by the sell-off, with the Composite fading as much as 2% on the day. The H2 future traded through the 100-dma support at 15529, marking the first time below that level since early October.

- Materials and energy remain poorest performers, but again automakers are suffering, with Tesla, Ford and General Motors all off around 3% apiece.

- Meanwhile, COVID names including Clorox and Pfizer are rallying hard, topping the S&P 500 and indicating that omicron, as well as Manchin nixing the BBB, is behind today's price action.

- European markets traded with similar losses, as the German DAX dropped 1.9% and the EuroStoxx50 by 1.3%. The FTSE-100 fared slightly better, but still edged lower by 1.0% into the close.

COMMODITIES: Oil Tumbles On Omicron And BBB Double Act

- Oil futures have tumbled on fears of stricter Omicron-related restrictions and Manchin’s blocking of BBB, far outweighing a shutdown in production at Libya’s largest oil field.

- WTI is -5.1% at $67.2, having briefly cleared the first support level of $66.62 (Dec 6 low) before retracing. Further support is seen at $65.45 (Dec 3 low) whilst initial resistance is the intraday high of $69.98.

- Declines are somewhat front-loaded over near-term contracts but nevertheless still significant further out.

- $55/bbl puts have been the most active strikes today for the G2 (Feb'22) contract, followed by $60/bbl puts and then closely $75/bbl calls.

- Brent is -4.4% at $70.28, with first support at $69.24 (Dec 3 low) and plenty of room to run to the upside with initial resistance at $75.01, the 20-day EMA.

- Gold has dipped -0.2% against this backdrop to $1794.8, eyeing up $1770.5, the base of the bull channel drawn from the Aug 9 low.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.