Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: Risk-Rally In Your Stocking

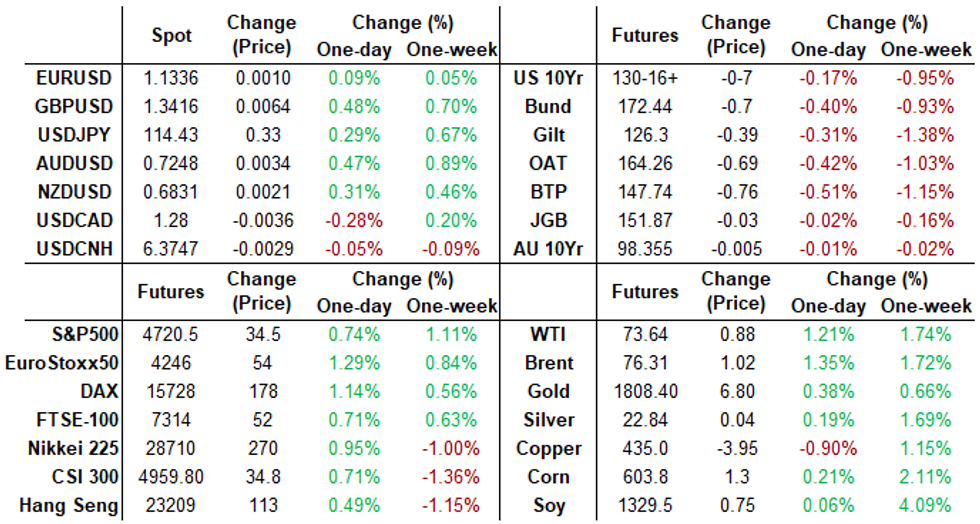

Rates trading weaker after Thursday's early close (Friday markets closed for Christmas Eve) on very light volumes: TYH2 just over 466k.- Tsy futures near bottom of the session range after selling off on another positive showing for equities (ESH2 +33.0 to 4719.0, 4724.25H vs. 4738.5 all-time high on Dec 16).

- Tsy futures pared modest losses briefly post-data (in-line wkly claims, continuing claims beat, durables beat but core cap goods weak). Rates reversed gains after stocks opened and held near lows since midmorning (30YY 1.9122%H; 10YY 1.4995%H).

- U. of Mich. Sentiment in-line with estimate (70.4), existing home sales weaker than estimated: +12.4% TO 0.744M SAAR (.770M est) did spur some light buying in 10s-30s.

- Upbeat Covid headlines similar to Wednesday: OMICRON HOSPITAL RISK 50-70% LOWER THAN DELTA, U.K. SAYS ... MERCK COVID PILL AUTHORIZED FOR EMERGENCY USE IN THE U.S, Bbg

- No new high-grade issuance, Dec running total stands at $62.2B. NY Fed buy-operations pause for holidays, resume Jan 3 with Tsy 2.25Y-4.5Y, appr $6.325B vs. $7.375B prior.

- The 2-Yr yield is up 2.6bps at 0.6861%, 5-Yr is up 2.5bps at 1.2401%, 10-Yr is up 4bps at 1.491%, and 30-Yr is up 5.6bps at 1.9052%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N +0.00463 at 0.07513% (+0.00088/wk)

- 1 Month -0.00088 to 0.10188% (-0.00062/wk)

- 3 Month +0.00837 to 0.21975% (+0.00713/wk) ** Record Low 0.11413% on 9/12/21

- 6 Month +0.01000 to 0.33638% (+0.02363/wk)

- 1 Year +0.00775 to 0.56113% (+0.03150/wk)

- Daily Effective Fed Funds Rate: 0.08% volume: $69B

- Daily Overnight Bank Funding Rate: 0.07% volume: $234B

- Secured Overnight Financing Rate (SOFR): 0.04%, $893B

- Broad General Collateral Rate (BGCR): 0.05%, $347B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $331B

- (rate, volume levels reflect prior session)

- NY Fed buy-operations pause for holidays, resume Jan 3:

- Mon 01/03 1010-1030ET: Tsy 2.25Y-4.5Y, appr $6.325B vs. $7.375B prior

- Tue 01/04 1100-1120ET: TIPS 1Y-7.5Y, appr $1.525B

- Wed 01/05 1010-1030ET: Tsy 7Y-10Y, appr $2.425B vs. $2.825B prior

- Wed 01/05 1100-1120ET: Tsy 22.5Y-30Y, appr $1.825B

- Thu 01/06 1100-1120ET: TIPS 7.5Y-30Y, appr $0.925B

- Fri 01/07 1010-1030ET: Tsy 0Y-2.25Y, appr $9.325B

FED Reverse Repo Operation

NY Fed reverse repo usage recedes to $1,699.277B from 82 counterparties vs. $1,699.277B Wednesday. New record high this week of $1,758.041B posted Monday, December 20.

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- 5,000 Green Mar 97.75 puts, 2.0

- +2,000 Green Mar 98.25/98.37/98.50 call flys, 1.5, 98.375 ref

- -10,000 Mar 99.68 c/99.87 p guts, 29.25

- 18,000 Mar 100.00 calls, cab

- 1,000 Jun 99.06/99.31/99.56 iron flys

EGBs-GILTS CASH CLOSE: Bunds Underperform Going Into Holiday

The German curve bear steepened Thursday, with Bunds underperforming Gilts.

- Gilts had underperformed in the morning, with the UK gov't reportedly avoiding lockdown restrictions ahead of Christmas.

- But Bunds moved lower (and BTP spreads widened to the most since Q3 2020 though recovered), with RX futures dipping through support. The absence of ECB purchases (the last ones of the year were made Tuesday) was cited by some desks as playing a factor, as was the covering of long positions amid thin liquidity ahead of a prolonged market holiday.

- Most European bond and equity markets are closed Friday (as is the U.S.) in observance of the Christmas holiday. Gilts/FTSE are the main exception, though with a shortened session.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.4bps at -0.678%, 5-Yr is up 3.1bps at -0.513%, 10-Yr is up 4.4bps at -0.249%, and 30-Yr is up 5.3bps at 0.117%.

- UK: The 2-Yr yield is up 2bps at 0.66%, 5-Yr is up 2.5bps at 0.772%, 10-Yr is up 3.6bps at 0.922%, and 30-Yr is up 2.6bps at 1.093%.

- Italian BTP spread up 1.9bps at 136.2bps / Spanish up 0.3bps at 75.6bps

EGB Options: Largely Downside

Thursday's Europe rates / bonds options flow included:

- DUG2 112.20c bought for 6.5 in 5k

- DUG2 112.10^ sold at 16.5 in 4k

- OEG2 133.75/134.25cs, bought for 19 and 19.5 in 2.5k

- OEG2 133.25/133ps bought in 1.5k vs selling 500 lots of the 134.25c, traded for flat

- 2RH2 10012/100ps, sold at 7 in ~1.5k

- ERH3 100.125/99.875 ps bought for 5 in 2k

- ERZ2 100.25/100.00ps bought for 4.5 in 2k (ref 100.35)

FOREX: US Dollar Index Remains At Lows Of Week As Risk Climbs

- Despite some initial strength in broad dollar indices, the greenback weakened back to unchanged and remains close to its worst levels of the week.

- With risk sentiment continuing to climb, evident by supportive price action in both equity and commodity markets, risk tied FX such as AUD, NZD and GBP all extended their rallies.

- In similar price action to the previous two sessions, the Japanese Yen remained weak and USDJPY consolidated gains above the 114 mark grinding up to 114.45, the best levels since November 26.

- Having breached 114.38, the 61.8% Fibonacci retracement of the Nov 24 - 30 downleg, this signals potential for a stronger technical rally.

- AUDJPY and GBPJPY were the strongest performing pairs, gaining close to 0.75%.

- In emerging markets the Turkish lira took another huge boost, firming roughly 17% against the dollar at its peak where USDTRY made lows of 10.25, an astonishing 44% from the week’s high print. The pair bounced back to around 11.25 but remains roughly 7% weaker for Thursday.

- Japanese National Core CPI overnight before an empty Christmas Eve docket with US markets closed for holiday.

EQUITIES

Key late session market levels:

- DJIA up 202.41 points (0.57%) at 35963.68

- S&P E-Mini Future up 34 points (0.73%) at 4720.5

- Nasdaq up 143.7 points (0.9%) at 15664.76

- EuroStoxx 50 up 48.8 points (1.16%) at 4265.86

- FTSE 100 up 31.68 points (0.43%) at 7373.34

- German DAX up 162.84 points (1.04%) at 15756.31

- French CAC 40 up 54.48 points (0.77%) at 7106.15

COMMODITIES: Oil Up Again On Easing Covid Fears, Gas Swings Continue

- Oil futures are up a little over 1% as improved risk-on sentiment as Omicron fears ease for the third day running.

- WTI is +1.2% at $73.7, with resistance next seen at $74.54, the 61.8% retracement of the Oct-Dec sell-off, whilst support is seen at $68.56 (Dec 21 low).

- Price increases have been broadly spread across 2022 contracts as opposed to yesterday’s front-loaded bias.

- Brent is +1.3% at $76.3 and through a couple resistance points including the 50-day EMA of $76.17. Next resistance at $76.70 (Dec 9 high).

- Gold is up +0.2% at $1807.8, moving closer to the near-term bull trigger at $1815.6 (Nov 26 high). Initial firm support is seen at $1773.1 base of the bull channel.

- US natural gas prices have swung heavily, currently down -4.4% on the day from a trough of -9.5%. They are back towards month lows and almost 20% below the Nov average, helping dampen US energy price inflation over the short-term.

- This is small compared to the more than 20% daily decline in European gas prices on incoming US LNG cargoes after a surge earlier in the week put European prices at a rare premium to Asia.

| Date | GMT/Local | Impact | Flag | Country | Event |

| 24/12/2021 | 1600/1100 | ** |  | US | St. Louis Fed Real GDP Nowcast |

| 24/12/2021 | 1600/1100 | ** | | US | NY Fed GDP Nowcast |

| 27/12/2021 | 1530/1030 | ** | | US | Dallas Fed manufacturing survey |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok