Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

Eurodollar/Treasury Futures/Options Roundup

Another volatile day for stocks Tue, similar to late Mon's sharp rebound to finish higher, shares staged a second half rally back near steady -- but pared more than half the bounce after the FI close.- Otherwise, Tsy trade was generally subdued trade ahead Wed's FOMC policy annc (no rate change anticipated yet, clearer forward guidance re: liftoff, balance sheet run-off, QT) Main focus on geopolitical risk and headlines re: Russia/Ukraine invasion threat, NATO, US troops on high alert.

- Limited react to data on day: US NOV FHFA HPI SA +1.1% V +1.1% OCT; +17.5% Y/Y; US CONF BOARD CONSUMER CONFIDENCE 113.8 IN JAN V DEC 115.2.

- Tsy futures holding near middle of weaker session range with mild short covering after $55B 5Y note auction (91282CDT5) stops through: 1.533% high yield vs. 1.547% WI; 2.50x bid-to-cover vs. December's 2.41x.

- Indirect take-up: climbs to 68.72% vs. Dec's 2021 year high of 65.66%. Primary dealer take-up: recedes 14.80% vs. 20.02%; Direct take-up 16.48% vs. 14.32%.

- Eurodollar option flow: Liftoff Positioning, 50Bp June hike in addition to 25bps liftoff from Fed in March. EDM2 currently trading 99.265: +5,000 Jun 98.93/99.00/99.06/99.12 put condors, 1.0 vs. 99.29/0.05%

- Elsewhere, targeting five 25bp quarterly hikes starting this March through March 2023, paper adding to bear curve (Whites/Greens) steepener: +15,000 short Mar 98.50/Green Mar 98.00 put spds, 0.25/Greens over

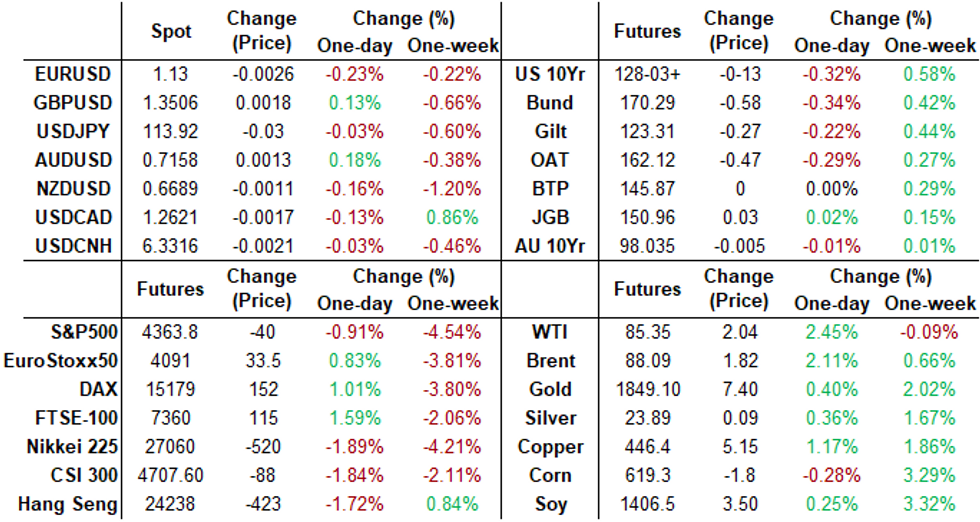

- The 2-Yr yield is up 6.2bps at 1.0333%, 5-Yr is up 2.2bps at 1.5691%, 10-Yr is up 1.1bps at 1.7814%, and 30-Yr is up 1.4bps at 2.1258%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N +0.00215 at 0.07886% (+0.00415/wk)

- 1 Month -0.00057 to 0.10786% (+0.00015/wk)

- 3 Month +0.00043 to 0.26757% (+0.00986/wk) ** Record Low 0.11413% on 9/12/21

- 6 Month +0.00172 to 0.45029% (+0.00586/wk)

- 1 Year -0.00371 to 0.78986% (-0.00871/wk)

- Daily Effective Fed Funds Rate: 0.08% volume: $75B

- Daily Overnight Bank Funding Rate: 0.07% volume: $273B

- Secured Overnight Financing Rate (SOFR): 0.04%, $886B

- Broad General Collateral Rate (BGCR): 0.05%, $332B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $322B

- (rate, volume levels reflect prior session)

- TIPS 1Y-7.5Y, $1.999B accepted vs. $2.829B submission

- Pause for FOMC policy annc on Jan 26

- Thu 01/27 1010-1030ET: Tsy 22.5Y-30Y, appr $1.825B steady

- Mon 01/31 1010-1030ET: Tsy 2.25Y-4.5Y, appr $8.425B vs. $6.325B prior

- Tue 02/01 1100-1120ET: TIPS 7.5Y-30Y, appr $1.225B vs. $0.925B prior

- Thu 02/03 1100-1120ET: Tsy 10Y-22.5Y, appr $1.625B steady

- Tue 02/08 1010-1030ET: Tsy 22.5Y-30Y, appr $1.825B steady

- Thu 02/10 1010-1030ET: Tsy 7Y-10Y, appr $3.225B vs. $2.425B prior

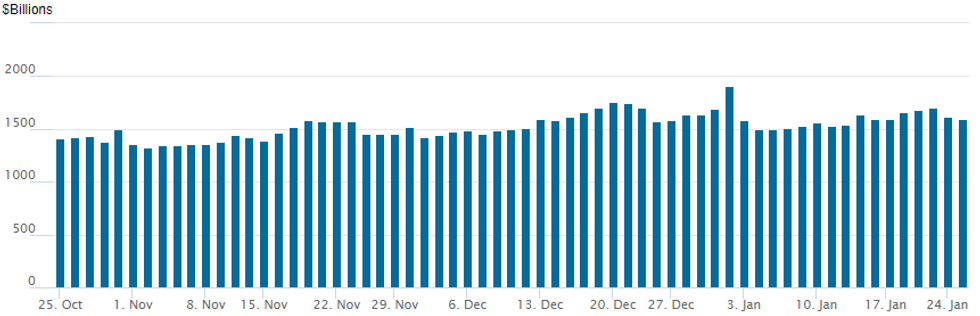

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage recedes to $1,599.502B w/81 counterparties vs. $1,614.002B prior session -- still well off all-time high of $1,904.582B on Friday, December 31.

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- +5,000 Jun 98.93/99.00/99.06/99.12 put condors, 1.0 vs. 99.29/0.05%

- Update, +15,000 short Mar 98.50/Green Mar 98.00 put spds, 0.25/Greens over

- +5,000 Apr 98.87/99.00 put spds 1.25 over Jun 98.93/99.06 put spd

- +8,000 short Jun 98.50/99.00 1x2 call spds, 10.0 vs. 98.425/0.14%

- 5,000 Mar 99.87 calls, .25

- -3,000 Green Feb 97.87/98.00 7x4 put spds, 5, 4-legs over

- -10,000 Red Sep 100.25 calls, 1.0

- Overnight trade

- Block, +15,000 short Sep 98.25/98.87 1x2 call spds, 14.5 vs. 98.255/0.10%

- 11,500 short Mar 98.50 puts, 9.5

- 4,000 short Mar 98.25/98.50 put spds

- 9,000 Jun 99.87 calls

- +5,000 TYH 127.5 puts, 27

- 5,000 FVH 123/123.25 call spds

- +5,000 FVH 119 puts, 14.5

- -4,000 TYH 128.25 straddles, 1-27

- +4,000 TYM 125.5 puts, 39-40

- -5,000 TYH 128.5 calls, 40-38

- Overnight trade

- 12,500 TYH 127.5 puts, mostly 28-32 part tied to condor:

- +5,500 TYH 125.5/126/127/127.5 put condors, 6

- 5,000 TYJ 124.5/126.5 put spds

- 5,000 FVH 118.5/119 put spds

- 10,000 FVH 118/118.75 put spds

- 5,000 FVH 119/120 strangles

- 4,600 FVH 119 puts, 15.5

EGBs-GILTS CASH CLOSE: Yield Bounceback Loses Steam

A bounce-back session for risk saw German and UK yields rise across the curve Tuesday, with periphery EGB spreads tightening.

- But Russia-Ukraine tensions and stock market woes remained prevalent themes, and yields finished off late-morning highs, mirroring a pullback in equities from overnight best levels.

- Duration supply a theme too: Netherlands sold E2bn 30Y DSL, while FInland 20Y mandate helped weigh on semi-core EGBs.

- Italian presidential elections continue; BTP spreads fell 2+bp, GGBs down 3.6bp.

- Some attention on the UK Gov't lockdown party scandal, w headlines that the Gray report would be released tonight. Though most attention on the Federal Reserve decision tomorrow.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.4bps at -0.648%, 5-Yr is up 1.9bps at -0.359%, 10-Yr is up 2.8bps at -0.079%, and 30-Yr is up 3.7bps at 0.235%.

- UK: The 2-Yr yield is up 2.5bps at 0.896%, 5-Yr is up 2.9bps at 0.996%, 10-Yr is up 3.8bps at 1.164%, and 30-Yr is up 4.2bps at 1.284%.

- Italian BTP spread down 2.2bps at 136.9bps / Greek down 3.6bps at 173.6bps

EGB Options: Possible Profit-Taking Ahead Of Fed

Tuesday's Europe rates/bond options flow included:

- RXH2 171/173cs 1x2, bought for 32.5 in 5k

- RXH2 169.5/168.5ps, sold at 26 in 7.75k (closing)

- RXH2 169.50/168.50/167.50p ladder, bought for 10 in 2k

- OEH2 132.25 put bought for 12 in 4.25k

- ERZ2 100.5/100.25/100 iron p fly, sold the body at 19.25 in 1.25k

- 0RG2 100.15/100/99.87p fly, trades 1.5 in 3k

- 0RH2 100.25/100.12/100p fly, sold at 3.25 in 3k

- 0RH2 100.125/100.00 ps bought in 7.8k vs selling 3.9k 100.25c, received 3 ticks for the package (unwind)

- 3RG2 99.75/99.50ps, sold at 10 in circa 6.7k

FOREX: Greenback Off Highs As Equities Stage Another Late Bounce

- A tale of two halves for the US dollar on Tuesday as markets prepare for the January FOMC meeting tomorrow. Renewed equity index weakness during Europe lent support to the greenback and prompted a near 0.4% higher in the DXY. However, another late bounce for the major benchmarks worked against the dollar throughout the US trading session, which now hovers close to unchanged.

- The Swiss Franc is a standout, notably underperforming its G10 counterparts. The strength in USDCHF (+0.56%) prompted a brief breach of the 0.9200 handle, representing a two-week high for the pair. Some analysts speculated the weakness may be down to potential intervention from the central bank with eyes on next Monday’s sight deposit data for any clarification.

- Elsewhere EURGBP fell 0.45% after finding resistance at the 50-day exponential moving average late on Monday around 0.8420. The pair is currently recovering off a multiyear low of 0.8305, Jan 20 low. Gains had been considered corrective with a bearish technical outlook remaining. Further weakness would refocus attention on the major support and bear triggers at 0.8282/77 from February 2020.

- Overall, ranges/volatility continue to be underwhelming in comparison to those seen in equity markets.

- Tomorrow, the first key central bank meeting will be the bank of Canada where analysts are split between a hold and potential lift-off. Focus then turns to the Fed where the FOMC are expected to continue its hawkish shift at the January meeting, using the Statement to signal that a rate hike is coming in March.

FX: Expiries for Jan26 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1225-40(E1.4bln), $1.1280-00(E978mln), $1.1350(E619mln)

- USD/CNY: Cny6.2800($500mln), Cny6.2855($590mln), Cny6.3500($830mln), Cny6.40($642mln)

EQUITIES: Paring Losses, Large Buy Program

Similar to Monday's late rebound on a smaller scale, equities paring losses after report of large 1,500+ name buy program went through, S&P eminis climbed to 4401.50 just ahead the FI close vs. 4279.75 session low.

- One desks revives a NY Fed staff report from Sep 2011 (revised Aug 2013) titled "Pre-FOMC Announcement Drift":

- "We document that since 1994, the S&P500 index has on average increased 49 basis points in the 24 hours before scheduled FOMC announcements. These returns do not revert in subsequent trading days and are orders of magnitude larger than those outside the 24-hour pre-FOMC window."

- Current sector gains has energy stocks outperforming (+3.87%), financials a distant second (+.72%).

COMMODITIES: Oil Close To Reversing Yesterday’s Dip

- Crude oil prices have bounced strongly after yesterday’s losses were led by Fed tightening fears. The latest move has been boosted by a marked recovery in US equities from earlier lows, along with a general backdrop of rising geopolitical tensions.

- The IMF cutting its 2022 global economic growth forecast made little difference compared to broader moves seen today.

- WTI is +2.25% at $85.2. Resistance is seen at $87.1 (Jan 20 high) whilst support is materially lower at $81.90 (Jan 24 low).

- Today's most active strikes in the H2 contract have been $73/bbl puts.

- Brent is +2.0% at $88.02. Next resistance is $89.5, the Jan 19 high and bull trigger, whilst support is $85.04 (Jan 24 low).

- Gold is up +0.3% at $1848.6, having come off new recent highs of $1853.9. It earlier moved through two resistance levels at $1848.0 and $1849.1, potentially opening $1871 (Nov 18 high).

Data Outlook for Wednesday

| Date | GMT/Local | Impact | Flag | Country | Event |

| 26/01/2022 | 0700/0800 | ** |  | SE | PPI |

| 26/01/2022 | 0700/1500 | ** |  | CN | MNI China Liquidity Suvey |

| 26/01/2022 | 0745/0845 | ** |  | FR | Consumer Sentiment |

| 26/01/2022 | 1000/1000 | * |  | UK | Index Linked Gilt Outright Auction Result |

| 26/01/2022 | 1200/0700 | ** |  | US | MBA Weekly Applications Index |

| 26/01/2022 | 1330/0830 | ** | | US | advance trade, advance business inventories |

| 26/01/2022 | 1500/1000 | *** |  | CA | Bank of Canada Policy Decision |

| 26/01/2022 | 1500/1000 | | CA | BOC Monetary Policy Report | |

| 26/01/2022 | 1500/1000 | *** | | US | new home sales |

| 26/01/2022 | 1530/1030 | ** | | US | DOE weekly crude oil stocks |

| 26/01/2022 | 1600/1100 | | CA | BOC Governor press conference after rate decision | |

| 26/01/2022 | 1630/1130 | ** | | US | US Treasury Auction Result for 2 Year Floating Rate Note |

| 26/01/2022 | 1630/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 26/01/2022 | 1900/1400 | *** | | US | FOMC Statement |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok