Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

Market Roundup: Tsy Yields Continued Fall

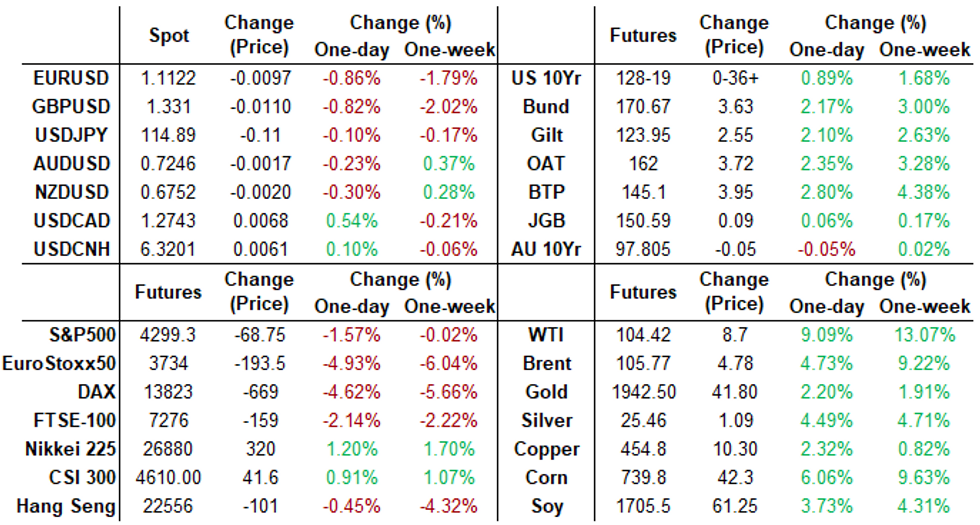

Tsy yields revisited midday lows in late trade, 30YY slipped to 2.0660%L, 2.1157% last (-.0454); 10YY 1.6800L, 1.7173% last -.1077.

- Knock-off affect of Russia's ground war in Ukraine and subsequent wide-ranging sanctions are leaving their mark. Induced stagflation?

- Hearing growing opinion that current events will/may derail central bank plans to hike rates as risk-off/safe-haven buying forces yields lower -- while economic growth falters due knock-off effects of sanctions on Russia having broader ripple effect on food and gas prices.

- Concerns over the Russia/Ukraine conflict getting worse/out of hand quickly more likely the main safe-haven driver -- not a more considered (esoteric) front-running of period of stagflation.

- In the meantime, shares of global banking, shipping, oil producers/distributors, defense contractors alternately being pulled higher/lower due to positive/negative risk exposure to Russia sanctions as well.

- Two days of falling Treasury yields and heavy buying in short end Eurodollar futures (Whites: EDH2-EDZ2 +0.19-0.22; Reds: EDH3-EDZ3 +0.430-0.470) has provided enough of a shift in narrative to draw traders off the sidelines Tuesday. By the close, chances of no hike by the Fed this month had risen to 12%.

- The 2-Yr yield is down 10.8bps at 1.3248%, 5-Yr is down 15.1bps at 1.5665%, 10-Yr is down 10.9bps at 1.7156%, and 30-Yr is down 6.4bps at 2.097%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N -0.00014 at 0.07700% (-0.00014/wk)

- 1 Month -0.00686 to 0.23457% (+0.00400/wk)

- 3 Month +0.00657 to 0.51086% (-0.01214/wk) ** Record Low 0.11413% on 9/12/21

- 6 Month -0.04085 to 0.76386% (-0.06485/wk)

- 1 Year -0.11129 to 1.17671% (-0.15400/wk)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 0.08% volume: $65B

- Daily Overnight Bank Funding Rate: 0.07% volume: $236B

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 0.05%, $1.052T

- Broad General Collateral Rate (BGCR): 0.05%, $369B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $351B

- (rate, volume levels reflect prior session)

NY Fed Purchase Operation: The Desk plans to purchase approximately $20 billion, ending Thu, March 9.

- TIPS 7.5Y-30Y, appr $601M accepted vs. $2.413B submission

- Next scheduled purchases

- Thu 03/03 1100-1120ET: Tsy 7Y-10Y, appr $1.625B vs. $3.225 prior

- Tue 03/08 1010-1030ET: Tsy 22.5Y-30Y, appr $1.825B steady

- Thu 03/09 1010-1030ET: Tsy 2.25Y-4.5Y, appr $4.025B

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage recedes to $1,552.950B w/ 77 counterparties vs. $1,596.052B prior session -- remains well off all-time high of $1,904.582B on Friday, December 31.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- +10,000 Dec 97.50/97.75/98.00/98.25 put condors, 4.25

- +15,000 short Apr 97.50/97.75/98.00 put flys, 4.0

- 10,000 short Jun 97.62/97.75 put spds, 3.5

- 7,700 Mar 99.87 calls, cab

- Overnight trade

- 10,000 Jun 99.43/99.56 call spds

- 15,000 short Apr 97.75 puts

- Block, 6,000 short May 97.68/98.00 2x1 put spds, 0.0

- 8,000 short Sep 96.75/97.25 put spds

- 6,000 Jun 98.25 puts vs. short Jun 97.50/97.75 put spds

- 3,500 short Mar 98.25/98.37/98.50 call flys

- 5,000 short Jun 97.25/97.50 put spds

- 4,000 Dec 98.12/98.75 put spds

- 9,000 short Mar 97.87/98.00 put spds

- 6,000 short Apr 97.68/97.81 put spds

- Block, 5,000 Dec 99.00 calls, 11.5 vs. 98.26/0.18%

- -10,000 TYJ 129 calls, 52

- Overnight trade

- 8,000 TYK 123/124 put spds, 5

- 9,200 FVJ 119.25 calls, 18-20

- 6,000 FVK 116.5/118 3x2 put spds, 35 vs. 118-29.75/0.28%

- 5,000 TYM 124.5/126 put spds, 27

- +15,000 TYK 123/124 put spds, 5 vs. 128-11.5/0.08%

- Blocks, total 20,000 TYJ 130 calls, 33-35, more on screen from lower lvls:

- 5,000 TYJ 130 calls, 12

FOREX: Souring Risk Sentiment Weighs On Euro, EURUSD Prints Below 1.1100

- Amid the ongoing Russia/Ukraine warfare, market expectations of the first ECB rate hike were pushed back to 2023, in turn weighing on the Euro throughout Tuesday’s session.

- Euro weakness was fairly broad based with notable extensions lower in EURJPY and EURCHF, the latter sinking to the lowest point since shortly after the removal of the floor in January 2015.

- EURUSD (-0.84%) also plunged to fresh recent lows, printing below the 1.11 handle to 1.1090. Having temporarily breached support and the bear trigger through 1.1106, the next targets are 1.0976, 2.00 projection of the Jan - Jun - May ‘21 price swing and 1.0871 Low May 25, 2020.

- EURUSD weakness and renewed selling pressure in equities lent support to the dollar index which climbed around 0.7%. Heavy euro crosses and the continued surge in commodity prices prompted relative resilience in the likes of AUD (-0.17%), NZD (-0.34%) and to an extent CAD (-0.45%).

- EURGBP weakness also kept GBP on a relatively firm footing, however, cable played catch up to the broad USD strength, shooting down from 1.34 to within close proximity of the 1.33 handle.

- In emerging markets, PLN, HUF and CZK were all offered throughout the session amid the single currency weakness and their direct exposure to the Ukraine crisis. Both Hungarian and Polish central banks took the opportunity to verbally intervene, dragging the local currencies off the worst levels.

- Australian GDP data kicks off Wednesday’s APAC session before the European docket is highlighted by Eurozone HICP Inflation flash estimates. Later on Wednesday, the Bank of Canada are expected to commence lift-off with a quarter point hike to 0.5%.

Equity Roundup: Near Late Session Lows

Risk-off theme continues, stocks testing session lows, Rates near highs in late trade.

Recent headlines contributing to the tone:

- STOXX TO REMOVE 61 RUSSIAN COMPANIES FROM INDICES: FT

- EU ENVOYS APPROVE LIST OF 7 RUSSIAN BANKS TO BE CUT OFF SWIFT

- Earlier draft list of seven banks: VTB Bank PJSC and Bank Rossiya Bank Otkritie, Novikombank, Promsvyazbank PJSC, Sovcombank PJSC and VEB.RF.

- Knock-on pressure for Large US Banks: JP Morgan (-5.55% to 133.94, -7.90), Goldman Sachs (-3.82% to 328.10, -13.02), Bank of America (-4.92% to 42.03, -2.17). American Express (-7.49% to 179.86, -14.38)

- Airlines: Boeing (-5.24% to 194.59, -10.76); Delta (-5.05% to 37.90, -2.0)

- Weak auto sales weighing on Honda (-2.68% to 29.74, -0.82), sales in Feb down 20.6%.

- SPX Eminis -73.25 points (-1.68%) at 4295.25; Dow Industrials -674.35 points (-1.99%) at 33215.18; NASDAQ -210.5 points (-1.5%) at 13541.24.

- SPX lagging sectors:

- Financials -4.07%

- Materials -2.54%

- Information Technology -1.96%

- RES 4: 4671.75 High Jan 18

- RES 3: 4586.00 High Feb 2 and a key resistance

- RES 2: 4494.61 50-day EMA

- RES 1: 4408.26 20-day EMA

- PRICE: 4357.50 @ 14:27 GMT Mar 1

- SUP 1: 4101.75 Low Feb 24 and the bear trigger

- SUP 2: 4055.60 Low May 19 2021 (cont)

- SUP 3: 4029.25 Low May 13 2021 (cont)

- SUP 4: 3990.50 0.764 proj of the Jan 4 - 24 - Feb 2 price swing

Medium-term E-Mini S&P found resistance this morning ahead of the 20-day EMA that intersects at 4408.26. This represents an important intraday resistance. Recent gains are likely part of a corrective cycle that is allowing a recent oversold condition to unwind. A deeper sell-off would signal a resumption of the downtrend and refocus attention on 4101.75, the Feb 24 low and bear trigger. A breach of the 20-day EMA would expose 4494.61.

COMMODITIES: Oil, Gold and Gas Surge On Continued Russian Escalation

- Crude oil has surged 8% today on continued escalation of the Russian invasion and growing supply concerns, with the Brent-WTI spread narrowing further as traders seek out alternatives and gains heavily front-loaded in shorter-dated contracts.

- WTI is +9.2% at $104.4, off an earlier high of $106.78 which has seen four resistance levels blown out through the course of the day, the highest being $105.25 (Jul 22, 2014 high, cont).

- The most active calls in the Apr22 contract have been $110/bbl but there has even been decent volumes up at $120/bbl. The most active puts have been at $90/bbl.

- Brent is +7.9% at $105.7, also down from earlier highs of $107.44 (Aug 8, 2014 high, cont).

- Gold once again gains strongly on its safe haven and inflation hedging properties, up +1.7% at $1940.5 as it currently tests the bull channel top of $1940.9 drawn from the Aug 9 2021 low. A clear break here would open $1974.3 (Feb 24, initial Russian invasion high).

- European natural gas prices surged again, up 22-23% and with ytd increases closing in on 70%.

Wednesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 02/03/2022 | 0001/0001 | * |  | UK | BRC Monthly Shop Price Index |

| 02/03/2022 | 0700/0700 | * | | UK | Nationwide House Price Index |

| 02/03/2022 | 0855/0955 | ** |  | DE | unemployment |

| 02/03/2022 | 1000/1000 | ** | | UK | Gilt Outright Auction Result |

| 02/03/2022 | 1000/1100 | *** |  | EU | HICP (p) |

| 02/03/2022 | 1000/1100 | | EU | ECB Schnabel at BMAS roundtable | |

| 02/03/2022 | 1100/1200 | | EU | ECB de Guindos Q&A at Universidad Carlos III | |

| 02/03/2022 | 1200/0700 | ** |  | US | MBA Weekly Applications Index |

| 02/03/2022 | 1315/0815 | *** | | US | ADP Employment Report |

| 02/03/2022 | 1400/0900 | | US | Chicago Fed's Charles Evans | |

| 02/03/2022 | 1430/0930 | | US | St. Louis Fed's James Bullard | |

| 02/03/2022 | 1500/1000 | *** |  | CA | Bank of Canada Policy Decision |

| 02/03/2022 | 1500/1000 | | US | Fed Chair Pro Tempore Jerome Powell | |

| 02/03/2022 | 1530/1030 | ** | | US | DOE weekly crude oil stocks |

| 02/03/2022 | 1600/1700 | | EU | ECB Lane lecture at Hertie School Berlin | |

| 02/03/2022 | 1630/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 02/03/2022 | 1830/1830 | | UK | BOE Tenreyro speech to Economic Research Council | |

| 02/03/2022 | 1900/1400 | | US | Fed Beige Book | |

| 02/03/2022 | 2000/2000 | | UK | BOE Cunliffe speech at Oxford Union | |

| 02/03/2022 | 2130/1630 | | US | New York Fed's Lorie Logan | |

| 03/03/2022 | 2200/0900 | * |  | AU | IHS Markit Final Australia Services PMI |

| 03/03/2022 | 0030/1130 | ** | | AU | Trade Balance |

| 03/03/2022 | 0030/1130 | * | | AU | Building Approvals |

| 03/03/2022 | 0030/0930 | ** |  | JP | IHS Markit Final Japan Services PMI |

| 03/03/2022 | 0145/0945 | ** |  | CN | IHS Markit Final China Services PMI |

| 03/03/2022 | 0700/0200 | * |  | TR | Turkey CPI |

| 03/03/2022 | 0730/0830 | ** |  | SE | Manufacturing PMI |

| 03/03/2022 | 0730/0830 | ** | | SE | Services PMI |

| 03/03/2022 | 0730/0830 | *** |  | CH | CPI |

| 03/03/2022 | 0815/0915 | ** |  | ES | IHS Markit Services PMI (f) |

| 03/03/2022 | 0845/0945 | ** |  | IT | IHS Markit Services PMI (f) |

| 03/03/2022 | 0850/0950 | ** |  | FR | IHS Markit Services PMI (f) |

| 03/03/2022 | 0855/0955 | ** | | DE | IHS Markit Services PMI (f) |

| 03/03/2022 | 0900/1000 | ** | | EU | IHS Markit Services PMI (f) |

| 03/03/2022 | 0930/0930 | ** | | UK | IHS Markit/CIPS Services PMI (Final) |

| 03/03/2022 | 1000/1100 | ** | | EU | retail sales |

| 03/03/2022 | 1000/1100 | ** | | EU | unemployment |

| 03/03/2022 | 1000/1100 | ** | | EU | PPI |

| 03/03/2022 | 1330/0830 | ** | | US | WASDE Weekly Import/Export |

| 03/03/2022 | 1330/0830 | ** | | US | Jobless Claims |

| 03/03/2022 | 1330/0830 | ** | | US | Non-Farm Productivity (f) |

| 03/03/2022 | 1445/0945 | *** | | US | IHS Markit Services Index (final) |

| 03/03/2022 | 1500/1000 | *** | | US | ISM Non-Manufacturing Index |

| 03/03/2022 | 1500/1000 | ** | | US | factory new orders |

| 03/03/2022 | 1500/1000 | | US | Fed Chair Pro Tempore Jerome Powell | |

| 03/03/2022 | 1530/1030 | ** | | US | Natural Gas Stocks |

| 03/03/2022 | 1630/1130 | ** | | US | NY Fed Weekly Economic Index |

| 03/03/2022 | 1630/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 03/03/2022 | 1630/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 03/03/2022 | 1630/1130 | | CA | BOC Governor Macklem speech, "Economic Progress Report." | |

| 03/03/2022 | 2030/1530 | | CA | BOC Governor Macklem testifies at House committee. | |

| 03/03/2022 | 2130/1630 | | US | New York Fed's Lorie Logan | |

| 03/03/2022 | 2300/1800 | | US | New York Fed's John Williams |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.