Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: Fed Taking Inflation Seriously

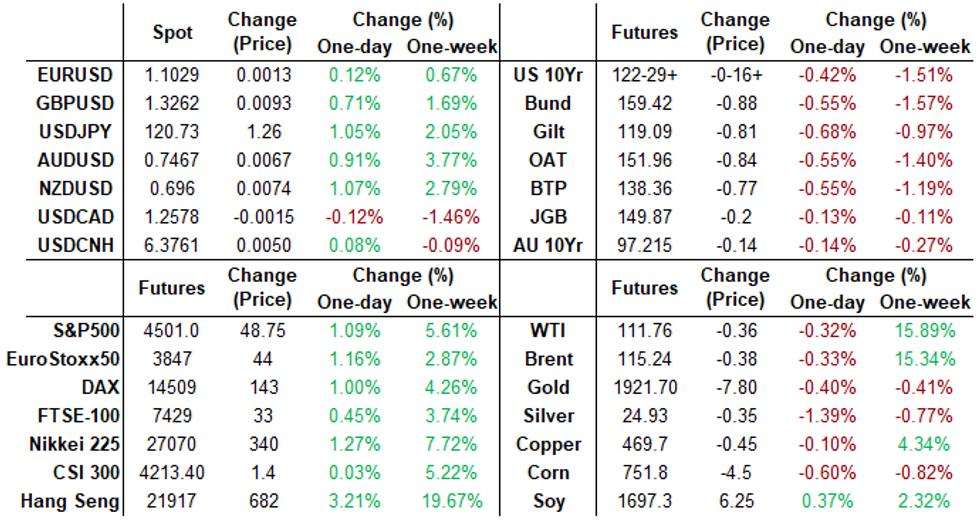

Rates finish broadly weaker yet again, 30YY climbs to late session high of 2.6153% +0.0988, highest lvl since July 2019. Markets less whippy than Monday opener, better volumes, market depth w/Japan back from extended holiday weekend.

- Tsy sell-off accelerated early after StL Fed Pres Bullard comments on Bbg TV urged Fed to "move aggressively to curb inflation .. faster is better" to get "policy back to neutral", adding 50bp hike "would definitely be in the mix."

- Slight delayed reaction to hawkish StL Fed Bullard comments, lead quarterly Eurodollar futures reversed after going bid on lower 3M LIBOR settle (-0.00386 to 0.95371%, +0.01971/wk). Balance of Whites-Reds (EDU2-EDH4) weaker but off lows as markets priced in increased chances for 50bps hike in May and/or June.

- Trading desks report moderate domestic real$ buying in 3s around comment from SF Fed Pres Daly re: inflation expectations "well anchored". U.S. economy can probably escape a 1970s-style bout of stagflation Daly explained because America has emerged as an oil exporter since then and because economic growth will likely remain around its long-run trend rate.

- More Fed-speak on tap Wednesday, limited data:

- 0800ET: Fed Chair Powell, BIS Innovation panel event, moderated Q&A

- 1000ET: New Home Sales (801k, 810k); MoM (-4.5%, +1.1%)

- 1145ET: SF Fed Daly, moderated discussion Bbg equality summit

- 1300ET: US Tsy $16B 20Y Bond auction re-open (912810TF5)

- 1500ET: StL Fed Bullard economic outlook, no text, moderated Q&A

- 2105ET: StL Fed Bullard pre-recorded economic outlook, Credit Suisse conf

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N -0.00271 at 0.32743% (-0.00128/wk)

- 1 Month +0.01086 to 0.45486% (+0.00829/wk)

- 3 Month -0.00386 to 0.95371% (+0.01971/wk) ** Record Low 0.11413% on 9/12/21

- 6 Month +0.04843 to 1.38457% (+0.09700/wk)

- 1 Year +0.14443 to 2.01257% (+0.22614/wk)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 0.33% volume: $76B

- Daily Overnight Bank Funding Rate: 0.32% volume: $260B

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 0.29%, $989B

- Broad General Collateral Rate (BGCR): 0.30%, $381B

- Tri-Party General Collateral Rate (TGCR): 0.30%, $371B

- (rate, volume levels reflect prior session)

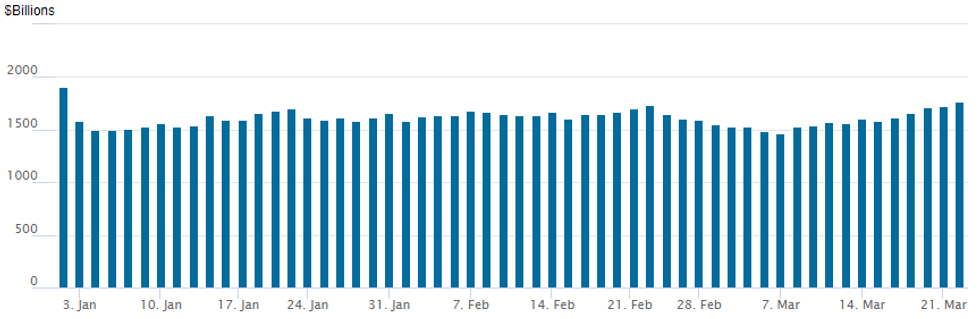

FED Reverse Repo Operation, Second Highest on Record

NY Federal Reserve/MNI

NY Fed reverse repo usage climbs to second highest on record at $1,763.183B w/ 88 counterparties vs. $1,728.893B prior session -- still well off all-time high of $1,904.582B on Friday, December 31.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Carry-over bid for outright puts and put spreads reported Tuesday as FI sell-off accelerated this morning after StL Fed Pres Bullard comments on Bbg TV urged Fed to "move aggressively to curb inflation .. faster is better" to get "policy back to neutral", adding 50bp hike "would definitely be in the mix."- Slight delayed reaction to hawkish StL Fed Bullard comments, lead quarterly Eurodollar futures reversed after going bid on lower 3M LIBOR settle (-0.00386 to 0.95371%, +0.01971/wk). Growing expectation of 50bp hike from Fed in May and June spurred buying of 5,000 Jun 98.00/98.12/98.25/98.37 put condors, 3.5 and 20,000 Jun 98.62 puts 10.5-12.0 over Dec 97.87/98.12 put spds.

- Treasury options saw pick-up in call buying later in session as sell-off in underlying levels out: salient trade included +12,500 TYK 124.5 calls, 22, block buy of 10,000 TYK 122.5/125 1x3 call spds, 24 and buy of +25,000 FVK 115 calls, 38.5-40 vs. 114-29.

- +5,000 SFRZ2 97.75/98.00 put spds, 15.0 ref: 97.695

- Block: 15,000 Dec 97.00/97.25 put spds 7.0 over 98.50/98.75 call spds at 1040:25ET

- Block, 2,200 Sep 98.25/98.50 6x5 put spd, 39.5 net at 1030:09

- +3,000 Green Jun 96.37/97.00 2x1 put spds 2.0 over -6,000 Green Jun 98.12 calls

- +20,000 Jun 98.62 puts 10.5-12.0 over Dec 97.87/98.12 put spds

- +5,000 Jun 98.00/98.12/98.25/98.37 put condors, 3.5

- Block, 15,000 Green Sep 98.25 straddles vs. Green Dec 97.37/97.87 strangle, 42.5

- -5,000 Blue Jun 97.75/98.00 put spds, 18.25

- Overnight trade

- -4,000 Green Apr 97.00/97.25/97.50 put flys, 7.0 vs. 97.335/0.04%

- +4,000 Sep 75/77 put spds 1.0 over 98.00/98.25 call spds

- +12,500 TYK 124.5 calls, 22

- +25,000 FVK 115 calls, 38.5-40 vs. 114-29.5

- Block, 10,000 TYK 122.5/125 1x3 call spds, 24

- -5,000 FVK 116.25 puts, 132

- 5,000 FVK 112.5/112.75/113.75 broken put flys

- -3,000 TYM 121/125 put over risk reversals, 4 vs. 123-00/0.52%

- 1,500 FVK 112.75 puts, 6

- 3,500 TYM 124/125 put spds, 22

- 1,300 FVJ 114.5/115/115.25/115.75 put condors

- Overnight trade

- +10,000 TYK 119/120 put spds, 4-5

- -6,000 TYK 123/124/125 put flys, 11

- Block, -5,000 FVK 116.25 puts, 121.5

EGBs-GILTS CASH CLOSE: Bear Flattening

The German and UK curves bear flattened as the short-end sold off sharply once again.

- The increasingly hawkish shift by the Federal Reserve drove most of the move, but there has also been an element of risk appetite returning (BTP spreads lower, equities higher).

- 10Y Bund and Gilt yields hit fresh post-2018 highs, but the 2Y segment underperformed on both curves as central bank hike pricing ticked higher.

- UK in focus Weds, with CPI data and Spring budget statement (our preview is on the MNI website).

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 4.9bps at -0.235%, 5-Yr is up 4.7bps at 0.223%, 10-Yr is up 3.5bps at 0.505%, and 30-Yr is up 1.4bps at 0.672%.

- UK: The 2-Yr yield is up 9.3bps at 1.415%, 5-Yr is up 8.4bps at 1.462%, 10-Yr is up 7bps at 1.708%, and 30-Yr is up 5.6bps at 1.922%.

- Italian BTP spread down 2.2bps at 151.7bps / Greek up 2.1bps at 224.1bps

EGB Options: Bund And BTP Downside

Tuesday's Europe rates/bond options flow included:

- RXK2 155.5/154.5/153.5p fly, bought for 5 in 3k

- OEJ2 130.00/129.75 ps, bought for 13.5 in 12.35k

- ERZ2 100.12/100.25c ladder, bought for 1.5 in 1k

- IKJ2 138/136 ps, bought for 32 in 4.5k (ref 138.75)

- SFIK2 98.55/98.65/98.70/98.80c condor, bought 2.75 in 10k

FOREX: USD/JPY Most Technically Overbought In Six Years

- The USD/JPY rally drew plenty of attention Tuesday, with the pair clearing the psychological 120 handle and briefly tipping above the Y121 level. The move coincided with a sizeable move in 5Y breakevens, which increased back to highs of 3.68%. This comes despite oil moving lower and the tighter rates pricing, with an additional 193bps of hikes priced across 2022.

- Market focus turns to the longevity of recent strength, with the USD/JPY RSI now tipped to its highest level since late-2016. The Japanese finance minister commented after the Asia-Pac market close, noting that sudden moves in currency markets aren't desirable, and stability remains important. Markets will be on watch for any strengthening of this rhetoric.

- Elsewhere, GBP/USD underwent a sizeable intraday rally, topping the Monday high in short order and making headway north of both 1.3250 as well as key resistance at 1.3231 20-day EMA. Moves came despite the more hawkish Fed tones evident in FOMC appearances this week, with markets repricing a BoE hiking to see close to five 25bps by year-end.

- Antipodean currencies outperformed throughout, with AUD and NZD at the top of the G10 pile, pushing AUD/USD through early March's 0.7441 and to the best levels since mid-November.

- Focus Wednesday turns to the UK's Spring Statement (preview here: https://marketnews.com/mni-research/global-issuanc...) and inflation data, as well as US new homes sales. Speeches are due from BoE's Bailey, Fed's Powell and ECB's Visco - among others.

FX: Expiries for Mar23 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0850(E621mln), $1.1065-80(E1.1bln)

- EUR/JPY: Y130.50(E815mln)

- USD/CAD: C$1.2630-50($1.3bln)

EQUITIES: Late Equity Roundup, Near Late Highs

Looking strong in late trade, SPX eminis holding above key (round number) resistance of 4500.0 at 4505.25 (+52.75, 1.18%), with focus on next resistance of 4578.50 High Feb 9; Dow trades +261.8 (0.76%) at 34822.42, Nasdaq +269.3 (1.9%) at 14108.45.

- Combination of factors buoyed stocks: broad based share buy backs ("Alibaba boosted its share buyback program to $25 billion from $15 billion" WSJ), renewed support from China to support economy and markets, and peripherally, weaker crude: WTI off midday lows at $111.76 (loosely tied to lack of unified EU ban on Russia oil imports).

- SPX leading/lagging sectors: Consumer Discretionary (2.66%) driven by surge in autos +7.18%; Communication sector (+2.25%) with media and entertainment (+2.58%) leading. Financials sector (1.75% moved past Information Technology (1.60%) in the second half, Banks outperforming diversified financials and insurance names.

- Laggers: As noted, lack of follow-through in crude weighing on Energy sector (-0.62%), petroleum drillers, manufacturers, pipelines trading lower but off lows.

- Dow Industrials Leaders/Laggers: Boeing (BA) holding near highs at 190.80 after Mon's sell-off on China 737 crash. Cloud-based software company Salesforce.Com (CRM) stronger but off highs (+4.38 at 218.14), Microsoft (MSFT) a close second (+4.47 at 303.64).

- Laggers: United Health -1.50 at 506.16 and Caterpillar -0.93 at 222.78.

- RES 4: 4730.50 High Jan 1

- RES 3: 4663.50 High Jan 18

- RES 2: 4578.50 High Feb 9 and a key resistance

- RES 1: 4500.00 Round number resistance

- PRICE: 4481.00 @ 13:42 GMT Mar 22

- SUP 1: 4336.06 20-day EMA

- SUP 2: 4129.50/4094.25 Low Mar 15 / Low Feb 24 and a bear trigger

- SUP 3: 4055.60 Low May 19 2021 (cont)

- SUP 4: 4029.25 Low May 13 2021 (cont)

COMMODITIES: Oil Prices Pause On Lack Of New Drivers

- Oil prices are currently relatively little changed on yesterday’s settlement with no new major progress on the EU mulling a ban on Russian oil imports or headlines on Iran talks.

- More recent reports of a Ukrainian counter-attack against Russian forces in the north of the country but see some escalation ahead.

- WTI is -0.3% at $111.76. Initial resistance is seen at the overnight high of $115.01 and then $116.38 (61.8% retracement of Mar 7-15 downleg) whilst support is the 20-day EMA of $102.97.

- Brent is -0.05% at $115.56, again below the intraday high of $119.48 whilst support is the 20-day EMA of $105.95.

- Gold is -0.7% at $1922.31 in a continuation of the reaction to Powell dialling up hawkishness yesterday. Resistance remains at $1954.7 (Mar 15 high) and support at $1895.3 (Mar 15 low).

- US natural gas meanwhile bucked the softer moves elsewhere, up 6% on colder weather.

Wednesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 23/03/2022 | 0700/0700 | *** |  | UK | Consumer inflation report |

| 23/03/2022 | 0700/0700 | *** | | UK | Producer Prices |

| 23/03/2022 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 23/03/2022 | - | | UK | OBR Economic and Fiscal Forecast | |

| 23/03/2022 | - | | UK | DMO 2022-23 Financing Remit | |

| 23/03/2022 | 1200/1200 | | UK | BOE Bailey Panels BIS Innovation Summit | |

| 23/03/2022 | 1200/0800 | | US | Fed Chair Jerome Powell | |

| 23/03/2022 | 1230/1230 | | UK | FY 2022/23 Budget statement | |

| 23/03/2022 | 1315/1415 |  | EU | ECB Lagarde Speech at BIS Innovation Summit | |

| 23/03/2022 | 1400/1000 | *** | | US | New Home Sales |

| 23/03/2022 | 1430/1030 | ** | | US | DOE weekly crude oil stocks |

| 23/03/2022 | 1435/1035 | | US | New York Fed's John Williams | |

| 23/03/2022 | 1500/1600 | ** | | EU | Consumer Confidence Indicator (p) |

| 23/03/2022 | 1530/1530 | | UK | DMO Quarterly Consultation Meetings Agenda | |

| 23/03/2022 | 1530/1130 | ** | | US | US Treasury Auction Result for 2 Year Floating Rate Note |

| 23/03/2022 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 23/03/2022 | 1545/1145 | | US | San Francisco Fed's Mary Daly | |

| 23/03/2022 | 1700/1300 | ** | | US | US Treasury Auction Result for 20 Year Bond |

| 23/03/2022 | 1900/1500 | | US | St. Louis Fed's James Bullard | |

| 24/03/2022 | 2200/0900 | *** |  | AU | IHS Markit Flash Australia PMI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.