Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

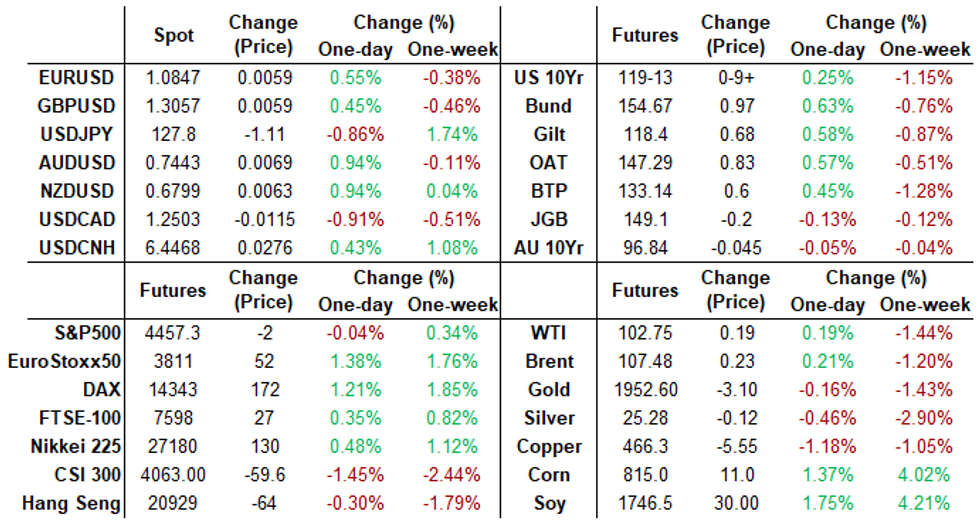

US TSYS: 2s10s Yield Curves 16Bp Off Early Tuesday Highs

Tsy futures trading mostly mostly higher through the day, curves flatter with long end outperforming, 30Y bonds bouncing back near second half highs, 30YY currently 2.8788% vs. 2.8635% low.- Curves bull flattened Wednesday (2s10s off early Tue's high of 42.897, currently -7.606 at 26.219) as short end remained under pressure -- pricing in two to three 50bp hikes over the next three FOMC meetings.

- Little react to in-line March reading of Existing Home Sales of 5.77M units annualized, or -2.7% MoM.

- Bond yield had climbed to new 3-year high of 3.0285% in early Asia hours before the Bank of Japan offered to conduct an unlimited purchase of Japanese Government Bonds (JGBs). That put the brakes on surge in yields as they retreated into the NY open.

- Adding impetus to the bid: Some trading desks citing surge in industrial production and housing starts that recession fears are overblown, and looking for longer futures to continue to rebound.

- Tsy futures gapped higher (30YY falls to 2.8874% low) after strong $16B 20Y note auction reopen (912810TF5) trades through with 3.095% high yield vs. 3.120% WI; 2.80x bid-to-cover vs. last month's 2.72x.

- Fed speak on tap Thu: Fed Chair Powell, ECB Pres Lagarde at IMF/global economy panel event at 1300ET. Fed Blackout midnight Friday.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N +0.00871 at 0.33100% (+0.00114/wk)

- 1 Month +0.00686 to 0.63157% (+0.03714/wk)

- 3 Month +0.03800 to 1.13629% (+0.07358/wk) ** Record Low 0.11413% on 9/12/21

- 6 Month +0.06743 to 1.67457% (+0.11786/wk)

- 1 Year +0.06629 to 2.36886% (+0.14729/wk)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 0.33% volume: $70B

- Daily Overnight Bank Funding Rate: 0.32% volume: $263B

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 0.28%, $895B

- Broad General Collateral Rate (BGCR): 0.30%, $342B

- Tri-Party General Collateral Rate (TGCR): 0.30%, $327B

- (rate, volume levels reflect prior session)

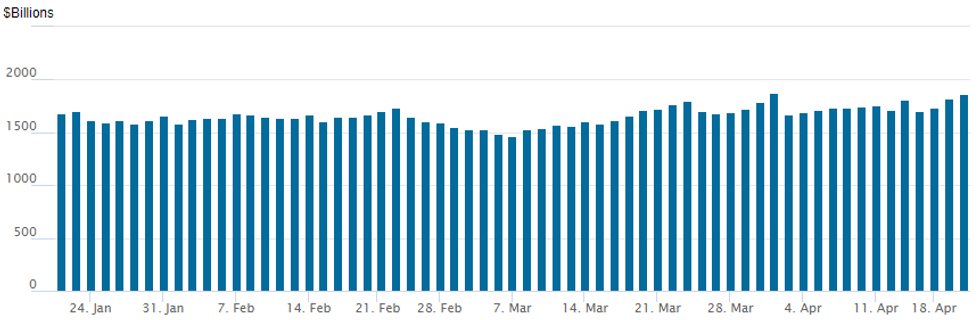

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage climbs to 1,866.560B w/ 93 counterparties from prior session 1,817.929B. Compares to all-time high of $1,904.582B on Friday, December 31.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Tuesday's better upside call buying fading the sell-off in underlying futures that saw 30YY top 3% (3.016%; 3.0285% during Asia hours) - had the right idea anticipating Wednesday's rally as underlying futures bounced off lows after the Bank of Japan offered to conduct an unlimited purchase of Japanese Government Bonds (JGBs).- (BOJ offered to conduct an unlimited purchase of Japanese Government Bonds (JGBs) at a fixed rate from April 21 to April 26 to prevent the 10-year JGB yield from rising above 0.25%, an upper limit of the preferred minus-plus 0.25% range.)

- Some trading desks citing surge in industrial production and housing starts that recession fears are overblown, and looking for longer futures to continue to rebound. Wrap: curves bull flattened Wednesday as short end remained under pressure -- pricing in two to three 50bp hikes over the next three FOMC meetings.

- Eurodollar put buying out to September expirys saw moderate volumes while 3Y midcurves saw decent buying in 3Y midcurve calls on the day. Treasury options saw more consistent buying in 10Y calls on the day.

- Block total +32,442 short May SOFR (0QK2) 97.12 calls, 6.0 vs. 96.82/0.23%

- Block 10,000 SFRU2 96.87 puts, 3.75 vs. 97.84/0.05%

- Block, +5,000 short Jun 96.62/96.87 put spds, 11.5

- Update, +11,000 Blue Jun'25 98.00 calls, 1.5 ref 96.965

- +7,500 Jun 98.37/98.50 call spds, 2.0

- +5,000 Sep 97.62/97.75 put spds, 7.5

- +6,000 short Jun 96.25/96.75 put over risk reversals, 0.5 net vs. 96.495/0.64%

- Overnight trade

- +10,000 Jun 97.87/98.12 put spds, 2.0 ref 98.30

- -4,000 Jun 98.00/98.25 call spds 20.5 vs. 98.305/0.29%

- +2,000 short May 96.50/96.75 1x2 call spds

- 10,000 TYM 119.5/121.5 1x2 call spds, 27

- +25,000 FVM 114 calls, 17

- 3,300 USM 132/134/136/138 put condors

- +3,000 TYM 121 calls 0.0 over TYN 122 calls, ref 118-28

- +2,500 FVM 112.5/113 put spds, 15

- Overnight trade

- 8,000 TYK 119 puts mostly 10-15

- 5,700 TYM 118 puts, 42

- Blocks, total 10,000 FVM 112 puts, 27-27.5

- +2,500 USM 134/136/138 put flys, 12 ref 140-08

FOREX: G10 Currencies Supported Amid Greenback Weakness, CNH The Outlier

- As yields in the US reversed the entirety of yesterday’s move higher, the US dollar echoed the price action, trading with an offered tone throughout Wednesday. The USD index is set to snap a four-day winning streak, having retreated 0.62% as we approach the APAC crossover.

- Greenback weakness lent support to the majority of other G10 currencies, with particularly impressive rallies for the likes of AUD, CAD and NZD, all rising over 1% amid another solid day for major equity benchmarks. In particular, the Canadian dollar was provided with an additional tailwind following above expectation CPI figures for March. This prompted various sell-side institutions to adjust their BOC rate calls with a Scotiabank analyst citing there is a solid case for a 75-100bp single hike in June.

- USDCAD’s recent move lower has threatened a bullish theme and highlights the fact that price has so far failed to remain above the 50-day EMA. Note that the Apr 13 session appears to be a bearish engulfing candle, which if correct, highlights a reversal. The breach of both 1.2522, Apr 14 low and 1.2479, Apr 6 low are additional bearish developments.

- USDJPY remains extremely volatile and following another overnight cycle high print of 129.40, the pair has sharply retraced. Worth noting the pair came within four pips of touted Fibonacci projection resistance and aided by the broad dollar weakness, the pair now resides back below the 128 mark.

- The Chinese Yuan was the clear outlier on Wednesday – weaker by almost half a percent. CNH weakness comes as an extension from price action on Tuesday and price action has been exacerbated by technical breaks of both the 200day MA and long-term downward trendline as indicated below.

- New Zealand CPI highlights the overnight data releases before the final reading of Eurozone CPI. Philly Fed Manufacturing Index and Initial Jobless Claims are on the US docket before potential comments from Fed, ECB and BoE Governors as they participate in panel discussions at the Spring meetings of the IMF.

FX: Expiries for Apr21 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0700(E920mln), $1.0800(E871mln), $1.0900-05(E3.2bln), $1.0925-35(E578mln), $1.1000(E1.3bln)

- USD/JPY: Y124.85-00($1.4bln)

- GBP/USD: $1.3050(Gbp860mln)

- AUD/USD: $0.7400-20(A$954mln)

- USD/CAD: C$1.2500($770mln), C$1.2650($565mln)

EQUITIES: Late Equity Roundup: Waiting For AA, UAL, TSLA Earnings

Stock indexes holding mixed after the FI close, DJIA and SPX mildly firmer vs. weaker NASDAQ levels into midday. SPX eminis traded weaker into the rate close have rebounded: ESM2 +9.5 (0.21%) at 4469 - still above 50-day EMA that intersects at 4447.32.

- Key resistance established at 4519.75, the Apr 8 high, where a break would ease the bearish threat. On the flipside, key support at 4355.50 Low Apr 18, followed by 4321.07 61.8% retracement of the Mar 15 - Mar 29 rally.

- Earnings cycle gains momentum, most early releases beat est's. Waiting for AA, UAL, TSLA after the close.

- SPX leading/lagging sectors: Real Estate (+2.13%) continues to outpace Consumer Staples (+1.58%) and Health Care (+1.55%).

- Laggers: Communication Services hit (-3.90%) after Netflix annc huge drop (-200k) in subscribers late Tue. NFLX currently -36.34% to 221.93.

- Meanwhile, Dow Industrials currently trades +299.28 (0.86%) at 35211.42, Nasdaq -147.4 (-1.1%) at 13472.43.

- Dow Industrials Leaders/Laggers: IBM also annc late Tue: leads rally (+9.05 at 138.16) on strong revs +8% and strong guidance in hybrid cloud service. Bad day for Disney (-6.93 at 124.97) as Fl Gov DeSantis seeks to end special tax district benefit.

E-MINI S&P (M2): Gains Considered Corrective

- RES 4: 4663.50 High Jan 18

- RES 3: 4631.00 High Mar 29 and a key resistance

- RES 2: 4588.75 High Apr 5

- RES 1: 4519.75 High Apr 8

- PRICE: 4446.50 @ 1600ET Apr 20

- SUP 1: 4355.50 Low Apr 18

- SUP 2: 4321.07 61.8% retracement of the Mar 15 - Mar 29 rally

- SUP 3: 4247.89 76.4% retracement of the Mar 15 - Mar 29 rally

- SUP 4: 4129.50 Low Mar 15

The S&P E-Minis short-term condition remains bearish despite this week’s gains - a corrective bounce. The contract recently traded through its 50-day EMA, which intersects at 4447.32, and this has reinforced a bearish threat. The move below 4400.00 signals scope for weakness towards 4321.07 next, a Fibonacci retracement. Initial firm resistance has been established at 4519.75, the Apr 8 high A break would ease the bearish threat.

COMMODITIES: WTI and Gold Prices Steady With Lack Of New Drivers

- Oil prices are flat to up slightly after sliding heavily yesterday with no material change in geopolitical headlines -- Russia tests a new ballistic missile which the Pentagon describes as a routine test, the Kremlin said the ball is in Ukraine’s court on peace talks having passed a document to them which Zelensky since denied.

- An earlier dip was reversed on a very large draw in US crude oil inventories.

- WTI is +0.5% at $103.1, with room to move around in whilst comfortably above support at $98.82 (50-day EMA) and below resistance at $109.81 (Apr 18 high).

- Brent meanwhile is unch at $107.28 having briefly cleared support at the 20-day EMA of $106.69 having failed to clear it yesterday (unlike both WTI and gold). Resistance is eyed at $114.84 (Apr 18 high).

- Gold is +0.15% at $1953.0, seeing surprisingly little boost from the slide in Treasury yields despite having suffered yesterday. Support is $1925.2 (50-day EMA) whilst resistance remains the bull trigger of $1998.4 (Apr 18 high).

Thursday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 21/04/2022 | 0645/0845 | ** |  | FR | Manufacturing Sentiment |

| 21/04/2022 | 0900/1100 | *** |  | EU | HICP (f) |

| 21/04/2022 | - | | EU | ECB Lagarde & Panetta in IMF/World Bank Meetings | |

| 21/04/2022 | 1230/0830 | ** |  | US | Jobless Claims |

| 21/04/2022 | 1230/0830 | ** | | US | Philadelphia Fed Manufacturing Index |

| 21/04/2022 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 21/04/2022 | 1300/1400 |  | UK | BOE Mann Speaks at BOE Webinar | |

| 21/04/2022 | 1400/1600 | ** | | EU | Consumer Confidence Indicator (p) |

| 21/04/2022 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 21/04/2022 | 1500/1100 | | US | Fed Chair Jerome Powell | |

| 21/04/2022 | 1530/1130 | ** | | US | NY Fed Weekly Economic Index |

| 21/04/2022 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 21/04/2022 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 21/04/2022 | 1630/1730 | | UK | BOE Bailey at Peterson Institute Event | |

| 21/04/2022 | 1630/1230 | | US | St. Louis Fed's James Bullard | |

| 21/04/2022 | 1700/1300 | ** | | US | US Treasury Auction Result for TIPS 5 Year Note |

| 21/04/2022 | 1700/1300 | | US | Fed Chair Jerome Powell | |

| 21/04/2022 | 1700/1900 | | EU | ECB Lagarde at IMF Debate |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok